It is encouraging that President Trump has tasked Elon Musk and Vivek Ramaswamy with reviewing federal spending under the banner of the Department of Government Efficiency.

The seemingly unstoppable rise in the U.S. debt burden poses serious questions about the health and credit quality of the U.S. economy. And inflationary pressures will only put more upward pressure on Treasury yields. However, the United States has a course of action to deal with the situation, namely the policy implemented after the debt reached 122% of GDP in the aftermath of World War II. A period of higher inflation and financial repression – whereby government policy forces regulated entities such as banks or insurance companies, or even pension plans or the Federal Reserve, to buy more Treasury bonds – made it possible to reduce the debt to 44% of GDP in 1960. This combination thus made it possible to keep the cost of servicing the debt at the time lower than the rate of growth of nominal GDP. If implemented in the coming years, this crackdown could help cap U.S. Treasury bond yields.

Last Friday, the nonpartisan Congressional Budget Office released its 2025 Budget and Economic Outlook Update, just ahead of Donald Trump’s second inauguration tomorrow. Our publication schedule did not allow for an in-depth analysis, but it is possible to draw some broad conclusions from the data already known. What is the outlook for a balanced federal budget and debt sustainability? And what could this mean for financial markets?

Growth fueled by deficits

Budget deficits exploded during the pandemic and continue to widen. Pandemic-related spending was initiated under the Trump presidency, which was already running sizable deficits before the coronavirus outbreak in early 2020. According to U.S. Treasury data, the deficit-to-nominal GDP ratio was – 3.0% – which corresponds to the ceiling under the Maastricht Treaty in Europe – at Mr Trump’s inauguration in January 2017 and increased steadily to reach -4.9% in January 2020. Federal support and stimulus measures intended to combat the effects of lockdowns and restrictions caused the deficit ratio to rise to -18.1% in March 2021, two months after President Biden’s inauguration, before begin to subside. However, the low point of the deficit under the Biden administration was only -3.7% in the summer of 2022, before increasing inexorably to an average of -6.3% in 2023 and 2024, and -6.9% last month.

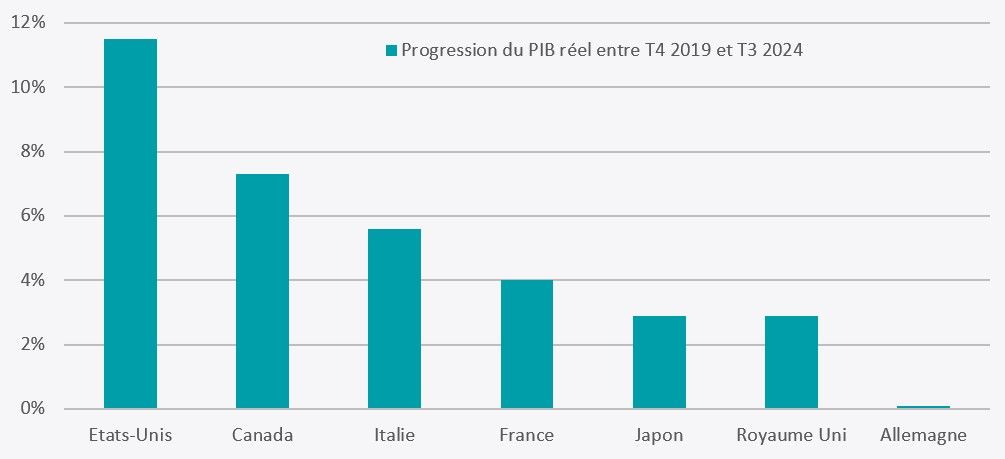

The further deterioration of the budget deficit during the latter part of the Biden administration was due to the government’s overhaul of industrial policy to boost domestic industry and the green transition, through a series of known initiatives collectively as Bidenomics (Biden economic policies). In terms of economic performance, it appears that these policies have worked: the United States has far outperformed other advanced economies since the pandemic. According to a recent study by the US Treasury, cumulative real GDP growth in the United States reached 11.5% between the fourth quarter of 2019 and the third quarter of 2024, compared to 4.0% in France and only 0.1% in Germany. (see graph).

Source: US Treasury Department

However, this growth was largely fueled by debt, meaning that short-term growth was boosted beyond the potential long-term GDP growth rate, which is largely determined by demographics and productivity. According to the Congressional Budget Office (CBO), the potential annual growth rate was 2.1% in the fourth quarter of 2024 and is expected to fall to 1.7% by 2034. Bidenomics policy anticipated consumption on future demand , which could slow down economic growth in the future.

Darkening debt outlook

It is striking that during the presidential campaign none of the three main candidates paid attention to the budget deficit and the increasing debt burden. On the contrary, according to the Committee for a Responsible Budget Deficit (CRFB), the cumulative budgetary impact of implementing the policies of the Trump agenda could reach a maximum of -$15.6 trillion between 2026 and 2035, with a projection central bank of -$7.8 trillion (for Kamala Harris, the equivalent figures were -$8.3 trillion and -$4.0 trillion, perhaps lower but still equivalent to between 28.3% and 13.4% of current nominal GDP).

