The election of Donald Trump is very scary. But at this point, the world, therefore the stock market, is going up. Yet the risks are there where we don't look as much as it goes up but…

To begin with, I talk about the stock market as being the world because today 70% of the world's stock market capitalization is in the US and 65% of American individuals have seen their wealth reach its highest level thanks to real estate and the stock market.

Thus, we must understand that if an economic crisis occurs, it can especially be catalyzed if the stock market falls. These consumers lose their wealth effect. Must sell to meet expenses and therefore create a snowball effect on the economy. Here it would be the fall in the stock market which would accelerate the decline in the economy.

But at this stage, the stock market is at its highest and therefore the economy is holding up. The opposite phenomenon has been working for 2 years.

But is the election of Donald Trump reshuffling the cards?

Let’s talk about stock market and bond valuation.

Since the election of Donald Trump, rates have risen to 4.5% and the dollar has strengthened. Exactly the opposite of what Trump wants to reduce the pressure on the US debt to continue the deficit and investments with the idea of making goods produced in the US less expensive and restoring the trade balance.

———————————-

Do you want to get started without falling into the traps? progress quickly? Are you tired of losing all your hard-earned winnings in an instant? Do you finally want to win regularly and without stress? So let me teach you everything you need to know to finally take the next step and never be the same investor again. Click here to finally take control of your PEA

———————————-

But the stock market is at its highest in the meantime. Because Trump is pro-business and will lower taxes.

In short, the stock market is currently anticipating the best already. And forget the worst.

The average valuation of the S&P 500 is 17 historically. Today we are at 26 but if we project next year's profits we are at 22 times profits.

As a reminder, when I pay 22 times the profits n+1 on the stock market, this means that I have a return of 4.5%

The 10-year rates are at 4.5% and continue to rise at this stage.

So today, the more my stock market continues to rise, the less the return I receive for taking risk makes sense compared to the return I obtain with the risk-free rate, US debt. My only risk as a European is the dollar/Euro exchange.

But in any case the Euro debt is 3.5% so also interesting for risk-free.

A dilemma then arises for the stock market

As long as the rise in profits in the US continues. at an equivalent level the stock market sees its PE fall and therefore no competition with the bondholder.

But if profits stagnate or decline in the future or if the stock market continues to rise more sharply than the increase in profits, the return on shares falls below 4% and therefore there is no longer a risk premium paid for buy stocks vs. the risk-free bond.

For fans of short-term fomo they don't care, but for those who plan ahead and want above all to safeguard capital, the question will arise.

Obviously, inflation must also be taken into account. If the stock market continues to rise with a lower yield than the bond, it is also because we anticipate 1/ that profits will continue to grow, 2. that inflation will continue. And that actions are protection.

So it doesn't take much in the end for the market to get scared. And it won't necessarily be Trump's fault.

If Trump's tax cuts or corporate profits do not continue to trend favorably. So it's going to get stuck.

If long-term rates continue to rise then things will get stuck.

To continue the rise in the stock market, rates will have to fall, the dollar will have to fall, inflation will rise but not too much and Trump will have to boost our profits through a big cut in taxes and deregulation.

The market has already anticipated all this.

The market did not anticipate, however, that the biggest companies in the S&P 500 are spending lavishly on AI. According to US accounting, these investments are expenses which are then amortized and depreciated to negatively impact the net result.

All it takes is stagnation, a slight increase in the profits of the giants, for valuations to immediately be seen as too high.

With rates at 4-4.5% on American rates, to take risk, normally the investor must be remunerated at 5-6%, i.e. an S&P 500 with a PE around 17, i.e. its historical average. Either we get there by a sharp increase in profits and prices which remain flat. Either by a drop in valuations and stock prices more or less helped by a drop in long-term rates.

Otherwise I don't really see how the stock market is sustainable in the long term.

But the stock market is not just the S&P 500.

The concentration of indices in quality tech values means that the problem is mainly with these values and the indices are therefore heavily weighted.

If we look at the other sectors, energy, utilities, basic consumption, materials, industrials: we are on PEs between 5 and 10. ie a return between 20 and 10% must be well above the rate without risk.

As an investor therefore, if I have to stay invested in shares. My goal will be to diversify on these values, on bonds by discarding part of my expensive tech. In order to rebalance my portfolio and be ready for anything.

