More than 4%, or approximately 40 francs: this is the difference that you may be charged for a purchase of 1000 euros abroad at any given time, depending on the bank card you use. The editorial staff of On En Parle and Mon Argent carried out the investigation by sifting through 48 credit and debit cards.

The example used for the test is that of a week-long trip to Europe: the hotel bill, amounting to 1000 euros, is paid in one go on site by card. But how much will it actually cost in Swiss francs, once the exchange rate and processing fees are applied?

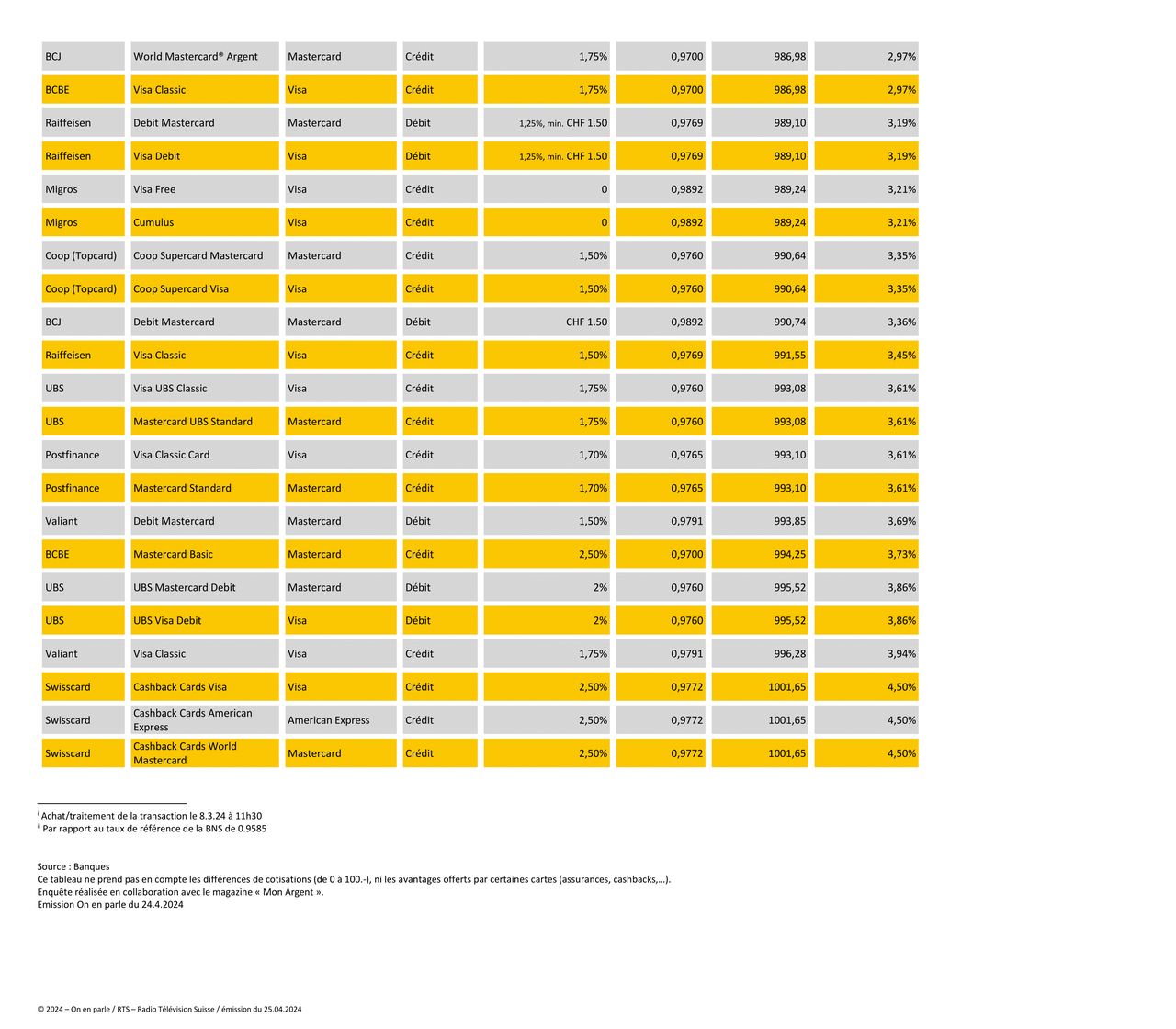

The analysis of the show On en parole and the editorial staff of the magazine Mon argent was based on 48 debit and credit bank cards issued by 23 traditional banks or neo-banks. The latter are 100% digital banks like Revolut, Neon or Yuh, where you manage your account yourself on a mobile phone application. For the comparison, the exchange rate used is that of March 8, 2024 at 11:30 a.m., for an invoice of 1000 euros. The cards are then ranked based on their fees, from cheapest to most expensive.

Result: depending on the card and the bank, the amount can vary greatly. For a bill of 1000 euros, this variation can be up to 40 Swiss francs. The bill therefore goes from 960 francs for the cheapest card to 1001 francs for the more expensive cards.

>> To consult: the complete table of the ranking of the cards: purchases abroad by card.pdf

Neo-banks and debit cards at the top of the rankings

There is no credit card at the top of the ranking. Debit cards are therefore the cheapest, particularly those from the following neobanks: Revolut’s “Standard Revolut” card is first in the ranking, with 960 francs spent for 1000 euros and no commission. Second on the podium, with 962.30 francs, Neon with his prepaid card. Finally, the Yapeal Visa card ranks third with 962.96 francs.

Please note that if the Revolut card is used on the weekend, or if the 1,250 francs mark is exceeded, an additional cost is applied. If the classification had been carried out with a sum of 2000 euros, it would therefore have been different.

“Cashback” credit cards at the bottom of the ranking

The three Swisscard “cashback” credit cards are the most expensive with 1001 francs spent for 1000 euros. This represents an additional cost of 4.5%. There is therefore a difference of 40 francs for the same payment of 1000 euros between the first and last cards in the ranking.

Questioned by We talk about it, Swisscard notes that this comparison does not take into account certain advantages. At the end of the year, the company reimburses up to 1% of the total amount spent by the customer thanks to “cashback”.

Each bank applies its own exchange rate

Invoicing of additional costs is done in two stages. First, each bank applies its own exchange rate, which varies significantly from one establishment to another at any given time. This is one of the findings of this survey.

Then, the foreign payment commissions applied amount to between 0 and 2.5%. These commissions are either fixed or a percentage of the amount. On their account statement, customers see the total amount invoiced, i.e. the exchange rate as well as the commission, if it exists. Note that cards that do not charge commission are not all at the top of the ranking because some make up for it with a higher exchange rate.

Radio subject: Isabelle Fiaux, Tatiana Silva de Sousa, Bastien von Wyss and Yves Genier Web adaptation: Myriam Semaani

{kind=link}