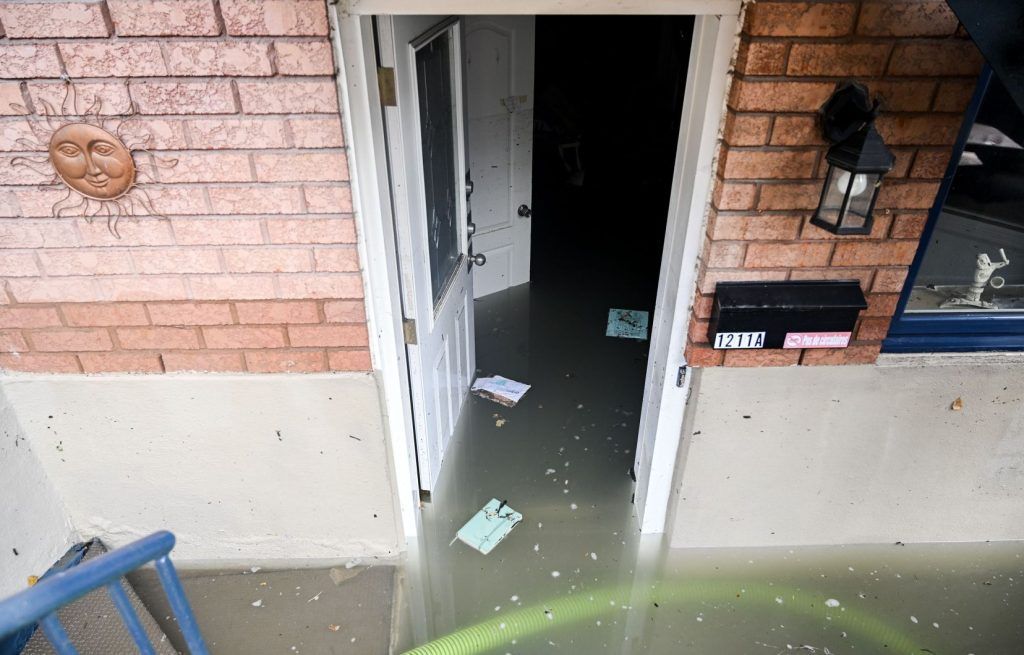

The new mapping of the Montreal Metropolitan Community doubling the number of residences in flood zones does not surprise the Insurance Bureau of Canada (IBC), which represents damage insurers in the country. The latter welcomes the update, which makes it easier to share information with residents.

“All this is nothing new. Cartography only catches up with reality. It does not create flood zones, it only identifies them,” explains Pierre Babinsky, director of communications and public affairs for the BAC in Quebec.

Insurers have already put in place tools to assess flood risk, in particular by using historical data, he continues. “As the minister said [de l’Environnement, Benoit] Charette in June, people who were flooded in 2017 or 2019 should not be surprised to see that the new mapping shows their residence in an area that presents some risk of flooding. »

For people in very high-risk areas, “we are no longer talking about a possibility, but almost a certainty,” says Mr. Babinsky. Access to information is an important aspect of the news, according to him: “There are too many people today who are in areas at risk of flooding and who are unaware of it. »

To be covered by your insurance in the event of flooding, you need a specific endorsement – additional protection – in your contract. “If we don’t have the endorsement, we are not covered” and we will not be compensated by our insurer, Mr. Babinsky simply summarizes. However, the flood endorsement is not available to everyone — it all depends on the level of risk. “Properties that are located in very high-risk areas, generally, are not offered this endorsement by their insurer, or the premium would be very, very expensive. »

Beyond insurance

However, “insurance is not the only solution,” adds Mr. Babinsky. It is part of all the measures that an owner can take to protect themselves well. » He suggests considering “active” protective measures such as installing a backflow preventer, ensuring the waterproofing of the foundation windows, or even installing a waterproof garage door.

Residents should also read their insurance contract carefully: “They may be surprised to already have certain protections.” “When we have doubts about our financial resilience, it is always a good idea to call your insurer or broker” to see what can be done, says Pierre Babinsky.

As for the real estate market, it is too early to determine the effect that the new mapping will have, according to John Fucale, senior vice-president of the brokerage firm Multi-Prêts Hypothèques. “For now, it’s

business as usual

», he said, mentioning in passing the possibility that new rules will be adopted in the coming years to mitigate the risks linked to flooding in certain sectors.

When granting a loan for the purchase of a residence, financial institutions assess the risks of flooding and may request that work be carried out or even refuse to finance an acquisition. In March, the Desjardins Movement announced that it was stopping financing the purchase of houses located in flood zones, with some exceptions.

{kind=link}