Activity is holding up well and inflation is rising again, leading to a tightening of the Fed’s rhetoric. In the euro zone, consumption has rebounded and the conditions for a continued recovery seem to be ripe.

Although it shows, as expected, a clear rebound in job creation, the November report has not allayed all concerns about the evolution of employment in the United States, with a household survey much weaker than that of businesses. Indeed, while job creations in the business survey rebounded to 227,000 in November, correcting the effects of storms and strikes, the household survey showed a drop of 355,000.

As the unemployment rate is calculated on the basis of the household survey, it increases again to reach 4.25%, a level very close to the high point of last July. However, as shown by the low level of weekly unemployment registrations, the increase is not explained by job losses but more by the increasing difficulty of the unemployed in finding a job. Additionally, the employment components of the surveys are starting to recover.

Another reassuring element for the American economy: surveys reveal a clear improvement in business confidence at the end of the year. Indeed, in November, the NFIB SME confidence index jumped to its highest level in three years and the PMI returned to its highest level since 2022 in December. This should undoubtedly be seen as a positive effect of the election of Donald Trump, with businesses awaiting measures that are favorable to them, notably the reduction in corporate taxes. We also observed a similar movement after the first election of Donald Trump in 2016.

The level of PMI surveys is consistent with GDP growth of around 3%, in line with the Atlanta Fed’s real-time GDP estimate. This attributes 70% of this growth to household consumption,

which remains by far the main engine of the American economy. Regarding inflation, the November figures showed that the question was not yet completely resolved. In fact, total inflation rose to

+2.7% over one year and underlying inflation remained stuck at +3.3% over one year for the third consecutive month.

Under these conditions, the Fed toughened its stance during its December meeting. The key rate was lowered to 4.25-4.50%, as expected, but it plans to move more cautiously next year. FOMC members now only anticipate two rate cuts of 25 basis points, compared to four in September. One of the reasons explaining this turnaround is the upward revision of inflation forecasts which would not return to 2% before 2027, compared to 2026 previously anticipated. During the press conference, Jerome Powell indicated that some members had started to incorporate into their forecasts the economic effects of the policies advocated by Donald Trump.

Euro zone: between uncertainties and hopes for improvement

GDP growth in the third quarter was revised upwards slightly to reach +1.7% at an annualized rate, the best result in two years. However, growth drops to +1.2% if we remove Ireland where the data is volatile. Demand contributions show that growth comes mainly from household consumption and stock replenishment by businesses, while the drivers of investment and exports are at a standstill.

The conditions for a continued recovery in consumption seem to be ripe as household income continues to grow at a faster pace than their spending. In addition, the unemployment rate remains very low at 6.3%, despite slight increases in France and Germany. This should enable a further improvement in household confidence and a gradual reduction in the savings rate, which remains high at 16% of disposable income.

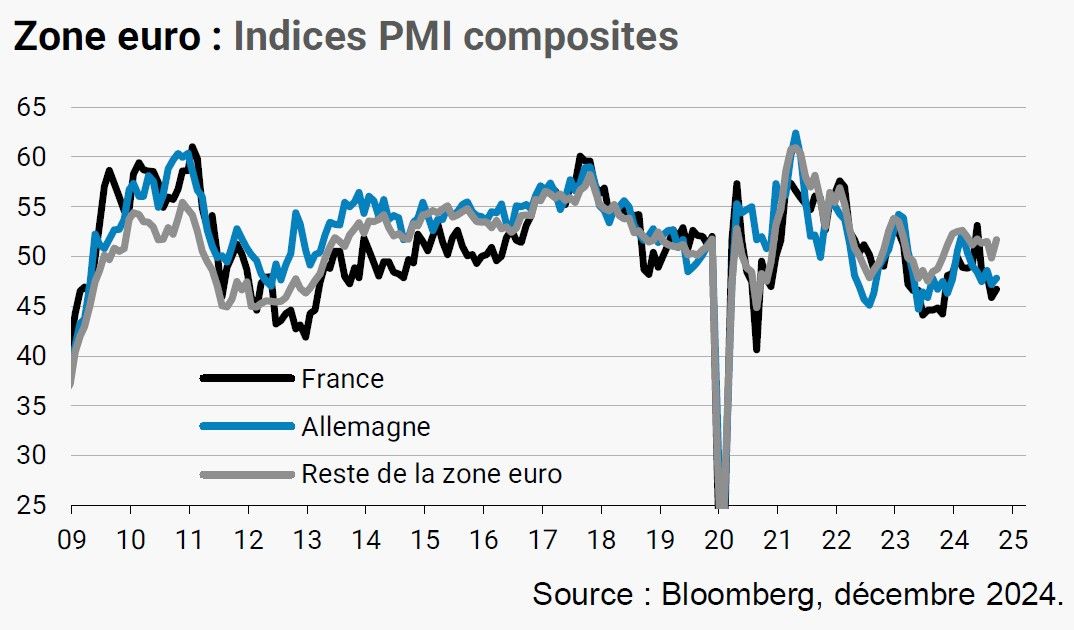

The PMI surveys went up a little in December, which is reassuring after the poor figures in November. However, the composite index remains slightly in contraction territory and the employment-related components are deteriorating. Furthermore, the improvement is mainly explained by the services sector, while the manufacturing sector is still in difficulty. France and Germany continue to underperform against the rest of the Eurozone, two economies where the political situation is uncertain.

