Today, everyone seems to agree on the fact that we must invest in large American growth caps. In any case, this is what the market is valuing this year, but also last year and for around fifteen years. Positive sentiment towards the United States (which now accounts for 74% of the MSCI World index), large caps (with Apple, Nvidia and Microsoft as standard bearers) and growth stocks seems to be at its peak. Explanation.

Le match USA vs. ex-USA

The US market has outperformed the non-US market for several entirely rational reasons. First, the earnings power of large U.S. companies, their global reach, and their leading role in technological innovation have been key drivers of this outperformance. American companies, particularly in the technology sector, have been able to capitalize on major growth trends such as artificial intelligence, which has increased their attractiveness to global investors. The “Magnificent 7,” including giants like Apple, Microsoft and Nvidia, captured a disproportionate share of investment flows, contributing to the rise in U.S. indexes. Additionally, the U.S. market enjoys a significant valuation premium relative to other markets, reflecting investor confidence in the resilience and continued growth of the U.S. economy. This premium is justified by faster economic growth compared to regions like Europe and Japan, although the U.S. economy is growing at a slower rate than some developing countries. However, the relative political stability, favorable regulatory environment and high liquidity of the US market attract foreign capital, further strengthening its dominant position. The US dollar also plays a crucial role in this dynamic. Its high value relative to other currencies enhances the attractiveness of dollar-denominated assets, attracting capital flows to the United States. This situation is accentuated by the monetary policy of the Federal Reserve, which, although facing challenges such as inflation, continues to maintain a favorable environment for investments. Furthermore, the United States accounts for a disproportionate share of global stock indices, prompting fund managers to overweight U.S. stocks in their portfolios. This overweighting is often justified by the superior historical performance of US stocks, creating a virtuous circle where sustained demand for US stocks fuels their valuation. However, this outperformance is not without risks. High valuations of U.S. stocks, particularly in the technology sector, are raising concerns that a bubble is forming. Additionally, the concentration of performance in a small number of large caps could leave the market vulnerable to corrections if these companies were to disappoint investors' expectations. The outperformance of the U.S. market relative to the non-U.S. market results from a combination of economic, political, technological and financial factors. However, investors should remain vigilant about the potential risks associated with high valuations and excessive concentration of performance in a limited number of companies. Geographic and sector diversification could prove wise to mitigate these risks and seize opportunities offered by other global markets.

Le triptyque GSV (Global Small Value) vs. ULG (USA Large Growth)

