In the euro zone, industrial production in April came in below expectations. In China, the progression of the consumer price index was stable in May.

Economy

The statistics published in the United States are somewhat mixed. The May inflation publication reassured: general price growth is lower than expected (+0% m/m vs. +0.1% est. and +3.3% y/y vs. +3.4% East.). The same goes for underlying inflation, excluding energy and food, (+0.2% m/m vs. +0.3% m/m est. and +3.4% vs. +3.5% est.). SME confidence (NFIB) recovered slightly (from 89.7 to 90.5) in May. The increase in unemployment claims is, however, a disappointment (242,000 vs. 225,000 expected) as is the fall in household confidence (Univ. of Michigan) in June (from 69.1 to 65.6). In the euro zone, industrial production disappointed in April (-0.1% m/m vs. +0.2% est.; -3% y/y). Finally, in China, the progression of the consumer price index was stable in May (+0.3% y/y) while a slight acceleration was expected (+0.4% y/y).

Planetary boundaries

According to a United Nations report released today analyzing the performance of 193 member states against the 17 Sustainable Development Goals defined in 2015, it appears that none of these 17 goals is on the trajectory to achieve the goals of 2030. The institution recommends that States redouble their financing efforts to achieve these objectives and also to overhaul the UN system itself.

Obligations

In the US, the Fed kept its rate unchanged, while the 2024 DOTS forecasts only foresee one reduction (vs. 3), which was more “hawkish” than expected. Nevertheless, inflation surprised favorably (0% m/m vs. 0.1% expected), with the first signs of disinflation on the services side. In this context, US rates fell sharply (10Y -22bp). In Europe, French political tensions led to a rally in German rates (10Y -26bp), while the French sovereign underperformed (10Y +3bp): its spread at 10Y vs Bund is close to 80bp, the highest since 2012.

Trader sentiment

Sotck exchange

A Europe sick of its policy, the USA at its highest with little catalysis for the continuation of the rise. This week, investors will face few if any major macroeconomic figures and a Wednesday off in the United States. Finally, although a rebound is likely in Europe, reluctance and a wait-and-see attitude should be required this week.

Currencies

Risk aversion causes the € to fall against the main currencies: €/$ 1.0696, €/CHF 0.9531. A temporary rebound remains possible but we remain negative on the € until the French elections, our ranges: €/$ 1.0535 -1.08. The CHF is trending upwards $/CHF 0.8907, €/CHF 0.9530; a rate cut by the SNB this week (-0.25%) could slow this trend. Our ranges: $/CHF 0.8825-0.9015, €/CHF 0.9440-0.9610. The £ is down £/$ 1.2670, sup. 1.2630 res. 1.2800. Gold consolidates at $2317/oz, higher. 2282 res. 2354.

Markets

The announcement of early legislative elections in France weighed on European assets, while the Fed’s decision, a little more hawkish than expected, was more than offset by favorable inflation figures. Thus, 10-year sovereign rates fell by >20bp in the US and Germany and were unchanged in France. Equities are progressing (US: +1.6%; emerging countries: +0.4%) outside Europe (-2.4%). The strengthening of the dollar (+0.6%) does not prevent that of gold (+0.7%). To be monitored this week: Empire Manufacturing, retail sales, industrial production, real estate developer confidence, housing starts, building permits and manufacturing and services PMI in the United States; ZEW confidence index, manufacturing and services PMI and household confidence in the euro zone; consumer and producer price indices in China.

Swiss market

To be monitored this week: evolution of nominal wages (OFS), summer economic forecasts (KOF & Seco), May accommodation statistics (OFS), 2023 financial stability report (BNS), foreign trade/watch exports May ( OFDF), April construction price index (OFS) and assessment of monetary policy (BNS). Klingelnberg has published its 2023/24 results.

Actions

Last week, during WWDC 2024, APPLE (Core Holdings) has highlighted convenience and improvements in AI capabilities on its devices. Forecasts for the coming quarters indicate a deceleration in annual growth in iPhone sales. The group will have to wait until September 2025 to potentially initiate a new cycle of device sales.

ING (Satellites): management today unveils its strategy and objectives for 2027. With essentially annualized growth of 4-5% and an ROE of 14%, the consensus is 5-10% behind the group’s ambitions at this time. stadium.

ROCK (Core Holdings) on Sunday presented positive phase III data for Columvi in second-line use in diffuse large cell lymphoma (a form of blood cancer). The indication represents a sales opportunity of c. 2 billion francs.

SIKA (Core Holdings) opened its 34th factory in China, in the province of Liaoning, for the production of mortars, adhesives and sealants. It will serve an area of c. 100 million people in northeast China and Mongolia.

Finally, it should be noted that we have removed several titles from our recommendation lists namely ESTEE LAUDER & STRAUMANN (Core Holdings list) as well asALSTOM, EDENRED And ORANGE in the Satellites list.

Chart of the day

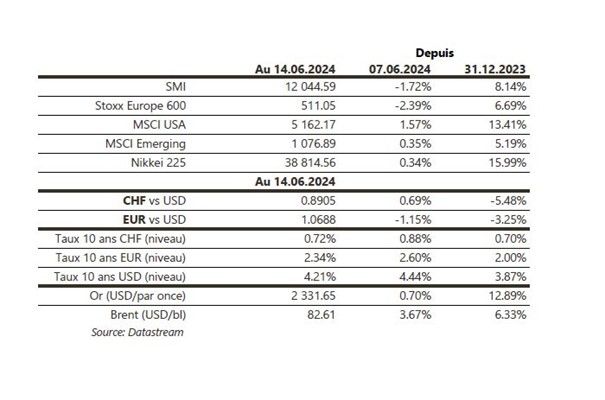

Performance

{kind=link}