According to economists, the Bank of Canada will not give borrowers a big gift

Published at 5:00 a.m.

Recent reductions in the key interest rate by the Bank of Canada have brought relief to many borrowers.

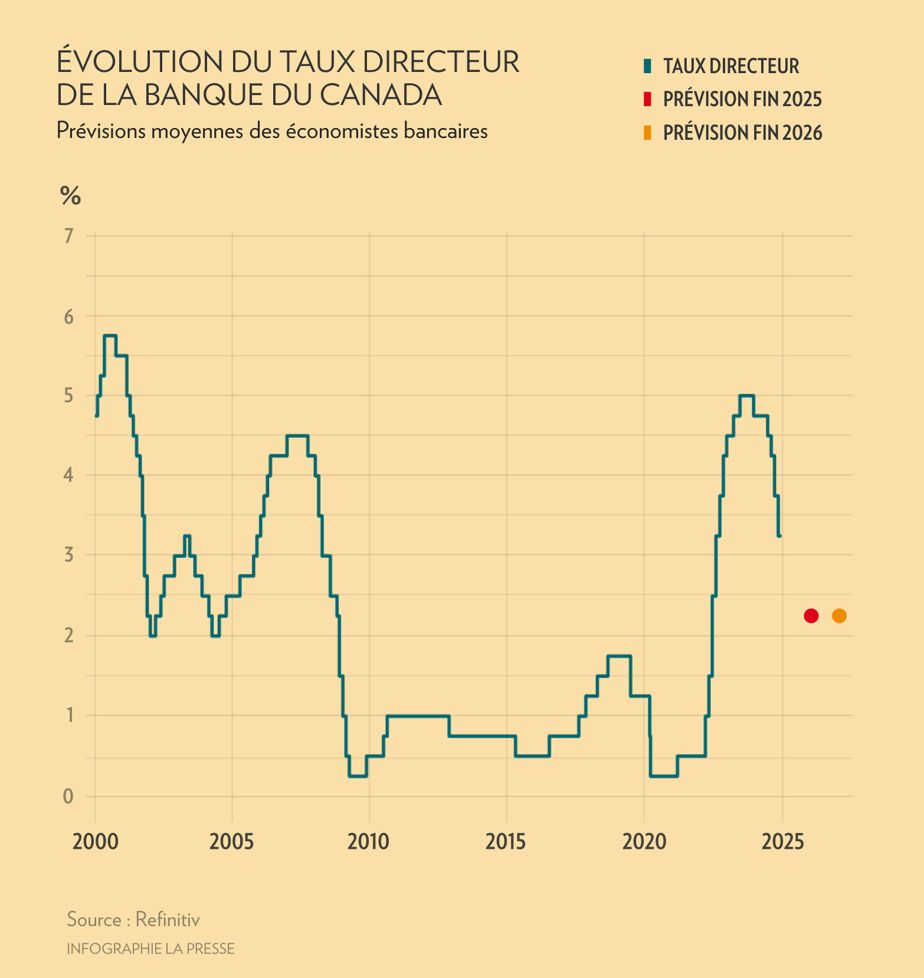

As a reminder of 2024: after jumping from 0.25% to 5% between February 2022 and June 2023, the key rate was lowered by 175 basis points (1.75%) in a few months, to 3.25 % in mid-December.

Obviously welcome, this drop in the key rate has also revived the hope of a return to interest rates as low as those which had prevailed since the beginning of the 2010s. And even towards even lower rates – the rate director at 0.25% – established in 2021 and 2022 by the Bank of Canada, in order to counter the economic crisis linked to the pandemic.

However, in the opinion of banking economists, this hope of a return to very low interest rates should be relegated to oblivion!

In fact, they expect a few more policy rate cuts in the coming months. But these are declines which, in the absence of sudden and major disruptions in the economy, should end at around 2.25% at the end of 2025 and for the following year, in 2026.

“An important consideration for borrowers is that the prospect of even lower interest rates is now slim, especially for longer-term borrowing,” says Jean-François Perrault, senior vice-president and economist. chief at Scotiabank, in his recent update of the economic and financial outlook.

