Hide summary

The French expect a drop in the rate of Livret A and other livrets. A reduction which will be effective from February 2025. Several estimates of these future rates are circulating. However, it was necessary to wait for the recommendations of the Banque de France.

Or, as our colleagues at MoneyVox tell usthe governor of the Bank of France, François Villeroy de Galhau, has just made his recommendations public. As expected, it is obviously a reduction that he is proposing. But at what level? Is there any good news?

Livret A: a drop in the rate in a few days

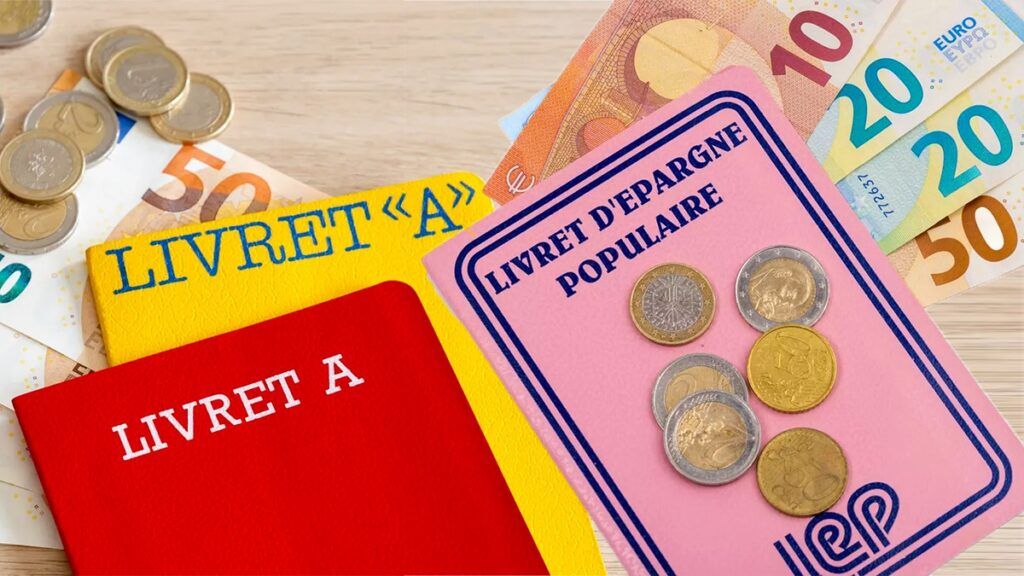

While the media and the French expect a drop of 3% to 2.5% for the Livret A and the LDDS, the governor of the Banque de France opts for a significantly greater reduction. Indeed, according to his proposal, the rate will drop to 2.4% from February 2025.

At the same time, the Popular Savings Booklet (LEP) would see its rate go from 4% to 3.5%. From that side, it's a nice surprise. Indeed, estimates indicated a drop of one point, to 3%.

To have

Finished Booklet A? The 7 alternatives that will earn you more in 2025

This new Livret A rate aligns with the official calculation formula. This takes into account the half-yearly average of inflation excluding tobacco, between July and December 2024, as well as the evolution of the interbank rate €STR (Euro Short-Term Rate) over the same period.

According to the Banque de France, this rate of 2.4% reflects the decline in inflation. The latter is 1.3% at the end of December 2024. In addition, this new adjustment should reinforce the dynamic observed over the past year in favor of the financing of social housing and local authorities, sectors closely linked to Livret A funds.

The Popular Savings Booklet: support for the savings of low-income households

Concerning the LEP, the calculation formula would result in a theoretical rate of 2.9%. A percentage well below the current 4%. However, the Banque de France proposes to set its rate at 3.5%. The goal is to maintain its attractiveness and support eligible households.

-Maintaining the LEP rate at 3.5% will make it possible to preserve a significant gap with the Livret A. In addition, this would further encourage low-income households to benefit from it.

Remember that there are two fundamental differences between Livret A and LEP. While everyone can open a Livret A, only modest French people can have a LEP. Afterwards, the maximum investment for the first is 22,950 euros, while it is 10,000 euros for the second.

To have

The Livret A rate is falling, yet it will earn you more: here’s why

Overall context and outlook for savers

While other savings products often have lower returns, these revised rates remain competitive in a low inflation environment. Indeed, our colleagues from MoneyVox point out that the Livret A like the LEP stand out as secure solutions for the French. The State guarantees the funds and therefore eliminates the risk of losses.

In addition, these adjustments confirm the authorities' desire to preserve the balance between the attractiveness of popular savings and financing strategic sectors for the national economy.

Certainly, rates are falling. However, regulated savings products continue to play a central role in the wealth management of French households. They actually continue to combine safety and reasonable performance.

Source : MoneyVox