According to the Jones Lang LaSalle 2025 study, new construction activity has reached its lowest point. A recovery is expected in the investment market.

Jones Lang LaSalle (JLL) publishes its new study on the office real estate market in Switzerland. The report provides a comprehensive overview of the office space market in Zurich, Geneva, Bern, Lausanne, Basel and Zug. In addition to the key figures and the main changes observed in the most important regions, the office real estate study also offers an analysis of the availability of ESG-compliant space and presents a brief overview of the real estate market in European office.

In the five largest office real estate markets in Switzerland – Zurich, Geneva, Bern, Basel and Lausanne (CH%) – the supply of available office space increased by 9% compared to the previous year, totaling 995,500 m² at the end of 2024. This means that the volume of available office space has continued to increase in recent years. Since the end of 2019, when teleworking was still uncommon in many places, the average supply rate in the five largest Swiss office markets has increased from 4.1% to 5.0% at the end of 2024 (+0. 9%). However, this increase must be put into perspective in international comparison, because the average vacancy rate in 24 European cities increased from 5.2% to 8.5% (+3.3%) over the same period.

Despite the completion of 1.16 million m² of new office space since 2020, the increase in supply remains moderate, with only 231,000 m² additional over the same period. Construction activity reached a peak in 2020 with around 343,000 m² of new office space, then gradually decreased to reach 57,000 m² in 2024. A gradual resumption of the creation of new office space is expected between 2025 and 2027.

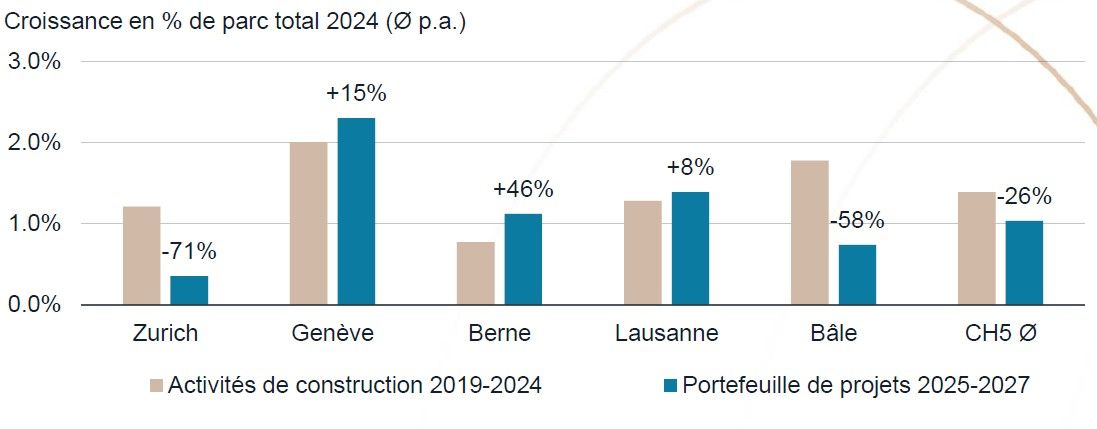

Market dynamics vary considerably by region. Geneva stands out with the strongest growth, averaging 2.0% in stock between 2019 and 2024, which is expected to accelerate to 2.3% by 2027. Bern is seeing a significant rise in construction activity , but its future growth, estimated at 1.1% per year, will only slightly exceed the Swiss average. Conversely, Zurich and Basel respectively plan 71% and 58% less new space by 2027 compared to the period 2019-2024. Overall, for the top five markets, average annual office stock growth is forecast at 1.0% through 2027, down 26% from the previous period, reflecting regional disparities and divergent trends. of the Swiss office real estate market.

Overall, demand for space remains strong. However, marketing vacant spaces in old buildings, far from stations, remains a challenge. Conversely, the market is relatively quickly absorbing modern, flexible, ESG-compliant office space with good connectivity. This is particularly reflected in the limited supply in these locations.

In district 1 of Zurich, 3.0% of office space is available, compared to 1.5% in the CBD of Lausanne and only 0.4% in the city center of Bern. Supply is also scarce in the cities of Lucerne (1.3%), Zug (1.7%), Freiburg (2.0%) and Lugano (2.1%). The CBD of Geneva displays a greater offer with 3.9% availability. In Basel, the vacancy rate reached 9.2% in the city center.

Transaction market

The outlook for office real estate in Switzerland is mixed. On the one hand, vacancy rates have recently increased slightly, and investors remain cautious due to uncertainty over future space requirements linked to more flexible work concepts. On the other hand, robust economic and employment growth supports demand, and the Swiss office market has proven its strong resilience. Additionally, rents are protected against inflation and, unlike the residential rental market, the risk of political intervention in the commercial market is limited.

Many investment funds and foundations carried out capital increases in the second half of 2024 and will enter the new year with significant liquidity. Their investment strategy should focus on “core” properties located in the attraction areas of urban centers, not requiring renovation and ideally meeting the required sustainability criteria. In recent weeks, a greater willingness to pay coupled with an overall broader interest has been noticeable. This trend, coupled with a lower interest rate environment, is expected to lead to compressed yields and increased trading volumes this year.

Jan Eckert, CEO Switzerland & Head Capital Markets DACH at JLL, says: “Many market participants are optimistic about the coming months and want to take advantage of the improved investment environment to carry out transactions. We observe this trend both in the quantity and quality of the offers received. The short-term outlook is more favorable than it has been in three years.”