THE prix wheat have lost ground on Euronext between January 3 and 6, which had an impact on the walk French physics of soft wheat andbarley fodder. Corn prices closed the session stable to slightly down. On these two products, the rise in the single European currency has penalized export competitiveness.

To find out everything about agricultural market news, click here

Conversely, the decline of the dollar against other currencies boosted the prices of American cereals. THE wheat closed higher on the CBOT in Chicago, as well as Kansas City and Minneapolis. In winter wheat, concerns about winter temperatures in the state of Kansas, which concentrates a large part of the productionwere also playing on the rise. Temperatures remain very low, down to -20°C in certain areas of the UNITED STATES. In addition, precipitation remains scant and soils dry, the USDA reported in its weather bulletin. Figures ofexports weekly returns higher than expected in wheat also supported prices. In India, the country could resort to imports again. Wheat availability for millers are in fact increasingly rare, and the costs high, so that the mills are no longer working at full capacity, reports Reuters. However, the government had lowered the stocks authorized for millers in order to improve the circulation of goods in December. This also provided support for US wheat prices.

The prices of but were showing an increase on the CBOT in Chicago, supported like wheat by the fall in dollar. The taxation measures provided for by Donald Trump could ultimately concern fewer products and destinations than expected, which weighed on the greenback. Weekly corn exports were within expectations; with the cumulative total for the campaign reaching 24.5% more than the previous campaign, according to the USDA. Finally, the dry conditions in Argentine continue to push corn prices upwards.

In Ukrainedemand for corn was present but limited in recent weeks, which kept prices stable, according to Ukragroconsult.

To find out everything about the latest news from professionals in the grain sector, click here

Commerce international :

- United States, wheat, exports : 412,342 t for the week ending January 2 (source: USDA)

- United States, corn, exports : 847,463 t the week ending January 2, i.e. -6.6% from one week to the next and -22.4% compared to the same period in 2023-2024; for a total of 16,236 Mt over the current campaign (source: USDA)

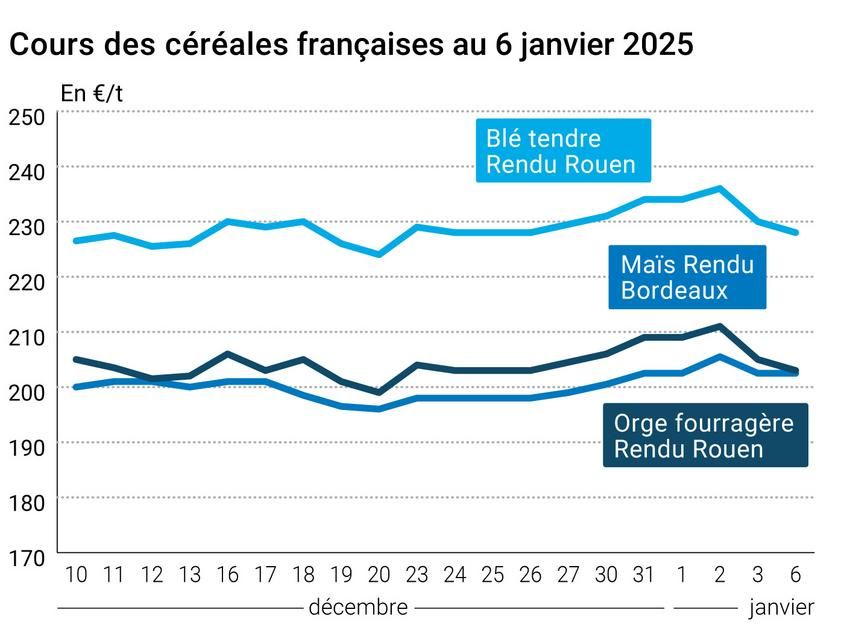

French physical markets from January 6, 2025 (July base for cereals)

| Soft wheat | Specifications | Due date | euro/t | | Variation |

| Dunkirk rendering | 220/11 miller Harvest 2024 | Jan-Mar | 228,50 | N | -2,00 |

