The inflation episode that hit the Western world from 2020 after forty years of stable prices now seems to be a thing of the past. One after the other, central banks are confirming this new situation by lowering the interest rates that they had increased to combat rising prices.

After the ECB, which reduced its rates for the second time this year on Thursday, September 12, the American Federal Reserve (Fed) is expected to announce its first rate cut since March 2020 on Wednesday, September 18. But inflation has left its mark on the economy. What are they?

► Will prices return to their 2021 level?

The waltz of labels on supermarket shelves over the past three years has left its mark. Food products have seen their prices soar and weigh on household budgets. Since autumn 2021, the cumulative increase has climbed to more than 21%, which has hit consumers hard, especially those on the lowest incomes.

The worst seems to be over. Overall inflation fell below 2% on an annual basis for the first time in August in France, with food prices having calmed down to 1.7%. The first price drops appeared on the shelves at the end of last year. However, there has been no drop. “On average, prices are only falling by 1%,” according to Olivier Dauvers, specialist in mass distribution.

At this rate, the three years of inflation are not about to be caught up. In any case, we should not expect to ever return to pre-crisis prices. “They evolve according to the costs of raw materials and energy, two uncertain factors, and the cost of labor. However, the latter is always oriented upwards, which fuels inflation,” Olivier Dauvers analyzes.

The trend is still downward, however, and the coming months should still show reduced prices. A gap between official figures and consumer sentiment remains likely. While three-quarters of products have become cheaper in recent months, it is generally only by a few cents. “Prices are falling but, unfortunately, this is not yet reflected significantly enough in the total cost of a trolley”acknowledged the boss of Système U, Dominique Schelcher, at the end of August.

On the energy side, bills have been marked by the inflation episode, even if the French have been partly protected by the “tariff shield” put in place by the government. The price of gas is still twice its level before the Russian invasion of Ukraine.

On the electricity side, on the other hand, the decline is noticeable on the wholesale markets, with a return to the level of February 2022, which benefits businesses. Households will have to wait until February 2025 to benefit from a drop of around 10%. Fuels and domestic fuel oil have returned to their December 2021 level.

► Has the purchasing power of the French decreased?

Despite the inflationary episode, household budgets have not collapsed. Disposable income per consumption unit (DIPU), the indicator that best measures purchasing power, has held up on average: the 0.4% drop in 2022 was partly offset by a 0.3% increase last year.

But this development hides many disparities. The only real beneficiaries are at the top and bottom of the income scale. On the one hand, the richest 20% have seen their wealth income grow sharply; on the other, the poorest 10% have benefited from the increase in social benefits.

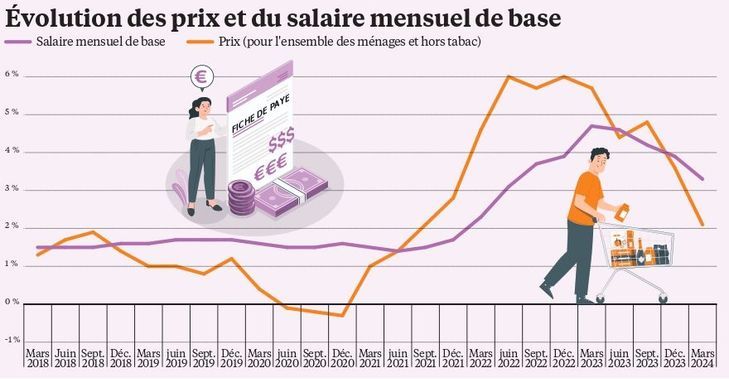

Between these two extremes are 70% of French people, who lose out from inflation. Their disposable income has shrunk by 0.3 to 0.7%. This can be seen in the drop in real wages, the labor income adjusted for inflation: between June 2021 and the end of 2023, the basic monthly wage (SMB) increased by 8.9% on average, while consumer prices increased by 11.3% – only those on minimum wages escaped this development, because their wage is indexed to prices.

Since the beginning of the year, however, the catch-up has been underway, with salaries increasing faster than prices. Deloitte notes that in the first half of the year, salaries increased by 3.5%, while inflation is expected to be limited to an average of 2.5% over the year.

“Unless there is a new external shock, the delay will be made up within six months to a year.says Stéphanie Villers, economist at PwC. However, given the weak growth, we should not expect spectacular increases.” Restoring purchasing power for all French people will take time. INSEE predicts an increase in gross disposable income per consumption unit of 0.9% in 2024.

► Can growth resume?

Can the inflationary episode that France and its European neighbors have just experienced, indirectly, revive French growth, considered particularly sluggish in recent years, around 1%? After the increase in interest rates carried out since the summer of 2022 by the European Central Bank to curb the waltz of labels, a second decrease occurred last week and others are planned.

“This will ease the constraints on real estate a little, because households will be able to borrow more easily, as will businesses,” points out Alexandre Baradez, at the broker IG France. According to him, “The Olympic effect will continue on tourism here next year,” which allows it to project “a recovery in activity in France in the coming months.” “But it will remain slight,” he emphasizes. The Bank of France announced on Tuesday, September 17 that it was forecasting growth of 1.1% in 2024 and 1.2% in 2025.

These few signs of optimism will face violent headwinds, adds Bruno de Moura Fernandes, head of macroeconomic research at credit insurer Coface: “French growth has held up since the beginning of the year, but mainly thanks to public spending, as household consumption and business investment are stagnating.”