Le match small caps vs. big caps

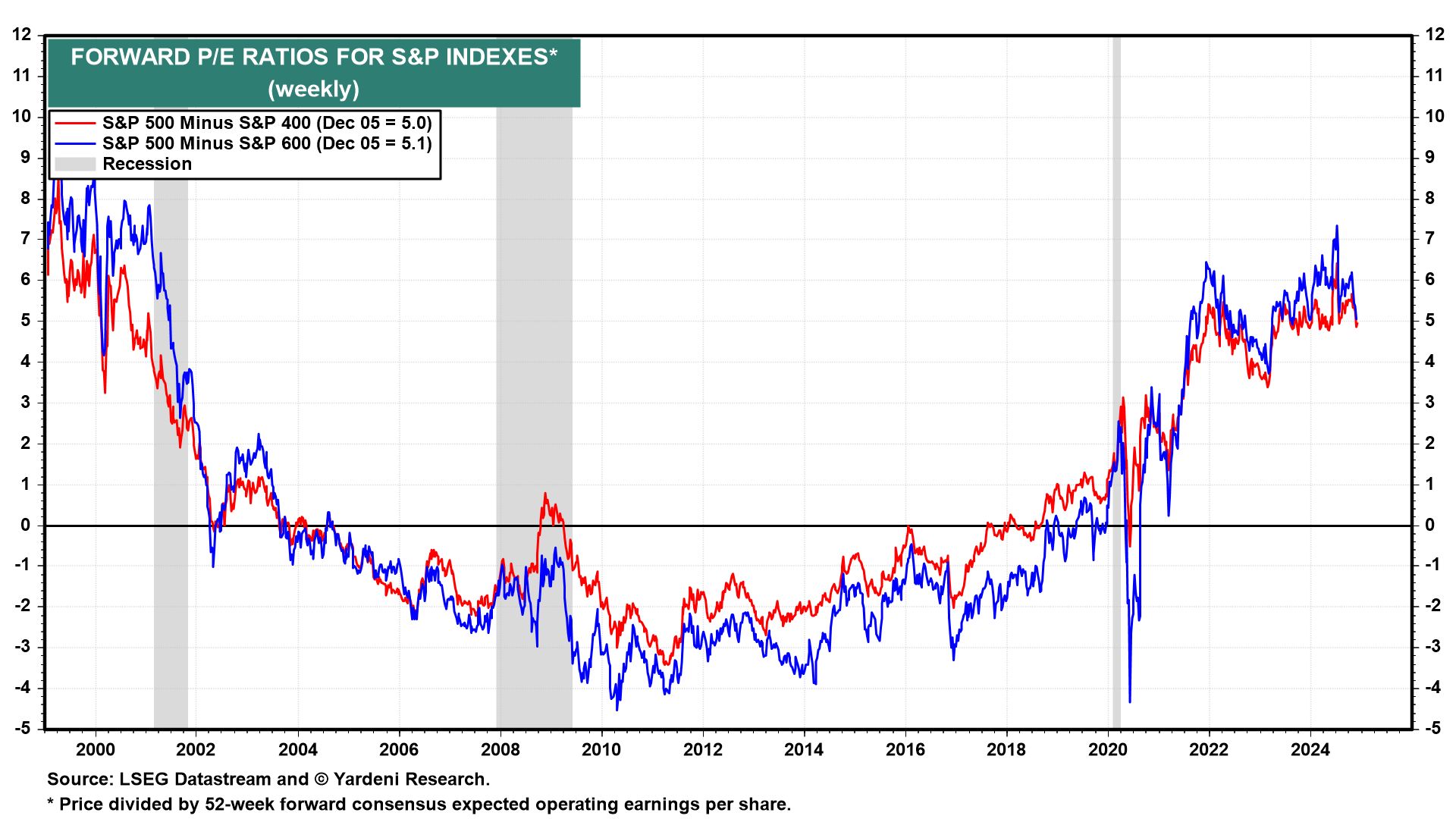

Small caps have underperformed over the past three years compared to big caps, and several factors explain this trend. First, large technology companies, often classified as big caps, have attracted disproportionate investor attention, particularly with the rise of artificial intelligence. The behemoths of the technology sector, nicknamed the “Magnificent 7”, have captured a significant share of investment flows, leaving the small caps in the shadows. This focus on large technology stocks has been exacerbated by the perception of these companies as safe investments, combining growth, profitability and stability. Second, the cost of capital played a crucial role. Small caps, generally more leveraged than their larger counterparts, have suffered from rising interest rates. Indeed, a significant portion of their debt is at variable rates, which makes them particularly vulnerable to rate fluctuations. For comparison, about 45% of small caps' debt is variable rate, compared to just 9% for S&P 500 companies. This has weighed on their performance as higher borrowing costs have reduced their capacity. to invest and grow. In addition, the macroeconomic environment favored large caps. Trade tensions, particularly between the United States and Europe, have created a climate of uncertainty which has encouraged investors to favor assets perceived as safer, often associated with large companies. Protectionist policies, such as those being considered by the Trump administration, have also accentuated this trend, as larger companies generally have a greater capacity to adapt in the face of regulatory changes. Furthermore, ongoing deglobalization has had mixed effects. While it has allowed certain small caps, more oriented towards local markets, to benefit from the relocation of supply chains, it has also limited their access to larger international markets, thus hampering their growth potential. However, this underperformance of small caps could present investment opportunities. Historically, periods of prolonged underperformance of small caps have often been followed by significant rebounds. The reduction in interest rates envisaged by the Federal Reserve could also reduce the debt burden of small caps, thus improving their attractiveness. Additionally, small caps currently trade at a significant discount to big caps, which could attract investors looking for undervalued stocks. Finally, small caps offer welcome diversification in a portfolio often dominated by large technology stocks. Their growth potential, although more risky, remains attractive, particularly in a context where the valuations of large companies are reaching historically high levels. Savvy investors could therefore consider rebalancing their portfolios to include more small caps, banking on a potential return of these stocks thanks to a change in the economic cycle.