| Rendering La Pallice | 76/220/11 Harvest 2024 | Jan-Mar | 226,00 | N | -2,00 |

| Rendering Rouen | 76/220/11 Harvest 2024 | Jan-Mar | 228,00 | N | -2,00 |

| Pontivy/Guingamp rendering | forage 74 kg/hl base, 72 kg/hl mini Harvest 2024 | Jan-Mar | 224,00 | N | -2,00 |

| Fob Moselle | miller Harvest 2024 | Jan-Mar | 235,00 | N | 2,00 |

| Fob Rouen | FCW Superior A2 class 1 major. included Harvest 2024 | Jan. | n.p. | | |

| | FCW Medium A3 class 2 majo. included Harvest 2024 | Jan. | inc. | | |

| Fob La Pallice | FAW Superior A2 class 1 major. included Harvest 2024 | Jan. | n.p. | | |

| Departure from Marne | BPMF 220 Hagberg Harvest 2024 | Jan-Mar | 229,00 | N | -2,00 |

| Departure from Eure/Eure-et-Loir | BPMF 76 kg/hl Harvest 2024 | Jan-Mar | 222,00 | N | -2,00 |

| Departure South-East | miller Harvest 2024 | Jan-Mar | 238,00 | N | 0,00 |

| Durum wheat | Specifications | Due date | euro/t | | Variation |

| Rendering Port-la-Nouvelle | semolina standards Harvest 2024 | Jan-Mar | 295,00 | N | 0,00 |

| Departure from Eure/Eure-et-Loir | semolina standards Harvest 2024 | Jan-Mar | 287,50 | N | 0,00 |

| Departure South-East | semolina standards Harvest 2024 | Jan-Mar | 285,00 | N | 0,00 |

| But | Specifications | Due date | euro/t | | Variation |

| Bordeaux rendering | Harvest 2024 | Jan-Mar | 202,50 | N | 0,00 |

| Rendering La Pallice | Harvest 2024 | Jan-Mar | 210,00 | N | 0,00 |

| Pontivy/Guingamp rendering | Harvest 2024 | Jan-Mar | 208,50 | N | 0,00 |

| Fob Bordeaux | Harvest 2024 | Jan-Mar | 206,50 | N | 0,00 |

| Fob Rhin | Harvest 2024 | Jan-Jun | 218,00 | N | -3,00 |

| Departure South-East | Harvest 2024 | Jan-Mar | 217,50 | N | 0,00 |

| Feed barley | Specifications | Due date | euro/t | | Variation |

| Rendering Rouen | 62-63 kg/hl Harvest 2024 | Jan-Mar | 203,00 | N | -2,00 |

| Pontivy/Guingamp rendering | Harvest 2024 | Jan-Mar | 206,00 | N | -2,00 |

| Fob Moselle | without limit. orgettes Harvest 2024 | Jan-Mar | 188,00 | N | -2,00 |

| Departure from Eure/Eure-et-Loir | Harvest 2024 | Jan-Mar | 192,00 | N | -2,00 |

| Departure South-East | 62/63 kg/hl Harvest 2024 | Jan-Mar | 215,00 | N | 0,00 |

| Malting barley – Winter 6 rows | Specifications | Due date | euro/t | | Variation |

| Fob Creil | Faro 11.5% max Port 500 t Harvest 2024 | Jan-June | 223,00 | N | 0,00 |

| Malting barley – Spring | Specifications | Due date | euro/t | | Variation |

| Fob Creil | Planet 11.5% max Port 500 t Harvest 2024 | Jan-June | 242,00 | N | 0,00 |

