(Ecofin Agency) – Despite a drop in funding, 2024 reveals a changing African ecosystem. Between mega-transactions, sectoral diversification and the emergence of new markets, ten trends are shaping the future of the continent’s start-ups.

In 2024, Africa saw funding for its start-ups decline, reflecting a global economic climate marked by caution and uncertainty. Against the trend of a slight global recovery, with 368 billion dollars raised (+5% compared to 2023, according to Pitchbook), the continent recorded a notable decline, a sign that “financing winters” do not spare emerging markets. However, between the mega-transactions which capture the majority of funds and the small fundraising often relegated to the background, the African ecosystem does not lack vitality. Far from giving in to pessimism, 2024 recounts a year of transformations: sectors like climate tech are gaining ground, emerging markets are asserting themselves, and investor appetite, although attenuated, remains palpable. A mixed portrait, made of promises and resilience for a continent whose margins for progress remain intact. Here are the ten major lessons to remember.

- A notable drop in funding

According to an analysis ofAfrica: The Big Dealone of the reference newsletters on investment in start-ups in Africa, African young shoots raised 2.2 billion dollars in 2024, a drop of 25% compared to 2023 where 2.9 billion dollars had been mobilized. This fall is mainly explained by a particularly slow start to the year. Between January and June, $800 million was collected, the lowest half since 2020. However, a rebound in the second half, with $1.4 billion raised, helped limit the damage.

- Kenya, undisputed leader, consolidates its place after dethroning Nigeria

Kenya dominated the landscape in 2024, with 29% of funding on the continent, or $638 million. East Africa, driven by this “Big Four” giant, attracted $725 million in total, and consolidated its position as the most attractive region for investors for the second consecutive year. Significant fundraising in climate tech, notably by companies like d.light, SunCulture and Basigo, largely contributed to this performance.

- A rebalancing in West Africa

West Africa regained color in 2024, becoming the second most financed region with $587 million, or 27% of the continental total. Nigeria remains the main driver, with more than $400 million raised, but emerging markets like Benin (50 million), Ghana (68 million), and Ivory Coast (33 million) are starting to make an impact. place. This diversity makes the region less dependent on its Nigerian giant and attracts growing interest.

- Egypt and South Africa in difficulty

The two heavyweights, Egypt and South Africa, have had a difficult year. In North Africa, funding fell by 35%, largely due to a 37% decline in Egypt, which nevertheless represents 84% of funds raised in the region. Southern Africa did not fare better, with a drop of 36% and a virtual absence of funding outside South Africa, where 99.4% of funds were concentrated.

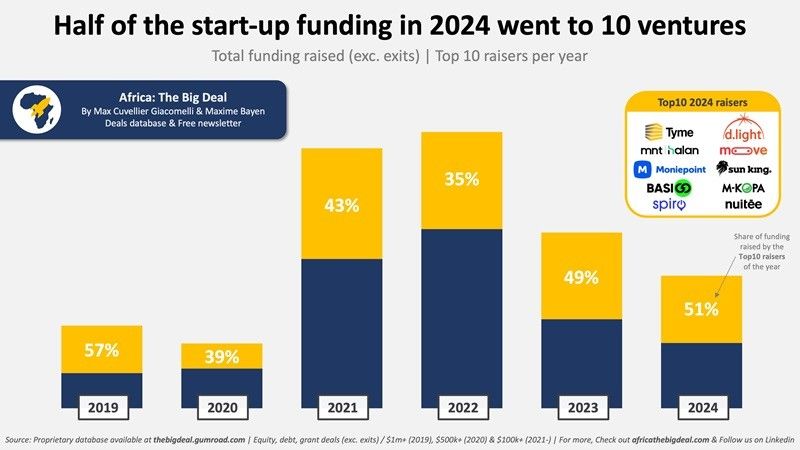

- Very concentrated fundraising

According to Africa: The Big Dealin 2024, the 10 largest fundraisings captured 51% of total funding, a record since 2019 and in line with the trends of the previous year. Among these leaders, we unsurprisingly find Moniepoint and Tyme, joined by two other fintechs, MNT-Halan and M-Kopa. The climate tech sector is also taking a prominent place with players like d.light and Sun King, specializing in solar, and Basigo and Spiro, positioned in the electric vehicle market. Moove and Nuitée complete this list. Tellingly, eight of these companies are headquartered in one of the “Big Four” countries – Kenya, Nigeria, Egypt and South Africa.

The figures also confirm the domination of these flagship markets: among the 42 start-ups having raised $10 million or more in 2024, 86% are also based in one of the “Big Four”.

-On the other hand, start-ups having raised more modest amounts – from $100,000 – display a different dynamic. These 345 companies, representing “the bottom 80% », attracted only 11% of total financing in 2024. While this figure may seem insignificant, these small transactions should not be underestimated. They embody the “long tail” of the ecosystem: the deals of tomorrow are often prepared in the shadow of the modest fundraising of today, concludes Max Cuvellier Giacomelli, co-founder of Africa The Big Deal in his analysis.

- Marked sectoral diversification

While fintech remains a pillar of start-up financing, sectors such as climate tech and digital health have taken an increasingly important place. In East Africa, companies such as SunCulture and d.light have benefited from significant funding, driven by the climate emergency and the growing need for sustainable solutions. In the field of health, West African start-ups like Healthlane are establishing themselves as models of innovation, with technological tools to improve access to care in often under-equipped regions.

- A new breed of investors

In 2024, Africa will see the emergence of a new breed of investors, far from the classic figures of venture capital. Impact funds, driven by a social and environmental mission. Agriculture, energy, sustainable technologies: these investors are redrawing priorities, betting on solutions capable of changing the situation.

But they are not alone. Governments, often criticized for their slowness in adapting to market realities, have surprised by increasing the number of public-private partnerships. From Kigali to Abidjan, the time has come for experimentation. Subsidies, access to infrastructure, tax incentives: States are seeking to attract local start-ups, which have become real laboratories for innovations adapted to the needs of populations.

- A drastic drop in fundraising by debt instrument

Although 2024 was marked by a decline in funding, some positive trends are emerging. The drop in financing is mainly due to a contraction in debt raisings (-40%), while capital raisings (-11%) show a certain stability. In addition, the second half of the year was marked by the emergence of two new unicorns, Moniepoint and Tyme Group, which confirm the continent’s potential for resilience and innovation.

- A shift in investor expectations

L’“financing winter » started in 2022 has left its mark. In a context of global economic slowdown, investor expectations have also evolved. The era of spectacular fundraising without guarantee of profitability seems to be over. In 2024, investors have favored start-ups with solid business models and a clear path to profitability. This new requirement has pushed many young African companies to review their strategy, limiting non-essential spending and focusing on rigorous management. Significant fundraising, such as those of Moniepoint and Tyme Group, show that investors favor well-structured projects with a long-term vision.

- A changing geopolitics of funds

The origins of funding are changing. If the United States and Europe remain major providers of capital, Asia – particularly China and Singapore – is asserting itself as a key player in the African start-up ecosystem. East Africa, in particular, is benefiting from this Asian attention thanks to sectors like climate tech and digital infrastructure.

Fiacre E. Kakpo

Edited by MF Vahid Codjia