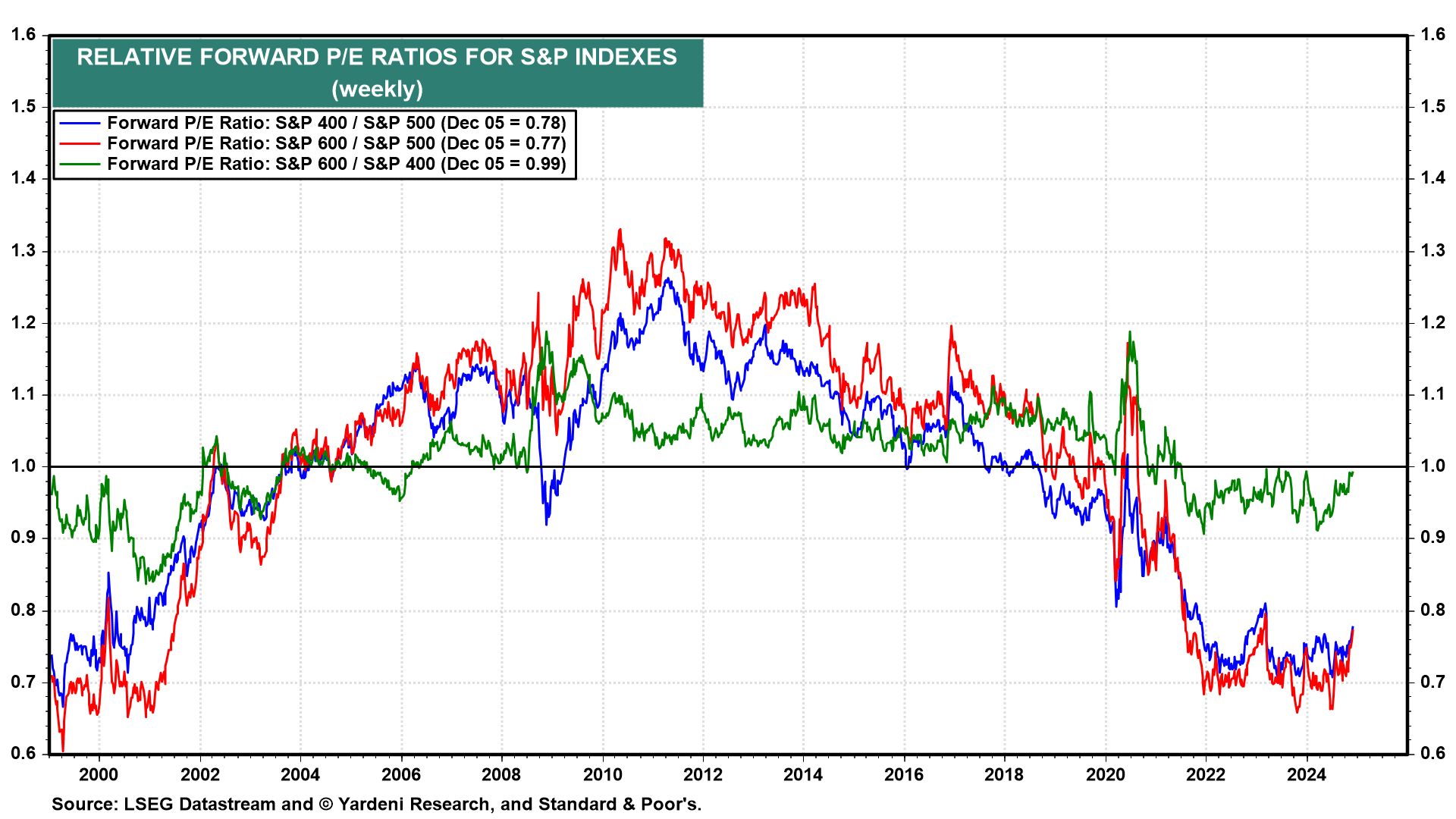

Projected relative valuation in terms of P/E ratio between American big caps (S&P 500), mid caps (S&P 400) and small caps (S&P 600)

Projected relative valuation in terms of P/E ratio between big caps (S&P 500) versus American mid caps (S&P 400) and small caps (S&P 600)

