The role of gold in a portfolio has always caused great controversy. On the one hand, proponents emphasize the importance of the precious metal as a key element of diversification, also serving as a refuge against inflation, international conflicts and civil unrest. On the other hand, detractors believe that gold is a relic of an ancient time, an unproductive commodity with limited utility and little tangible value.

In recent years, there is no denying that gold has strengthened diversified global portfolios. In fact, gold reached $2,615 per ounce, recording consecutive multi-month highs. Since the pandemic, gold has outperformed most other major asset indices, including global stocks, government bonds and commodities.

Asset returns since the Covid-19 pandemic

(% change for different assets since December 2019)

Sources: Bloomberg, QNB analysis

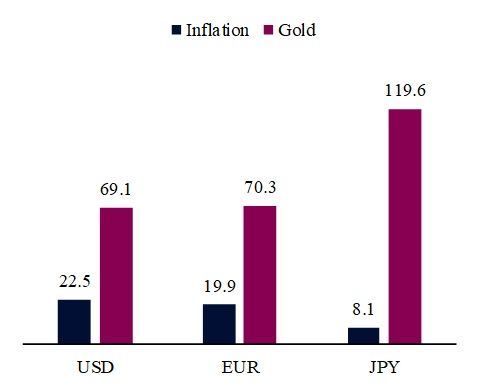

Importantly, gold has recently demonstrated its enduring value as a hedge against inflation. Following the Covid-19 pandemic, monetary authorities in advanced economies have faced significant challenges due to a sharp rise in inflation. This raised concerns about the rapid rate of decline in the “real value of money” as more units of currency would be needed to purchase the same basket of goods and services. Not surprisingly, during this period of high inflation, gold prices rose against most major currencies, more than offsetting the effect of consumer price increases. This offered a compelling affirmation of the well-established belief that gold is an effective hedge against inflationary pressures.

Post-pandemic accumulated inflation vs. gold returns

(% change for different currencies since December 2019)

Sources: Haver, QNB analysis

However, as disinflation progresses thanks to the normalization of supply chains, can gold continue to perform well in the medium term? Is the shiny yellow metal about to experience a correction or a period of significant underperformance?

In our view, despite a largely normalized inflation outlook in most advanced economies, global macroeconomic conditions remain supportive for gold. Three main factors support this position.

First, the monetary policy cycle in the US and Europe is now a driver for gold prices. In recent years, cash or short-term government securities offered high nominal yields, thereby increasing the opportunity costs of holding gold. Although nominal yields still remain well above pre-pandemic levels in most advanced economies, this dynamic is expected to change significantly over the next 24 months. The US Federal Reserve and the European Central Bank are expected to lower their key rates by 250 and 150 basis points, respectively. This means that cash and short-term government securities will be less attractive as investment options, favoring alternative investments such as gold.

Second, currency movements are also expected to play a role in supporting gold prices. Historically, gold prices are inversely correlated to the United States dollar (USD), with gold prices rising when the dollar falls, and vice versa. One assessment of the dollar indicates that it is overvalued by about 9%, requiring a significant adjustment. A weaker dollar increases the rest of the world’s purchasing power for USD-denominated commodities, such as gold, boosting overall demand and supporting prices.

Third, the current global economic environment remains marked by geopolitical uncertainties, such as the Russo-Ukrainian war, ongoing conflicts in the Middle East, and growing tensions between the United States and China in the Pacific. These factors can increase the risk premium of traditional assets, pushing investors to turn to alternative hedging instruments. Gold’s appeal has been enhanced by long-term trends, such as intensifying economic rivalry between West and East, decreasing international cooperation, increasing trade disputes, escalation of political polarization, and the “militarization” of economic relations through sanctions.

In an era of greater geopolitical instability, gold’s status as a tangible, jurisdiction-neutral asset that can serve as collateral in various markets is becoming increasingly important. Reflecting this trend, global central banks are accumulating gold at a rate not seen in generations, supporting stable long-term institutional demand.

In summary, despite rapid global disinflation and significant gains by gold in recent years, global conditions remain favorable for the precious metal. Gold prices are expected to be further supported by easing monetary policy from major central banks, dollar depreciation and geopolitical divides.

– Advertisement-