The slippage in public accounts will lead the next government to budget cuts, economists predict, and perhaps to tax increases. “We predict a recession in France, explains Grégoire Kounowski, at Norman K. The political uncertainty created by the dissolution has in fact led businesses to freeze their investments and households to save at a record level. Without forgetting “the very poor health of the German and Chinese economies, and the strong commercial and geopolitical tensions.”

We must also take into account more structural factors that are holding back our growth potential: the decline in the birth rate and the structural decline in productivity. “Without increasing productivity, there is no solid growth, note the economists of the Pictet bank. This is really what is causing problems for our social model.”

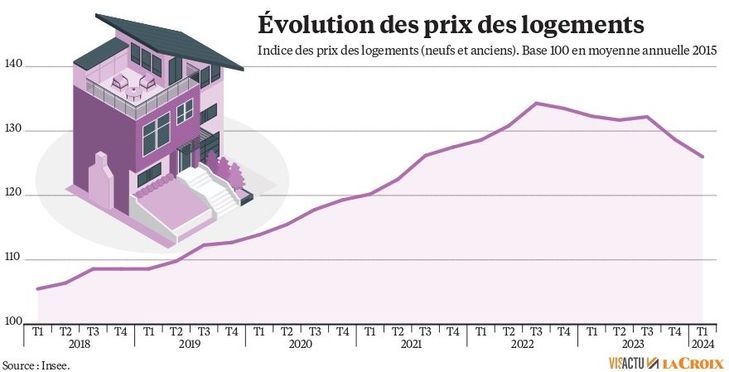

► Will the drop in rates affect real estate?

The second cut of the year in ECB interest rates, on Thursday 12 September, after the sharp rise linked to the inflationary crisis, brings some light to the real estate landscape, even if the banks have already anticipated the movement since the beginning of the year.

For a twenty-year loan, the average rate was trading at around 3.60% in August, compared to 4.30% at the end of 2023 and 4.45% a year ago. According to brokers, the decline should increase by the end of the year, with rates of 3 to 3.30% over twenty years. Starting next year, those who borrowed at 4% could even start to renegotiate their credit.

Real estate professionals are nevertheless remaining cautious, even though, according to notaries, the market has probably reached a low point this summer, after two years of decline. Guillaume Martinaud, the president of Orpi, prefers to speak of“a slowdown in the decline in sales agreement volumes“, down 8% over one year, in its network.

But the drop in rates, which gives buyers more purchasing power, could also encourage sellers to stop the decline in prices, or even revise their financial expectations upwards. At the end of August, prices in old properties were down by 4.8% on average over a year in France, and by 8.1% in Île-de-France, according to the notaries’ index.

The market is in any case incapable of responding to an increase in demand, given the slump observed in new construction, estimates Loïc Cantin, the president of the National Real Estate Federation (Fnaim), whose sales have plunged by 40% over a year.

Hence the urgency for the next government to put in place a housing plan. “There is unanimity among political parties and the French people on the subject,” wants to believe Olivier Salleron, the president of the French Building Federation (FFB). He advocates in particular the creation of a zero-rate loan (PTZ) or a reduced rate loan, “everywhere and for everyone”, and the extension of the Pinel system, for rental investment in new properties, which is due to end at the end of December.

► Will public finances continue to slip?

At first glance, inflation would not be a bad thing for public finances. Rising prices mean rising VAT revenues. And rising wages mean higher social security contributions and better income tax. In addition, by inflating the gross domestic product (GDP), inflation mechanically lowers the debt/GDP ratio: this is what France has seen, falling from 117.7% in the first quarter of 2021 to 111.8% in the fourth quarter of 2022.

“Both of these arguments are not wrong, but they miss important points,” However, a note from the General Directorate of the Treasury warned in July 2022.

Because inflation also leads to a revaluation of pensions, family or housing allowances and the RSA, indexed to prices. “Every additional point of inflation automatically increases these social expenditures by almost 5 billion euros,” noted the Treasury.

But it was especially the exceptional expenditure intended in particular to compensate for energy inflation that played a role. According to the Court of Auditors, shields, checks and compensation will have cost the State an additional 72 billion euros. Of course, the additional tax revenues have cushioned the expenditure by half, the rest, 36 billion, has increased the deficit. And therefore the debt…

But in the long run, debt doesn’t like inflation either. “A tenth of the debt” is at a variable rate, “indexed to inflation, so that each additional point of inflation results in an immediate increase in the apparent rate of about 0.1 point”estimates the Treasury. That is 2.5 billion more.

Between the increase in rates and the new expenditure, the debt burden has thus increased from 37 billion in 2021 to 50 billion in 2022, and is expected to reach more than 72 billion in 2027… “Such an increase does not pose a problem if nominal GDP increases in the same proportions”the Treasury acknowledges. Except that growth is not there.

——

An inflationary period unprecedented since 1985

In August 2024, inflation fell below the symbolic 2% mark for the first time since August 2021. As a reminder, inflation, on average over one year, reached +4.9% in 2023 and +5.2% in 2022.

These averages hide significant disparities. Thus, in 2022, energy prices had increased by 23% compared to 2021, and food prices by 7%.

Such an inflationary surge has not been observed since 1985. From 2002 to 2021, inflation only exceeded the 2.0% threshold, on average over the year, on four occasions (2003, 2004, 2008 and 2011).

To curb inflation, the European Central Bank, whose mission is to ensure price stability, had raised its rates ten times between July 2022 and September 2023, increasing its deposit rate from -0.5 to 4%. The institution had initiated a first reduction last June. Its American counterpart, the FED, which had done the same, is expected to announce a first reduction this Thursday, September 18.

{kind=link}