The valuation by the PER does not do everything on the stock market

So never forget that when you study a company and its performance for example, you look at past data or even future data but projected by a consensus of analysts who know it tends to have a confirmation bias that is to say to see everything rosy until the results and slash their recommendations after the fact.

So overall, to summarize, the fall in prices today reflects the rise in rates. If rates continue to rise, the risk premium will have to be maintained and therefore lowered further unless companies make more profits. and on the contrary the drop which has not yet taken place or which is starting to come, is that linked to the anticipation of the decline and the deterioration of the results of companies due to the drop in their margins due to the inflation of energy and various PM and therefore of their production costs which they are no longer able to transmit to the end customer.

But if there is a decline, the rates should also reflect this and therefore the risk premium can be improved thanks to the fall in rates also despite a drop in corporate profits.

Everything is and will be for the future a question of knowing how much we are talking about and for how long. For me at this stage it is the idea of normalization, the aftershock first then the more linear rise.

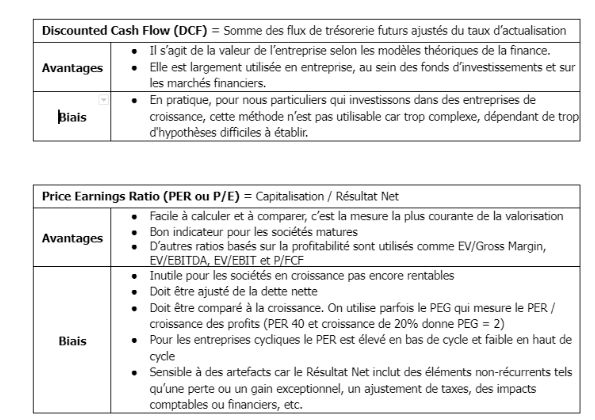

The PER is not everything and, like other ratios, has biases that you need to be aware of

- Low PE = cheap / high PE = expensive

- PE suffers from many biases and should never be used alone

- PE does not work for growth companies (Tech) nor for cyclical, declining or turnaround companies

- PE is only useful for comparing mature, profitable companies with comparable balance sheet structures and generally from the same industry

- % high dividend = very profitable stock

- The sustainability of the dividend over the long term (20 years or more) is essential

- A lower but growing dividend will give a significantly higher total return than a high dividend which is likely to decline over the next 10 years

- There is no “normal” valuation. The market changes and “anomalies” can last for a decade.

- At most, we can compare the company's valuation with that of its peers or measure its evolution over time.

- It is difficult to know whether markets are expensively valued or not

- It's just as risky to buy a company purely for its valuation as it is to ignore it altogether

- There are sometimes aberrantly low valuations, but this is extremely rare. Apple in 2016 was trading with a net cash PE of less than 10. As a general rule, a low valuation should be seen as a signal of risk rather than an opportunity.

- There are regularly aberrantly high valuations on certain trendy companies and even bubbles on entire sectors of asset classes.

