Article 18 of the LFSS 2024 (adopted, I remind you, by procedure 49.3, therefore without debate) introduces a profound reform of the social contribution base for self-employed workers, and in particular doctors.

The consequences for them will however be different depending on the annual BNC (Non-Commercial Profit) on the one hand, and on the other hand the conventional sector to which they belong.

So what does this reform consist of?

Small reminder: the CSG and the CRDS are not counted in social contributions but in taxes!

Currently social contributions are calculated on the BNC (plus tax exemptions and holiday voucher tax reductions), and the CSG and RDS on this same basis plus social contributions, which increases them significantly.

From 2025 income, the contribution base will be unified and simplified.

It will be calculated on the BNC plus social security contributions, to which a reduction of 26% is applied which cannot, however, exceed a PASS (€46,368 in 2024). This will penalize very high incomes, since beyond a BNC of €178,338, the reduction is capped, regardless of the actual amount of social security contributions.

A little calculation to understand:

Currently a sector I doctor with a BNC of €80,000 pays around €16,000 in social security contributions (including 15,000 for CARMF). He therefore pays his CSG and his CRDS on a basis of €96,000. Let’s also remember that 30% of the CSG-CRDS total is not deductible! CSG-CRDS amount to €9,500, so the total with social security contributions is €27,500.

We therefore pay taxes on part of the CSG and the CSG on social contributions!

With the reform, the new levy base will amount to €96,000 x 74% or €71,000. Social security contributions (at the current rate) would be €15,000 including 14,100 for CARMF and 900 for URSSAF, and CSG-CRDS “only” €7,000, a total of €21,000 and a saving of €6,500.

If the rates don’t change, but I’ll come back to that later.

The same doctor with a BNC of €80,000 but in sector 2 pays him 30,000 € in social security contributions, so 22,000 from CARMF and 8,000 from URSSAF, plus 10,800 € from CSG-CRDS, so in total 40,800 €.

With the reform it has an overall basis of €110,000 x 74% or €81,400.

His social security contributions would then amount to €22,150 from CARMF and €8,150 from URSSAF (logical since his base increases by almost 2%).

On the other hand, the CSG-CRDS only represents €8,000, therefore a total of €38,300 and a gain of €2,500.

And for a Sector I doctor with a part of unconventional activity ? It’s very complicated, and you have to look at it on a case-by-case basis.

Except that nothing assures us that the rates will remain unchanged! For the CSG-CRDS we can think that they will not change, since they are the same rates for all labor income.

But for the health insurance or CAF contribution that could change.

For sector I doctors the impact would be very limited, since conventionally their health insurance “remaining cost” is 0.1% regardless of the actual rate (we paid the price when this rate was reduced from 9 .7 to 6.5% in 2016, but in the event of an increase it would protect us), and that the CNAM partly covers the CAF contribution.

On the other hand, sector II would completely suffer an increase in these rates, while their base is already increasing.

And for the CARMF, the DSS specifically provides for an increase of 1.7% in rates, to be distributed between the supplementary plan and the ASV. The more the increase concerns the ASV, the less sector I will suffer since the CNAM pays 2/3 of this contribution. But CARMF would prefer to increase the supplementary regime to increase reserves.

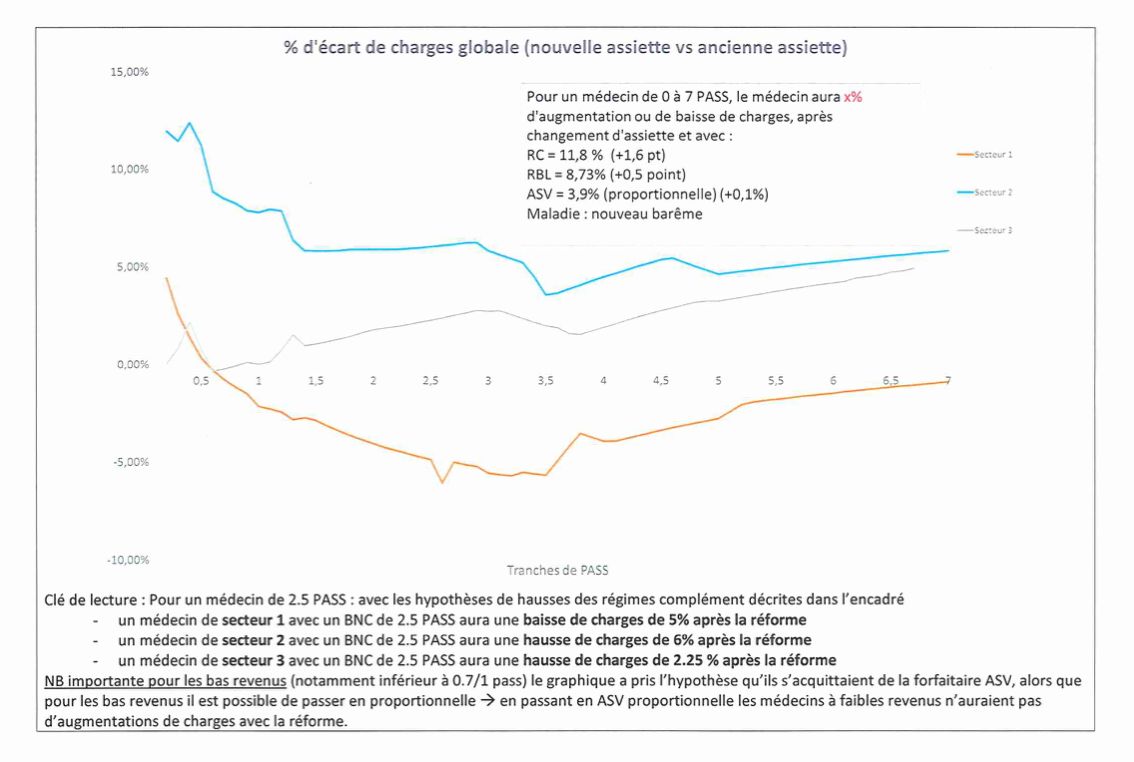

In fact, current CARMF projections show a drop in Sector I contributions of 2 to 5% compared to an increase of 5% for Sector II, as shown in this graph of current assumptions (which can still change and are subject to arbitration) .

In total :

- The calculation will be easier and (I hope) the DS PAMC too. But we will have to be extremely careful in 2025 and 2026 when calculating forecast contributions and regularizations for 2023 and 2024, since the calculation methods will be different.

- Almost all sector I doctors will find themselves winning (except very high incomes)

- It is much less obvious for sector II doctors, especially high incomes.

- Incidentally (but not that much), 2024 is the last year to redeem CARMF quarters of the basic plan and/or supplementary plan with an effect on actual contributions. From next year the flat-rate reduction will erase a large part of the financial advantage.

{kind=link}