Whether from an economic, political, social and societal point of view, France is unfortunately collapsing before our eyes and almost no one is reacting… All recent events unfortunately point in this direction: the censorship of the Barnier government , the repeated boondoggles on the 2025 budget, the heights of unpopularity of Mr. Macron, the surge in public deficits and debt, which have also become uncontrollable, but also the collapse of leading indicators of activity and the soaring prospects of increasing unemployment… A real economic and political horror! And it is not the appointment of a new Prime Minister that will change the situation.

Moreover, to make matters worse and confirming these slippages, the interest rates on French government bonds remain high despite the support of the ECB. They even passed above that of the Greek State during the week of December 2 and have remained at the same level since. At the same time, the 10-year interest rate difference (also called “spread”) between France and Germany reached 90 basis points, a peak since the summer of 2012, and has now stabilized around of 80 basis points, which remains very high. As for the France-Portugal “spread”, it has risen to between 30 and 40 basis points since last October.

For the first time, the 10-year interest rate on French government bonds has exceeded that of Greek government bonds and remains close to it

© AFT, BCE, ACDEFI

This shows the extent of the crisis of confidence that France is currently experiencing vis-à-vis the financial markets and investors in the broad sense. This sanction is nevertheless deserved. Indeed, France is the only country in the Euro Zone which has increased its public deficit over the last two years. Even more serious, it is the only one which is the subject of a procedure by the European Commission for excessive deficit and which is preparing to not respect its commitments for 2025.

Budget 2025: “The credibility of the French state is truly in free fall!”

And for good reason: the 2025 budget will be duplicated on that of 2024which forecast economic growth of 1.5%. However, in view of the advanced indicators of French economic activity (whether the Insee business climate and household confidence indices, but also the purchasing managers’ indices), not only should French GDP decline in the fourth quarter of 2024, but, moreover, it should only increase by at best 0.5% next year.

France: the composite PMI index collapses and announces a plunge in GDP at the end of 2024-beginning of 2025

© Insee, ACDEFI

In this context, the public deficit will still be greater than 6% of GDP in 2025. Which, for the second year in a row, will place France as the country in the Euro Zone with the highest public deficit. A new wave of distrust could then begin, sparking a new movement to increase bond interest rates and widen the “spreads” with the other members of the EMU. And this, especially since even before the 2025 budget, the real state of France’s public finances is simply catastrophic, with in particular a public debt which is around 3,300 billion euros and 115% of GDP.

>> Buy and sell your shares on the stock market at the right time thanks to Momentum, Capital’s premium investment letter based on technical, economic and financial analysis, which has done better than the CAC 40 since its launch. If you opt for the annual subscription, 5 months are free.

Certainly, in March 2020, given the cataclysmic global situation that then prevailed, it was conceivable to do everything to avoid the worst, in particular by increasing the public debt, which was also largely financed by the European Central Bank ( this is what we call “printing money”). The serious mistake was to continue to cause the public debt to soar after 2020. I have not stopped alerting the public authorities since then, but unfortunately without success.

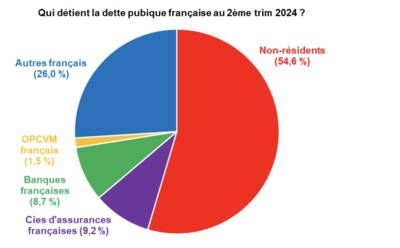

Moreover, this mismanagement of public debt has produced only poor economic results.. The figures speak for themselves: since the start of 2020, public debt has increased by around 850 billion euros, while, over the same period, French GDP in value (i.e. increased of inflation), increased by 450 billion euros. Yes ! You are not dreaming: 400 billion euros are missing! A French inefficiency which does not date from yesterday. The last French public surplus actually dates back to… 1974! The worst is that despite 50 consecutive years of deficits (a record for developed countries), French structural growth has continued to fall, going from 2.5% per year in 1980 to 0.9% today. today. It is this dangerous headlong rush that has caused the surge in public debt. The latter represented only 20% of GDP in 1980, compared to nearly 115% today. Even more serious, 54.6% of our public debt is held by non-residentswhich therefore makes us more and more dependent on the latter and de facto harms our sovereignty.

54.6% of French public debt is held by non-residents (compared to 47.8% at the end of 2021)

© AFT, Banque de France, ACDEFI

The tragedy of public debt is not so much its level as its lack of sustainability. A debt is indeed sustainable if it generates at least enough income to repay the interest on the debt each year. However, in France, such a situation has not been observed since 2007. Furthermore, given the recent increase in interest rates on French government bonds, the interest burden on French public debt currently reaches 60 billion euros per year, and soon 75 billion euros.

This has become unbearable, especially as the increase in interest rates affects all business and household credit. Hence a collapse in economic activity, which gives rise to a rising unemploymentbut also an increase in public deficits and debt, which leads to a new wave of increase in interest rates… and the pernicious circle continues until exhausted… Whatever happens, the crisis of confidence The capacity of the French State to reduce its public deficit will therefore increase, worsening the recession which is taking hold in France. How sad!

To end on a note of hope, it must be emphasized that France’s budgetary recovery remains possible. In fact, to reduce our deficit and save the French economy, we must engage in what I call “benevolent shock therapy.” This passes through two essential routes. On the one hand, a lower taxes for allbusinesses and households (notably taxes on production and the CSG), in order to revive confidence and economic growth. On the other hand, a clear reduction in public expenditure and in particular operating expenditure which has increased by more than 15% over the last three years, or 3 points more than all public expenditure. This is complete nonsense: when a company is in deficit, it starts by reducing its operating expenses to save the rest. In France, the State does exactly the opposite. It is high time that this changed.

Special law: will your income tax increase in 2025 without indexation of the scale?

Marc Touati, economist, president of the ACDEFI firm, economic advisor to eToro

You can find his video chronicles on his YouTube channel, which has more than 196,000 subscribers, including the latest: France, World, Stock Market, Bitcoin… What should we fear or hope for 2025 ?