“Simply Put”, the weekly column from the Multi Asset Group team at Lombard Odier Investment Managers

By Florian Ielpo, Head of Macro and Aurèle Storno, Multiasset CIO

In summary:

- Markets have recently shown themselves to be more sensitive to political risk, particularly following the result of the European elections. This resulted in increased volatility of French assets.

- The political turbulence spread more widely across European markets, causing European stocks and credit to significantly underperform over a few days.

- Faced with this increase in volatility, the asset allocation of our All Roads strategy has been adjusted by reducing exposure to French OATs. Further adjustments are anticipated if political risk were to increase.

Following the European elections, markets began to price in increased political risks. This notably resulted in a questioning of the high valuations of European equities, as well as a widening of credit spreads which had hitherto been on a downward trend. This increase in political risk mainly originates from the early legislative elections initiated by President Macron. Additionally, over the past week, European stocks have underperformed their US counterparts. We have already experienced similar scenarios in the past – the Cypriot crisis, the Scottish referendum or the 2017 French elections – during which these impacts proved to be transitory, marked by a peak in volatility before a return to market sentiment. more favorable to risk taking. The crucial question now is: how worrying is this situation, and above all, what is the extent of the market pricing of this political risk?

A French problem, not a European one?

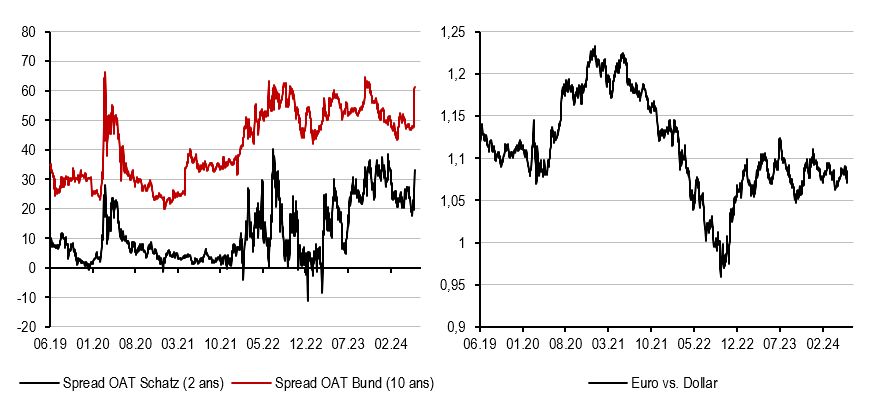

First of all, investors should keep in mind that the large coalitions forming the European Parliament have seen little change in their number of seats. Notably, the central EPP group retains 192 seats – at most, the European Parliament has experienced a slight shift towards the right of the political spectrum. The situation is different in France, however: with the victory of the National Rally with more than 30% of the vote, President Macron called for early elections of the National Assembly, in an attempt to regain legitimacy. This scenario is reminiscent of Cameron’s situation in the United Kingdom, where the European referendum was treated as a vote of confidence in the Prime Minister, which ended in a bitter failure. The RN, known for its anti-European program and its desire to increase rather than reduce state spending, leads many observers to see in this situation a cocktail between Liz Truss’s failed budget and Cameron’s European referendum. . France is, with Germany, a historic pillar of the European Union and this situation has been reinforced since the departure of the United Kingdom: France is not Europe, but an increase in the risk of Frexit could shake European markets. With the result of the election, the French risk premium increased significantly, as evidenced by the gap between the yields of French and German bonds (cf. Figure 1). Notably, the EUR/USD has only fallen slightly: it therefore does not seem to be a systemic problem for Europe at the moment, but rather an issue centered on France. Are we sure?

Figure as of June 18, 2024

A political contagion?

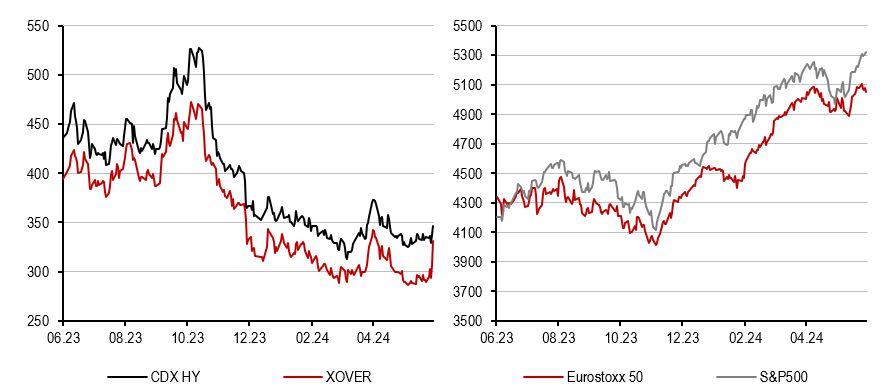

That’s not entirely correct. The European nature of risk is not really reflected in the Euro itself, but manifests itself somewhat elsewhere. In particular, by comparing the evolution of the XOVER spreads in Europe and the CDX HY in the United States, the difference in trajectory is rather obvious: as shown in the Figure 2, XOVER spreads widened four times more than the CDX HY, even reaching an increase of 40 basis points as of last Friday. The joint progression of these two indices demonstrates how this increase in political risk affects the market more broadly. The same can be said for stocks: here again, Figure 2 illustrates a marked gap between the Eurostoxx and the very robust S&P 500 at the end of last week. What this rise in political risk seems to be generating is a return of investors to positions that were successful last year: American stocks and particularly technology stocks – why look elsewhere for what lies so naturally beneath our eyes? What all these charts currently show is how a political risk factor – usually transitory in nature – spreads through markets. It would probably be wrong to underestimate it too quickly, and to think that it will only impact bond spreads. With government bond spreads widening, the ECB could step in if risk becomes systemic for Europe, but with European stocks underperforming there is little it could do – a risk factor which we continue to monitor carefully.

