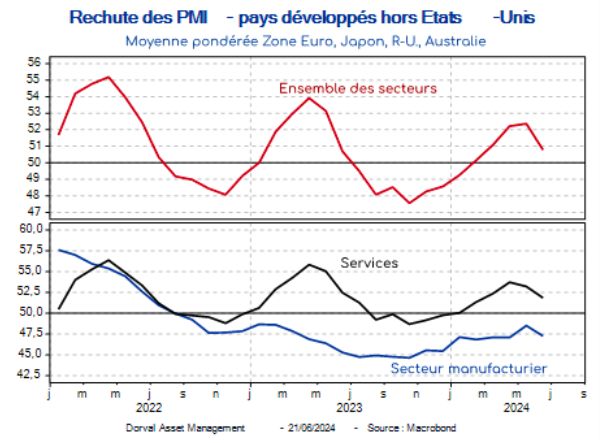

Reboosted during the first months of the year by the dynamism of the American economy, the end of stagnation in Europe and the stabilization of China, the economic optimism of investors threatens to weaken. Household consumption is moderating in the United States, and, outside the United States, the global business climate declined in June for the first time since the beginning of last fall if we are to believe the preliminary PMIs published by the company S&P Global (graph 1).

One month of hindsight is not enough to draw conclusions, and PMI surveys often send false signals about the dynamics of the GDP global. Financial markets, however, are sensitive to the second derivative, particularly when it contradicts a growing consensus – that of a certain optimism with regard to both the level and the diffusion of global growth. If the moderation of the economy American is part of the forecast consensus, two recovery themes are questioned by the latest PMI surveys: that of European growth and that of the global industrial cycle.

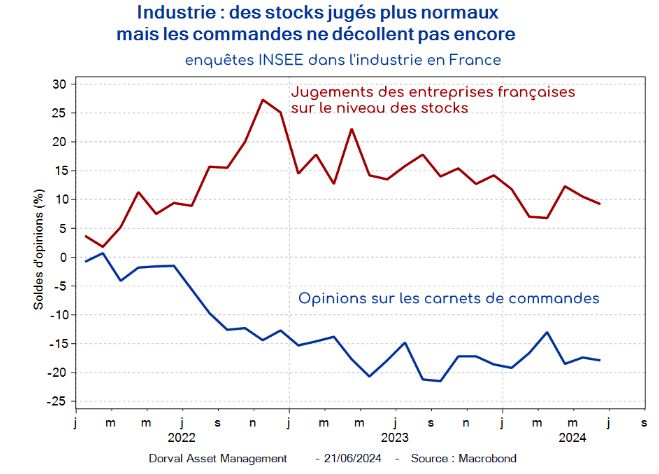

We continue to believe that the gradual reconstitution of the purchasing power of Europeans – prices rising less quickly than wages since last autumn – as well as the scale of household savings and the gradual easing of credit conditions favored by the drop in rate of there ECB should support domestic demand. As for industry, without positive momentum in new orders the recovery remains hypothetical for the moment, but certain necessary conditions are being put in place, such as the better alignment of stocks in relation to demand (graph 2). Some recent statistics also suggest that industrial dynamics are not uniformly weak at the global level. In the United States, manufacturing production rebounded significantly in May (+0.9%), and the PMI survey remains positive (51.7 in June after 51.3 in May).

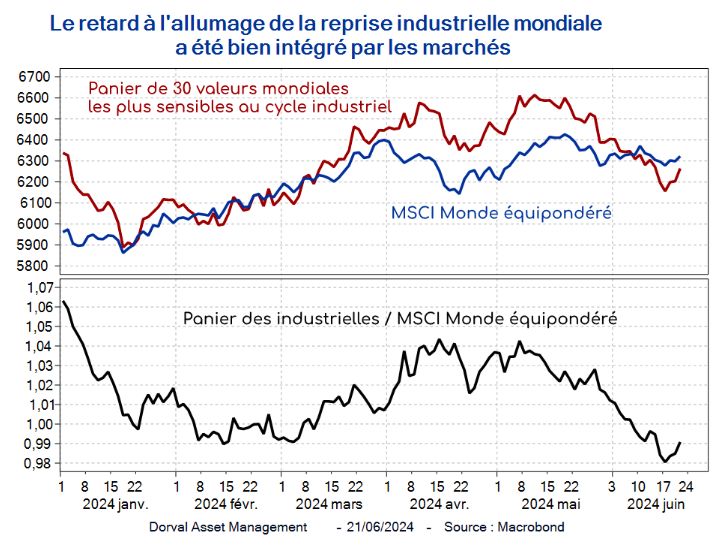

Finally, if by chance the summer of 2024 saw, as in 2023, a phase of weakening of economic optimism and certain growth indicators, this would happen in a monetary context very different from that of last year. Instead of rate increases, central banks are talking about rate cuts. This is already happening in Europe, and in the United States it would take relatively little to tip the Fed over, because the latest inflation figures have been very good. The famous “put” of banks power stations is therefore, in our opinion, well in place, which should encourage investors to look beyond a hypothetical temporary phase of economic disappointments. Note also that the markets have already at least partly integrated these disappointments, the stocks most sensitive to the global industrial cycle having already underperformed significantly since the beginning of May (graph 3).

In our global and European funds we are therefore maintaining for the moment the themes of cyclical industrial stocks and the improvement of the growth-rate mix in Europe (financials, small stocks). In Europe, however, some of these themes are covered due to the French political context. Finally, the core portfolio of our European flexible funds (Dorval Convictions range) remains focused on the major global champions of the Euro Stoxx 50.

Our exposure rates are as follows:

- Dorval Convictions : 60% net exposure to equities including Euro Stoxx 50 ISR core basket 60%, financial basket 6.5%, small cap basket 12%. Hedging in Euro Stoxx 50 futures and Euro Stoxx banks.

- Dorval Convictions PEA : 75% net exposure to equities including Euro Stoxx 50 ISR core basket 70%, financial basket 6.5%, small cap basket 15%. Hedging in Euro Stoxx 50 futures and Euro Stoxx banks.

- Dorval Global Conservative : 24% net exposure to equities, including Sélection Responsible Internationale 19%, Global Industrial Recovery 3%, New Capex 3%, European Financial Basket 1% (partially hedged in Euro Stoxx banks), hedging in S&P 500 options: -1 %. Balance in money market securities.

- Dorval Global Allocation : 50% net exposure to equities, including Sélection Responsible Internationale 37%, Global Industrial Recovery 5%, New Capex 5%, Antifragiles 3%, European Financial Basket 4% (partially hedged in Euro Stoxx banks), hedging in S&P options 500: -2%. Balance in money market securities.

- Dorval Global Vision : International Responsible Selection 73%, Global Industrial Recovery 9%, New Capex 9%, Antifragiles 4%, European Financials 5% (partially hedged in Euro Stoxx banks).

Content written by Dorval Asset Management

{kind=link}