| Sunflower | Specifications | Due date | euro/t | | Variation |

| Bordeaux rendering | oleic Harvest 2024 | Jan-Mar | 630,00 | N | 0,00 |

| Rendered Saint-Nazaire | oleic Harvest 2024 | Jan-Mar | 630,00 | N | 0,00 |

| Rapeseed | Specifications | Due date | euro/t | | Variation |

| Rendering Rouen | Harvest 2024 | Apr-June | 510,50 | N | 1,50 |

| Fob Moselle | Harvest 2024 | Apr-June | 512,50 | N | 1,50 |

| Soybean meals | Specifications | Due date | euro/t | | Variation |

| Departure Montoir | 48% pellets Brazil | Jan. | 381,00 | V | -7,00 |

| | 48% pellets Brazil | February 3 | 381,00 | V | -7,00 |

| Then | Specifications | Due date | euro/t | | Variation |

| Departure from Marne | forage Harvest 2024 | Jan-Mar | 295,00 | N | 0,00 |

| Departure from Somme/Oise | forage Harvest 2024 | Jan-Mar | 295,00 | N | 0,00 |

Quotations of milling products from December 31, 2024

| Its fine soft wheat | Specifications | Due date | euro/t | | Variation |

| Departure from Ile-de-France | | available. | 144,00-146,00 | T | |

| | pellets | available. | 154,00-156,00 | T | |

| Half-white remolding | Specifications | Due date | euro/t | | Variation |

| Departure from Ile-de-France | | available. | 164,00-166,00 | T | |

| Low flour | Specifications | Due date | euro/t | | Variation |

| Departure from Ile-de-France | | available. | 169,00-171,00 | T | |

Commercial quotations for dairy products from January 2, 2025

| Milk powder | Specifications | Due date | euro/t | | Variation |

| | NBPL departure at 30 days 5% H BT bulk | available. | 2490,00 | N | |

| Whey powder | Specifications | Due date | euro/t | | Variation |

| | NBPL departure at 30 days, BILA pH 6 bulk | available. | 865,00 | N | |

Dollar/euro evolution of January 6, 2025

| Devise | Closing value |

| 1 dollar US | 0,9591 euro |

| 1 euro | 1,0426 dollar |

Chicago Futures Market Close January 6, 2025

| Raw materials | Fence | Chicago |

| Wheat | 540,50 | cents/wood. |

| But | 457,75 | cents/wood. |

| Ethanol | 2,161 | $/gallon |

| Military | 992,50 | cents/wood. |

| Soybean meals | 298,60 | $/t |

| Soybean oil | 39,76 | cts/livre |

Closing of the Euronext futures market on January 6, 2025

| Milling wheat (Euronext) |

| Echéance | Fence |

| Mars 2025 | 231,25 |

| May 2025 | 235,75 |

| Sept. 2025 | 226,75 |

| Volume | 50277 |

| Corn (Euronext) |

| Echéance | Fence |

| Mars 2025 | 209,75 |

| June 2025 | 217,00 |

| August 2025 | 221,75 |

| Volume | 2656 |

| Colza (Euronext) |

| Echéance | Fence |

| Feb. 2025 | 513,75 |

| May 2025 | 511,50 |

| August 2025 | 473,50 |

| Volume | 19681 |

| Rapeseed oil (Euronext) |

| Echéance | Fence |

| Mars 2023 | 698,50 |

| June 2023 | 698,50 |

| Sept. 2023 | 698,50 |

| Volume | 0 |

| Rapeseed meal (Euronext) |

| Echéance | Fence |

| Mars 2023 | 196,25 |

| June 2023 | 196,25 |

| Sept. 2023 | 196,25 |

| Volume | 0 |

| European Union Wheat (CME) |

| Echéance | Fence |

| Sept. 2018 | 159,25 |

| Dec. 2018 | 163,25 |

| Mars 2019 | 164,75 |

| Volume | 0 |

International market quotes from January 6, 2025

| Energy | Echéance | Closing value |

| Oil (Nymex) | Feb. 2025 | 73,56 $ |

| Ocean freight indices | from January 6 | Variation |

| Baltic Dry Index (BDI) | 1043 | -29,00 |

| Baltic Panamax Index (BPI) | 1061 | 21,00 |

| Baltic Capesize Index (BCI) | 1290 | -85,00 |

| Baltic Supramax Index (BSI) | 867 | -17,00 |

| Baltic Handysize Index (BHSI) | 539 | -10,00 |