France has a new prime minister, but still no government or budget for 2025. In the meantime, a special law has been passed to extend the 2024 budget to next year, which will lead to a clear deterioration in the budgetary situation by compared to what was planned in the Barnier government’s finance bill. Indeed, instead of falling to 5.0% of GDP, the deficit should remain more or less stable around 6.0% of GDP. In Germany, early legislative elections will take place next February after the Chancellor lost the confidence of deputies. Polls indicate the CDU-CSU is in the lead but no party would have a majority, paving the way for a coalition government.

Initially, these uncertainties could encourage households and businesses to adopt a wait-and-see attitude. However, once governments’ roadmap becomes clearer, the opposite effect could occur. This would support activity and would add to the ECB’s rate cuts. Continued progress on inflation allowed a further cut of 25 basis points in December, bringing monetary easing to 100 basis points in this cycle. The market expects a further cut of 120 basis points next year, which would bring the deposit rate down to 1.75% from the current 3.00%.

China: recovery on hold

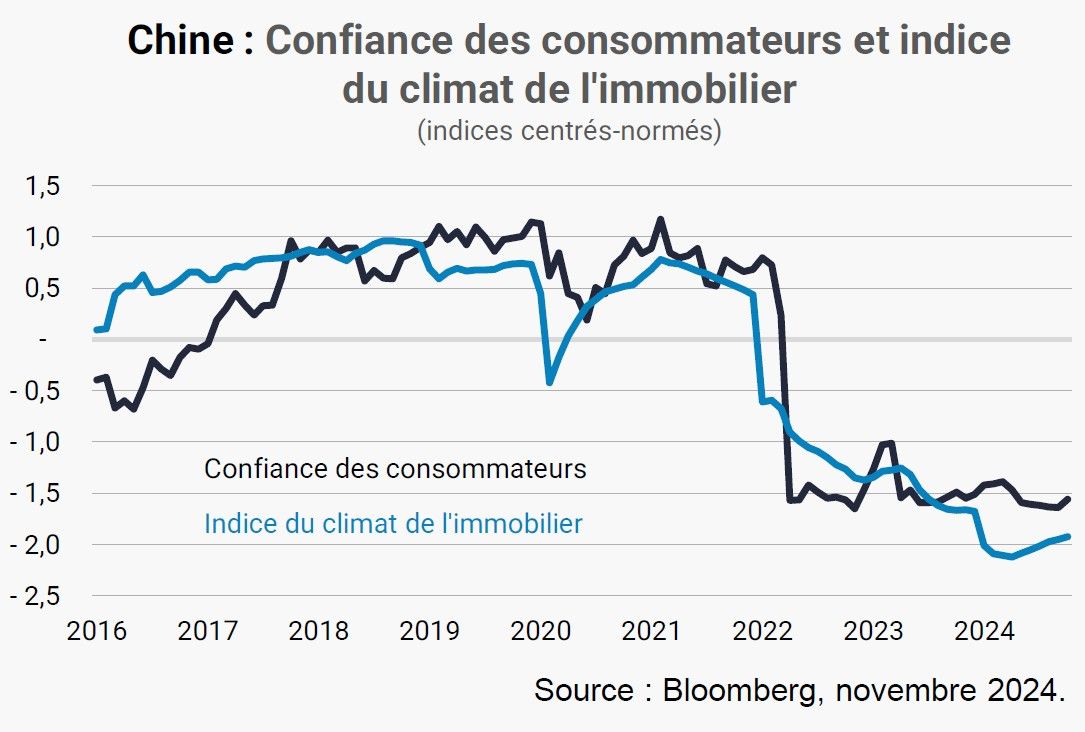

November’s activity data turned out to be disappointing, interrupting the improving momentum observed since the September stimulus measures. The main disappointment concerns household consumption, with a decline in retail sales from +4.8% to +3.0% over one year. However, this backlash was predictable because the anticipated sales schedule had encouraged households to bring forward their spending to October. If we take the average of the last two months, the trend remains improving. But this is not entirely convincing because sales are stimulated by government subsidies for the purchase of durable goods. More fundamentally, consumer confidence remains very low, even if it seems to have passed a low point.

An improvement in the situation on the real estate market could help. Indeed, the two are closely linked, with real estate constituting the bulk of Chinese household assets. The data remains mixed, with a gradual improvement in housing sales, but activity still very weak in the construction sector, like real estate investment which fell by 11.5% over one year. The good news is that this situation allows for a gradual reduction in the stock of homes for sale. However, it is still very high, maintaining downward pressure on prices.

The export manufacturing sector remains an important growth engine for the Chinese economy. Manufacturing production accelerated in November to reach +6.0% year-on-year, driven in particular by a rebound in automobile production, thanks to the government subsidy program, which stimulates car sales. Exports slowed to +6.7% year-on-year, but the trend remains positive and the fear of an increase in customs duties could lead to an anticipated increase in American demand in the coming months. Conversely, imports are trending downward, reflecting the weakness of domestic demand.

Overall, these data highlight the need to strengthen stimulus measures to consolidate the recovery. The annual economic conference generally confirmed the more accommodating orientation of the policy mix next year, but the authorities remained quite vague, making the extent of the recovery uncertain. The authorities have also indicated that they are aiming for relative stability of the currency, the fear being that they could let the RMB slip to offset the impact of an increase in customs duties. Regarding consumption, the government has explicitly committed to expanding the scale and coverage of the subsidy program for the purchase of durable goods.