Le match growth vs. value

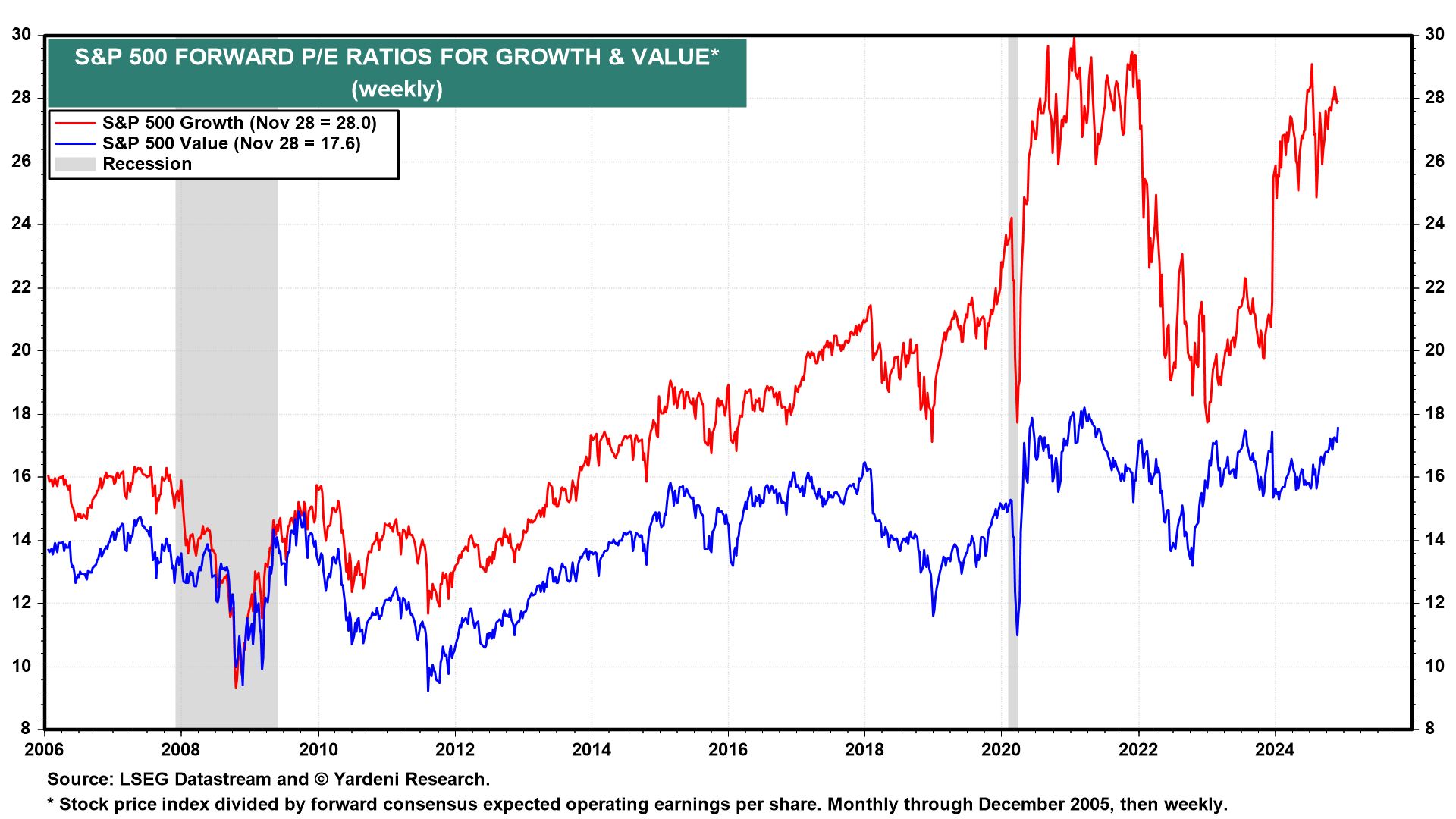

The value style has underperformed the growth style (especially in the US) over the past decade, for several reasons. First, the rise of large technology companies has played a central role. These companies, often categorized as growth, have enjoyed rapid revenue and profit growth, attracting considerable attention and investment. Giants like Apple, Nvidia, Microsoft, Meta Platforms, Amazon, Tesla and Alphabet, nicknamed the “Magnificent 7”, have seen their valuations soar thanks to their ability to combine innovation, profitability and investment security. This dynamic has been accentuated by the rise of artificial intelligence, which has propelled these companies to unprecedented heights. At the same time, the value style, which focuses on companies undervalued by the market, has suffered from the perception that these companies offer less growth potential. Investors preferred to bet on companies offering more promising growth prospects, even at high valuations. This preference for “growth” was reinforced by a low interest rate environment, which favored companies capable of generating significant cash flows and financing their growth at lower costs. Additionally, the COVID-19 pandemic has accelerated digital transition and technology adoption, further strengthening the position of growth companies. Lockdowns and teleworking have stimulated demand for technological services and products, accentuating the divergence between “growth” and “value” styles. Small caps, often associated with the value style, have also been overshadowed by large tech caps. Small caps, although historically more efficient in the long term, have been perceived as more risky in an uncertain economic context. Their higher debt and sensitivity to economic cycles deterred investors, especially in an environment where the cost of capital was crucial. Finally, the concentration of stock market performance on a small number of large companies has exacerbated the underperformance of the value style. Stock market indices, heavily weighted by these technology giants, saw their overall performance pulled upwards, masking the relative weakness of value stocks. In summary, the underperformance of the “value” style compared to “growth” in the United States can be explained by the rise of large technology companies, a low interest rate environment favorable to growth, and a concentration of stock market performances. on a limited number of actors. For the value style to regain its strength, there would need to be a paradigm shift, perhaps initiated by sector rotation or a change in macroeconomic conditions, such as a rise in interest rates or a slowdown in asset growth. tech giants.

The projected valuation in terms of P/E ratio of the S&P 500 Value vs. S&P 500 Growth