What this means for All Roads

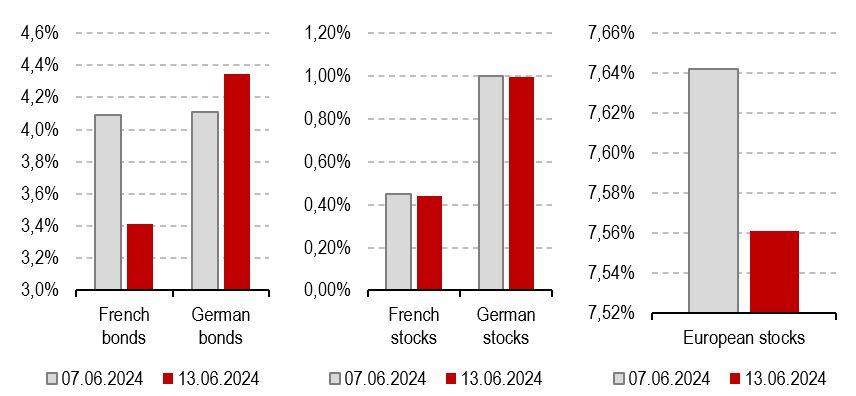

What this means for our All Roads strategy is quite simple to understand: in the face of increasing risks, our risk management models have started to respond. As risk-conscious investors, we know that maintaining diversification generally means being less invested in riskier assets and more in those with a lower level of risk. When proven risk increases, our allocation begins to adjust, as illustrated in Figure 3 below. For now, the increased volatility is occurring primarily in the bond markets, and this is where our reallocation has been most substantial. In the “balanced” strategy profile, we have slightly reduced our allocation to French OATs by 1%, while our equity allocation has remained stable for the moment. If the rise in risk continues, the natural rebalancing of risks in our portfolio will also continue.

Figure as of June 17, 2024

Simply put, the situation in France threatens to have a wider impact on European risk – investors aware of their risks should take this into account.

Macro/Nowcasting Corner

This section brings together the most recent developments in our nowcasting indicators for global growth, global inflation surprises and global monetary policy surprises. These indicators make it possible to monitor the most recent macroeconomic developments that move the markets.

Our nowcasting indicators currently indicate:

- Our growth signal increased this week as more positive data was published in the United States.

- The message from our inflation indicator remains the same as in previous weeks: the inflation risk is gradually resurfacing, mainly in the United States.

- Our monetary policy signal continues to anticipate a moderately “dovish” tone from central banks.

Show article disclaimer

For the exclusive use of professional investors

This document is published by Lombard Odier Asset Management (Europe) Limited, authorized and regulated by the Financial Conduct Authority (the “FCA”), and registered with the FCA under number 515393.

Lombard Odier Investment Managers (“LOIM”) is a trading name.

This material is provided for informational purposes only and does not constitute an offer or recommendation to buy or sell any security or service. It is not intended for distribution, publication or use in any jurisdiction where such distribution, publication or use would be unlawful. This material does not contain personalized recommendations or advice and is not intended to replace professional advice regarding investing in financial products. Before entering into any transaction, the investor should carefully consider the suitability of the transaction for its particular circumstances and, if necessary, obtain independent professional advice on the risks, as well as the legal, regulatory, tax and accountants. This document is the property of LOIM and is addressed to its recipient exclusively for their personal use. It may not be reproduced (in whole or in part), transmitted, modified or used for any other purpose without the prior written permission of LOIM. This document contains the opinions of LOIM, as of the date of issue.

Neither this document nor any copy of it may be sent, introduced or distributed into the United States of America, any of its territories or possessions or areas subject to its jurisdiction, or to or for the benefit of ‘a person of the United States. For this purpose, the term “United States person” means any citizen, national or resident of the United States of America, any partnership organized or existing in any state, territory or possession of the United States of America. America, any corporation organized under the laws of the United States or any state, territory, or possession thereof, or any estate or trust subject to United States federal income tax United, whatever the source of its income.

Source of figures: Unless otherwise stated, figures are prepared by LOIM.

Although certain information has been obtained from public sources believed to be reliable, without independent verification we cannot guarantee its accuracy or the completeness of any information available from public sources.

The views and opinions expressed are for informational purposes only and do not constitute a recommendation by LOIM to buy, sell or hold any security. Views and opinions are current as of the date of this presentation and may be subject to change. It should not be construed as investment advice.

No part of this material may be (i) copied, photocopied or duplicated in any form, by any means, or (ii) distributed to any person who is not an employee, officer, director or an authorized agent of the recipient, without the prior consent of Lombard Odier Asset Management (Europe) Limited. In the United Kingdom, this material is marketing material and has been approved by Lombard Odier Asset Management (Europe) Limited which is authorized and regulated by the FCA. ©2022 Lombard Odier IM. All rights reserved.

{kind=link}