Whether from an economic, political and financial point of view, 2024 will remain one of the worst years of the last three decades for our “sweet France”. And for good reason: unprecedented political instability, historic surge in public debt, dangerous rise in interest rates on government bonds, massive increase in unemployment, particularly for those under 25, worsening of the real estate crisis, collapse of industrial activity, return of recession in the fourth quarter… Obviously, it would have been difficult to do worse. Fortunately, the Paris Olympics helped limit the damage for a month, but were obviously unable to reverse the trend.

As shown in the graph below, the evolution of the interest rate on 10-year French government bonds perfectly illustrates this discomfiture. Lower than 2.6% in January 2024, it came close to 3.4% following the dissolution of the National Assembly and the absence of a majority within it. With the ECB's drop in interest rates, the lull in the Olympics and then the appointment of Michel Barnier to Matignon on September 5, it then fell back to 2.8%.

French public debt: what you need to know

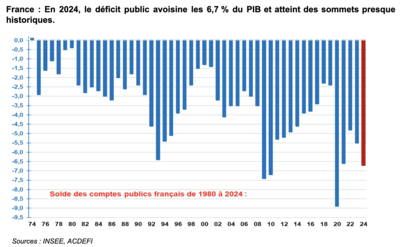

The French public deficit has probably exceeded 6.5% of GDP in 2024 and the debt is exploding

© ACDEFI

But it was only to rise better afterwards, reaching 3.2% with the impossibility of passing a budget for 2025 and then the motion of censure on December 4. Then, despite the barely concealed support of the ECB, it rose to 3.0%, then 3.2% in the wake of the arrival of François Bayrou at Matignon, which did not really reassure investors. Even more serious, as I write this article, it is heading towards 3.3% and widening the gap with its Euro Zone counterparts. The rate spread with Germany thus returns to around 90 basis points (0.9 percentage points). It rises to 40 basis points with Portugal and reaches 10 basis points with… Greece.

>> Buy and sell your shares on the stock market at the right time thanks to Momentum, Capital's premium investment newsletter based on technical, economic and financial analysis, which has done better than the CAC 40 since its launch. If you opt for the annual subscription, 5 months are free.

This aggravated distrust of the French state is also largely justified. Indeed, the latter is the only one in the Euro Zone which has dared to further increase its deficit for almost three years and which still fails to be credible in reducing it by 2025! In 2024, it should also be noted that the French public deficit has probably exceeded 6.5% of GDP, the largest deficit in the EMU and unheard of in French history since the post-war period. with the exception of the year of Covid and those of the 2009-2010 recession.

© ACDEFI

Worse, this deficit exceeds Bercy's initial forecast by almost 100 billion euros. In other words, this is not a small shell but a real state affair, which will obviously not improve France's poor credibility in terms of reducing public deficits. To make matters worse, the new Minister of the Economy, Eric Lombard, has just announced that tax increases were inevitable. And this, while Italy, which has already reduced its public deficit to less than 4% of GDP in 2024, has voted for a tax cut of 30 billion euros for 2025 which will concern both households and businesses .

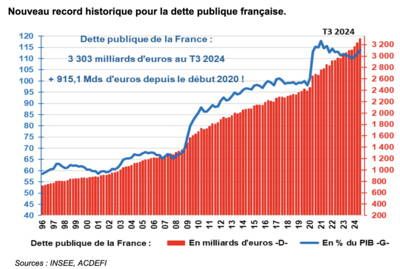

Even stronger, Italy plans to reduce its public deficit to 3.4% of GDP in 2025 thanks in particular to a reduction in public spending. A reminder that “when we want, we can”! Let's hope that this common sense policy will one day succeed in crossing the Alps… And in the meantime and unsurprisingly, the French public debt reached a new historic peak of 3,303 billion euros in the third quarter of 2024. Its share in GDP goes from 112.2% in the second quarter of 2024 to now 113.7%.

© ACDEFI

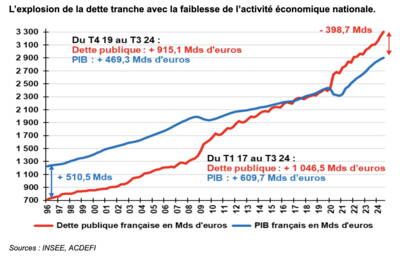

Since the start of 2020, our public debt has exploded by 915.1 billion euros, an increase of 38.2%, that is to say as much as in the previous ten years! And all this for what? For an increase in GDP of 469.3 billion euros including inflation! Yes, you are not dreaming: to obtain an increase in GDP in value of 469.3 billion euros, the French State in the broad sense increased its debt by 915.1 billion euros! So 445.8 billion euros are missing!

Since the fourth quarter of 2017, the large gap between these two variations is also dizzying: + 1,046.5 billion euros for public debt, compared to + 609.7 billion euros for GDP, enough to underline that the he inefficiency of public debt (i.e. its low capacity to generate GDP) is not new but it has deteriorated further over the past three years. A real economic and financial drama!

© ACDEFI

But unfortunately that's not all! Indeed, while consumer prices have still not fallen significantly and inflation is rising again, particularly in food and services, the outlook for activity has continued to deteriorate since the summer. last. The Insee business climate indices and those of purchasing managers are unequivocal: after having been artificially boosted by the Olympics in the third quarter of 2024, French GDP will decline sharply both in the fourth quarter of 2024 and in the first quarter of 2025, marking thereby France's official entry into recession (with two consecutive quarters of decline in GDP).

After sluggish growth, the return of recession for the French economy?

In this context, we must not turn a blind eye: France is falling back into a serious economic crisis. And the social, societal and political upheavals that have affected France since last spring are obviously not going to help the situation. This inevitable drop in French GDP will inevitably result in a further increase in unemployment, but also in public deficits and debt, plunging France into a particularly dangerous pernicious circle…

Growth: the fall of the economy accelerates in France, in industry and services

In this context, as has been observed for several weeks despite the support of the ECB, interest rates on government bonds will further increase significantly in France over the next few weeks and more than in the majority of countries in the Eurozone. Finally, while many economists announced a further appreciation of the euro against the dollar and while we anticipated, somewhat alone against everyone, a clear depreciation of the single currency, the euro continued to plunge against the dollar. On January 2, 2025, it even fell to 1.0265, its lowest since December 2002 (excluding the September 2022 air gap)!

© ACDEFI

And this for at least four reasons. 1. The Euro Zone has fallen back into recession, while American growth is around 3%, as is that of world GDP. 2. The United States/Euro Zone monetary and bond interest rate differentials largely favor the dollar. 3. Donald Trump's victory boosted investor morale in favor of the United States and the greenback. 4. The political crises in France and Germany have aggravated the markets' mistrust of the Euro Zone, which is once again threatened even its very existence. Enough to confirm that if 2024 was a “messed up year”, 2025 could be a “worse year”! A little humor can't hurt us in this increasingly dangerous context! Whatever happens, you can continue to count on me to be by your side during this year which promises to be disconcerting, but which I nevertheless wish you excellent on all levels!

Marc Touati, Economist, Economic Advisor to eToro, President of the ACDEFI firm

You can also find his video reviews on his YouTube channel, which has nearly 207,000 subscribers. Discover the latest: 2024 review: Another messed up year! Who are the winners and losers?