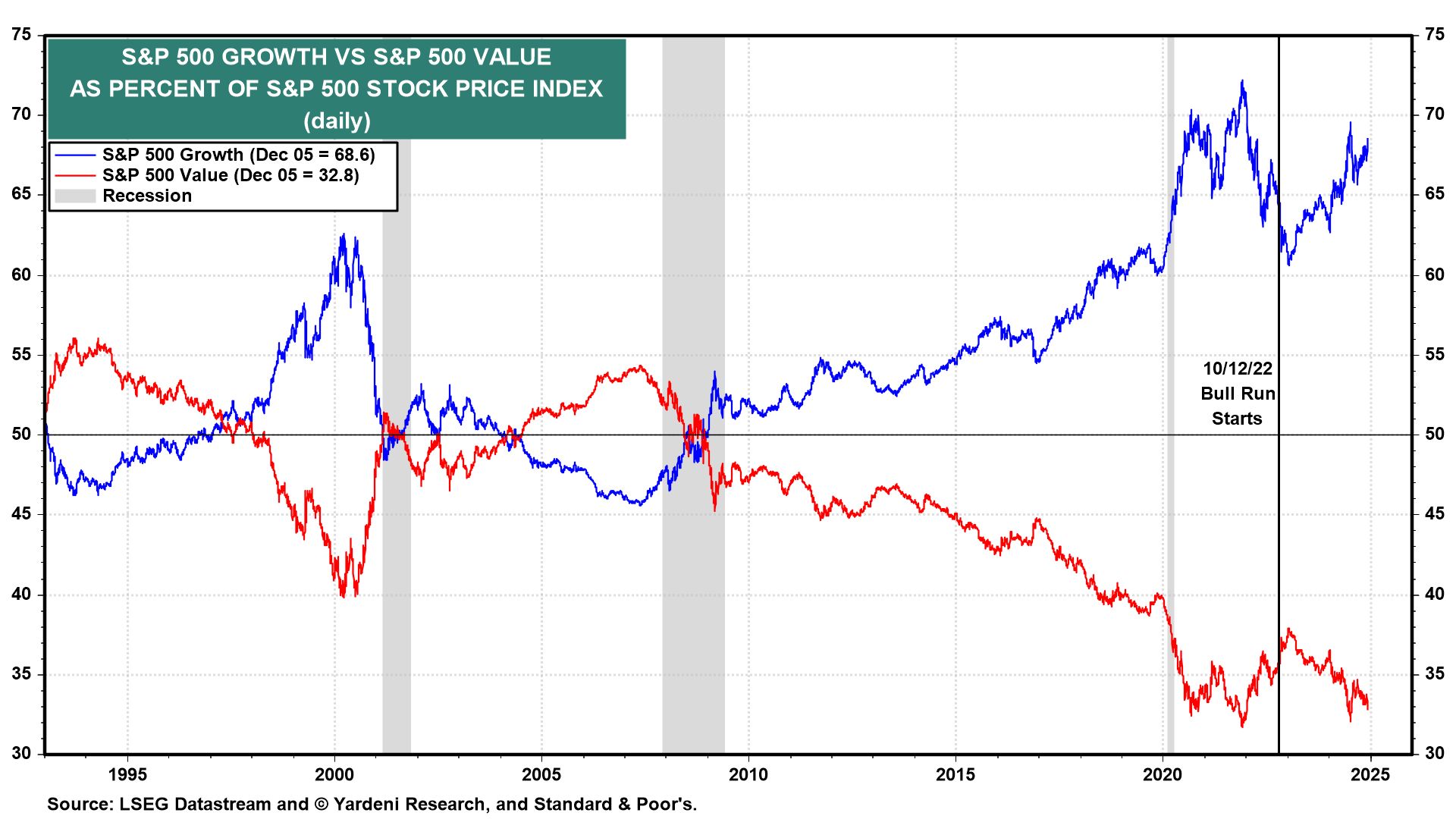

Proportion of value and growth in the S&P 500

Conclusion

Does recency bias mean anything to you? It is this tendency that investors have to place too much importance on their recent experiences and to generalize them. Initially, these stories may be based on actual facts, but they lose their relevance once fundamentals are priced in, pushing valuations well beyond the most optimistic predictions. The problem is that these narratives become so entrenched that when the fundamentals start to change (which is almost always), investors remain clinging to an outdated view. If large American growth caps have won the day in recent years, there is no guarantee that they will do the same over the next decade. Growth needs to be as strong in the future as it was in the previous decade to merit the current valuation. Many valuation experts expect very low returns for the S&P 500 in the future, around 3% per year until 2030.

Investment Ideas for Contrarian Investors