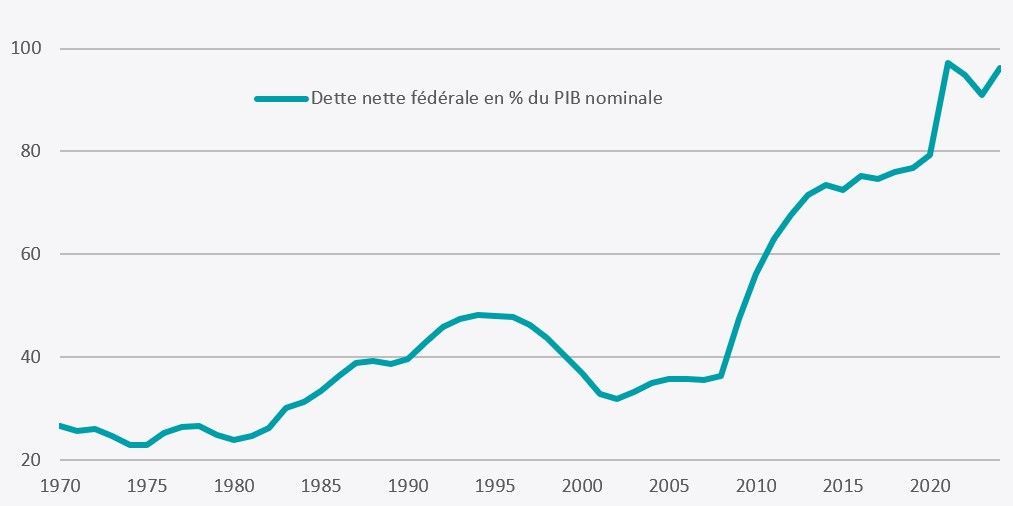

And these projections come on top of a debt already increasing sharply according to the CBO which estimates that it could reach 125% of GDP by 2035, and this does not take into account the debt held by the Medicare and security programs. social. Adding the impact of the central projection of President Trump’s program, the CRFB estimated that the net debt burden could reach 143% of GDP in 2035. In comparison, the debt burden amounted to 96.4 % in the third quarter of 2024, as shown in the chart below.

Source: FRED, Federal Reserve Bank of St. Louis

There is no absolute rule for determining beyond which level of debt GDP growth begins to be burdened. However, two former IMF economists, Carmen Reinhart and Kenneth Rogoff, attempted an estimate in their seminal 2009 book, This Time is Different. They argue that economic growth potential could be impaired when debt/GDP ratios are above 90%. This assertion is hotly contested by economists – why 90% and not 60% like the Maastricht threshold, or 120%? – but the basic principle that money used to service the debt is not available for more productive uses seems to hold water. Such a level of debt may not be so important when ten-year Treasury yields average 2.4% as in the 2010s – and even less so when they fall below 1% mark as it did for most of 2020 – but it’s becoming a pressing issue now that yields are back at 4.6%.

DOGE to the rescue?

Given this dynamic, it is encouraging that President Trump has tasked Tesla boss Elon Musk and former Republican presidential candidate Vivek Ramaswamy with reviewing federal spending under the banner of the Department of Government Efficiency ( DOGE). At the recent CES tech show in Las Vegas, Elon Musk said that a best-case scenario would be -$2 trillion in savings and that aiming for such a level would give them “a good chance” of getting – 1 trillion dollars.

However, even -1 trillion dollars is extremely ambitious. In its studies, the CBO distinguishes between mandatory spending, which amounts to $4.1 trillion in 2024, and discretionary spending, which reaches $1.8 trillion. Considering that $850 billion of the discretionary budget represents the defense budget, it seems virtually impossible to eliminate the entire remainder, which includes areas such as education, veterans’ health care , transport and border security.

Optimists point out that Argentine President Javier Milei has managed to cut spending by around 30% and balance the budget since coming to power in late 2023. However, Milei’s explicit campaign promise was to cut spending drastically , as illustrated by the chainsaw he brandished during his rallies. For his part, Donald Trump has made no such promises, and his electorate is therefore ill-prepared for the level of disruption that Musk’s proposed cuts would cause. Furthermore, although the White House makes proposals, spending is under the control of Congress, which has shown little appetite for belt-tightening in recent years.

Additionally, the new administration has promised to renew the Trump Tax Cuts and Jobs Act of 2017 (TCJA), which was set to expire this year, thereby increasing individual taxes. According to Penn Wharton’s budget model, a permanent extension of the TCJA would increase cumulative deficits over the next decade by -$4 trillion, or 13.6% of current GDP.

Financing costs and bond vigilantes

The situation is further complicated by the increasing cost of financing the US debt. According to the CBO, net interest on the national debt reached -$949 billion last year, surpassing the cost of the military for the first time in recent memory. And this cost is expected to increase further.

First, a number of President Trump’s campaign promises are somewhat inflationary in nature. For example, high tariffs on imports would be partly absorbed by importers, but most would be passed on to consumers in the form of higher prices. Furthermore, the mass expulsion of illegal immigrants would significantly reduce the number of low-wage workers, putting upward pressure on average wages and, therefore, sales prices. Furthermore, large and growing budget deficits are inherently inflationary. Such pressure could force the Federal Reserve to reverse its policy of lowering rates.

Next, we can expect further upward pressure on Treasury bond yields, which have already increased by almost 50 basis points since the beginning of November. The CBO’s projections are based on inflation of 2.3% this year and 2.2% annually thereafter, and the risk is that these estimates prove too optimistic. In this case, rising bond yields would result in higher debt service costs as the Treasury issues new bonds with higher interest rates.

There has been a lot of talk recently about the return of bond vigilantes (“bond vigilantes”), traders or investors who threaten to sell Treasury bonds and stop buying new issues if the government does not improve its balance. budgetary (this expression was coined by strategist Ed Yardeni in the 1980s). With the CBO projecting that debt service costs will reach $1.7 trillion by 2034, the equivalent of 42.5% of all projected individual tax revenues, it is not surprising that Many economists fear a surge in bond yields.