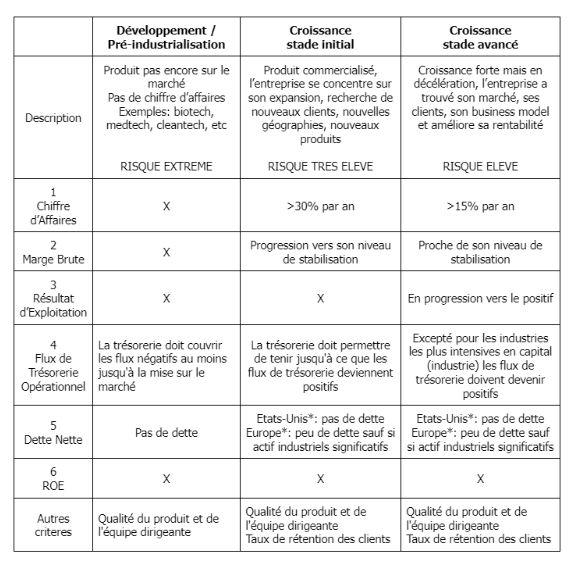

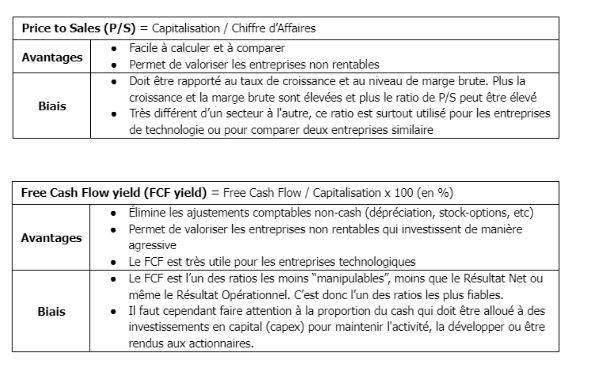

source tableaux: investircroissanceinnovation.substack

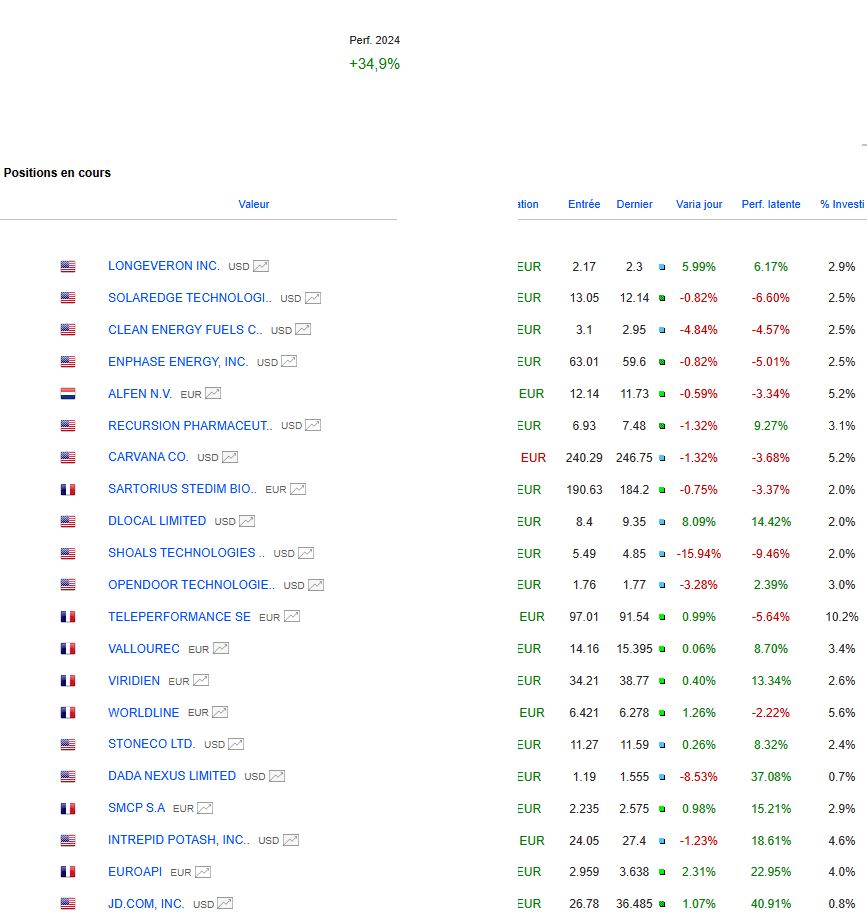

Graphseo Stock Market Portfolio

Few changes, the best is to avoid making big mistakes. Some stocks are still interesting but it's gradually deteriorating so returning to liquidity remains my priority with a desire to stay in take-what-you-have-to-take mode.

A few forgotten stops cost me dearly on solar values which continue to rise where I thought I had a good price for the rebound which took place but was quickly reversed and I did not have the presence of mind to put hitchhiking while I am less present to follow in the evening.

Many titles are on the wire before having to cut. it risks being empty. But I remain in a buying desire but above all to continue to rotate.

friendly

Julien

PS: I also recommend that you read

Note: All investments are discussed, announced and shared in real time on L'Académie des Graphs. The portfolio represents my consolidated personal beliefs (from my various brokers) and is not an invitation to buy or sell. Current performance includes unrealized capital gains or losses and the impact of foreign exchange on foreign stocks. 2023 performance: +38%; 2022: +46%; 2021: +122%; 2020: +121%; 2019: +79%; 2018: +21%; 2017: +24%; 2016: +12%; 2015: +45%; 2014: +30%; 2013: +72%, 2012: +9%, 2011: -11%…

Follow my portfolio and my positions for free by clicking here