After 2 years of gains of more than 20%, the correction of the S&P 500 is still awaited. A century of data on the S&P 500 allows us to compile statistics on the frequency and magnitude of corrections. But at this point, Wall Street is only looking up.

An impressive rise that leaves us no time to catch our breath. This is the feeling that the S&P 500 has left you with for 2 years. This is also the reality of the figures. The 60% increase in the index since its low point in October 2022 occurred without correction, that is to say without a drop of at least 10%. And with a clear increase in valuation multiples.

Let’s put things in order. As of October 2022, the S&P 500 is down 25% for the year. The sequence of rate hikes started by the Fed has hurt valuations. What follows is a 60% increase against a backdrop of American exceptionalism and artificial intelligence. And only 2 “breaths”. Between the summer and fall of 2023, the S&P fell by 9.85%, penalized by the rise in long-term rates. 150 basis points in just over 4 months for the American 10-year, and a peak at 5%; a painful level for the stock markets.

The summer of 2024 was also chaotic. A very beautiful sequence that many speakers experienced…from their vacation spot. The Fed decided on July 31 not to reduce its rates because everything is going well in the best of all possible worlds. 2 days later, an employment report comes out well below expectations. The market narrative is completely changing. The Fed is late and we urgently need to lower rates. The market is starting to fall and the unwinding of carry-trade positions is increasing the pressure. But more fear than harm. Between mid-July and early August, the decline was contained at 8.49%.

Historical anomaly?

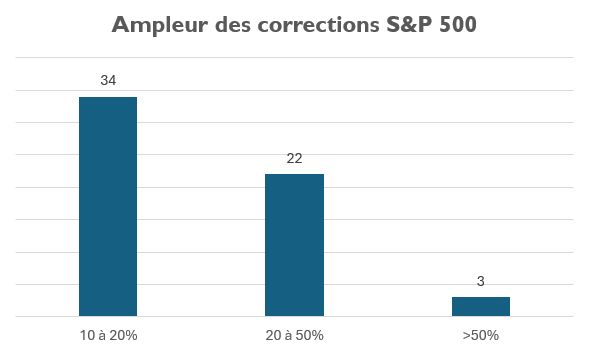

To know if the current period is out of the ordinary, you have to study the history of the S&P500. Since 1928, the flagship index of the New York Stock Exchange has experienced 56 correction phases. That is approximately one every 18 to 24 months, for an average drop of 23%. The last one was between August and October 2022. A correction of just over 16%, just before starting the formidable rally that we are experiencing. 27 months separate us from the start of the bull market. Statistically, the index is therefore ripe for a correction. Except that the vast majority of strategists predict a rise in the S&P 500 in 2025. But as the adage goes, the consensus is always wrong. Or the year will be eventful.

Buy the dip

From a historical point of view, the current period is therefore not completely an anomaly. But we can still be concerned about the pace of the increase and the confidence of investors in this stock market. According to the Conference Board’s November survey, Americans have never been so bullish on stocks. On the same theme, cash positions in portfolios are at their lowest since the beginning of the century while exposure to US equities is at its highest, according to the latest Bank of America survey of managers.

And those who find that market levels are high are just waiting for a correction to return. This “buy the dip” logic is very present in investor psychology. Indeed, stocks go up over the long term so buying dips doesn’t seem stupid. When the markets are high, everyone waits for the decline to return. But when the withdrawal happens, something is happening and no one wants to get in front of it anymore. No one knows when this decline will arrive or even if it will arrive in 2025. For the moment, the American market is still driven by its “animal spirit”. To quote a socialist president, you have to believe in the forces of the spirit.