“From the perspective of a potential home buyer, you should no longer expect much lower interest rates on five-year term mortgages. In fact, what we observe in the financial markets is that the next reductions in interest rates will be very limited and much more concentrated on loans with short maturities (less than three years) and at interest rates variable or preferential. »

INFOGRAPHICS THE PRESS

Change in monetary policy

Although disappointing for borrowers’ expectations, this attenuation of interest rate cuts must also be considered in the context of the recent and rapid turnaround in monetary policy.

“In just six months, the Bank of Canada has reduced its base interest rate from a very restrictive 5% to the upper limit of its estimate of a rate considered neutral for economy, or approximately 3.25%, reported Douglas Porter, chief economist at the Bank of Montreal (BMO), following the central bank’s most recent monetary policy statement in mid-December.

PHOTO TAKEN FROM THE BANK OF MONTREAL SITE

Douglas Porter, chief economist at the Bank of Montreal

Moving forward, the Bank of Canada has clearly indicated that the pace of rate cuts will slow considerably during its next monetary policy meetings. But on condition that the economy does not hold any major surprises – negative or positive – in the coming quarters.

Douglas Porter, chief economist at the Bank of Montreal

Similar observation from Randall Bartlett, senior director of analysis of the Canadian economy at Desjardins Group.

“Reduced to 3.25%, the Bank of Canada’s key interest rate is now close to a so-called “neutral” rate for the economy, i.e. the rate estimated when inflation is at 2% and the production level is returning to the long-term trend,” according to Mr. Bartlett.

“In other words, this implies that the Bank of Canada’s monetary policy is no longer ‘restrictive’ for the economy. For this reason, I don’t expect any further significant rate cuts in the foreseeable future. »

Back to normal?

In this context, what consolation for borrowers still nostalgic for very low interest rates? “Central banks do not always adopt the policies we would like. But sometimes they are what we need,” points out Pierre-Benoît Gauthier, vice-president of investment strategy at the firm IG Gestion de Patrimoine, in his recent update of the economic and financial outlook for the new year.

“While interest rates still appear high compared to those of just three years ago, they have in fact returned close to their long-term historical averages, including rates seen in the years 2000 [taux directeur moyen autour de 3,25 %]and before the financial crisis of 2008. This observation reinforces the point of view according to which we are returning to an “old normal” in terms of interest rates,” according to Mr. Gauthier.

“While rapid rate cuts can relieve pressures on mortgage costs, they are also considered to generate economic risks,” recalls Beata Caranci, senior vice-president and chief economist at TD Bank.

PHOTO TAKEN FROM TD BANK SITE

Beata Caranci, Senior Vice President and Chief Economist at TD Bank

Among other things, rate cuts encourage demand for residential real estate and accelerate consumer spending, which can fuel inflationary pressures in the economy.

Beata Caranci, Senior Vice President and Chief Economist at TD Bank

For example, Mme Caranci recalls the episode of overheating of the residential real estate market which occurred at the end of 2020 and in 2021.

“After the Bank of Canada lowered its key interest rate to near zero [0,25 %, pour contrer la crise pandémique]home sales jumped 40% in just 12 months. Homebuyers have reacted strongly to a once-in-a-generation record drop in mortgage rates. »

Furthermore, points out the chief economist of TD Bank, “pronounced rate cuts can weaken the Canadian dollar on the international currency market. A weak Canadian dollar increases the cost of imported goods and services. It can also become counterproductive for companies’ investments in machinery and equipment from other countries.”

The Bank of Canada ahead

As an additional comfort, those nostalgic for very low interest rates can perhaps console themselves with the fact that the Bank of Canada, after two consecutive rate cuts of 0.5% at the end of 2024, is l One of the most aggressive central banks with rate cuts among developed economies.

“No other G10 central bank has cut rates by more than 125 basis points (1.25%) in 2024. Even the US Federal Reserve (Fed) has limited itself to cuts totaling 75 basis points (1.25%). basis (0.75%) until mid-December 2024,” recalls Douglas Porter, chief economist at the Bank of Montreal (BMO).

In return, this eagerness of the Bank of Canada to lower its key interest rate during the second half of 2024 is considered one of the main factors in the devaluation of the Canadian dollar compared to the US dollar.

At the height of the rate cuts, from September to the end of December, the value of the Canadian dollar fell from 74.5 US cents to 70.3 US cents.

The Canadian loonie is thus trading at its lowest level since March 2020, when the economy was hit hard by the COVID-19 pandemic.

For the travelers and vacationers among you, be warned: the exchange rate could surprise you during your next stay outside Canada!