Editorial. There are debates that, in hindsight, should not have been held. And the one that pitted Biden against Trump last week on the other side of the Atlantic is one of them. The long-awaited event has, in fact, turned into a disaster for the Democratic candidate. A shipwreck that, once again, raises questions about the outgoing President’s ability to serve a second term. And, in the meantime, to grapple politically with his opponent over the rest of the campaign. Bluntly, some are now even inviting him to hand over without waiting for the November vote count. In short, this debate too many seems to have increased the chances of seeing Trump redecorate the Oval Office next January. The potential future tenant of the White House is of course not in his first lease and makes no great secret of his conduct of affairs. We already know the economic color. The opportunity to anticipate, a few months in advance, what the consequences could be for the markets.

Internationally, Trump II has already announced that he wants to continue the trade war he has started with the Middle Kingdom by raising customs duties to more than 60% on imports “made in China”. A prospect that could, if pushed too far, weigh on stocks as well as bond yields. Beyond that, the increase in tariffs on imported products could also impact sectors such as distribution, textiles and even furniture. In terms of the environment, he would once again throw the Paris Agreements in the trash – from where Biden had taken them in 2020. Trump II would also authorize the oil majors to resume their Swiss cheese-style drilling and would eliminate subsidies for wind turbines. A horizon – bleak for the climate – which would logically be favorable to the energy sector on the stock market and, on the contrarypenalizing the renewable sector – and, in addition, a sector like electric vehicles. Finally, he has every reason to believe that he would continue the relaxation of American financial regulations started under his first term, which will not fail to benefit the banking sector… Response to these hypotheses, on the evening of November 5.

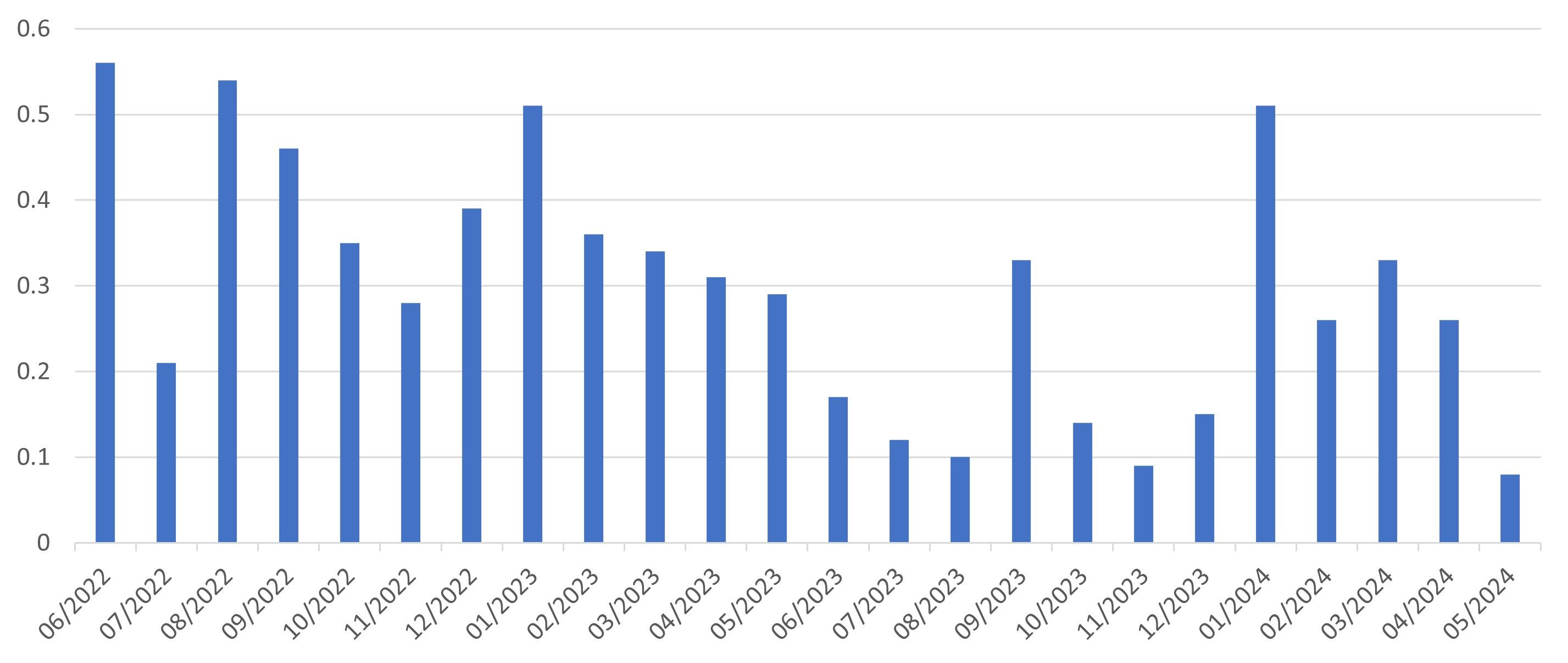

Chart of the week:

US inflation slows

Source : Bloomberg, June 2022-June 2024 – US Core Personal Expenditures Price Index (month-over-month and %)

To read the article in its entirety, Click here.

Disclaimers:

This document may not be reproduced or distributed without prior permission.

Fidelity only provides information about its products and does not make investment recommendations based on specific circumstances, this document does not constitute an offer to subscribe or personalized advice. Fidelity International refers to the group of companies that form the global investment management structure that provides information on products and services in the designated jurisdictions excluding North America. This information is not intended for and cannot be used by residents of the United Kingdom or the United States. This document is intended for investors resident in France only. Unless otherwise stated, all information communicated is those of Fidelity International, and all views expressed are those of Fidelity International. Fidelity, Fidelity International, the Fidelity International logo and the symbol F are registered trademarks of FIL Limited. This document was prepared by FIL Gestion, a SGP approved by the AMF under No. GP03-004, 21 Avenue Kléber, 75116 Paris. CP202103. PM 3553

To access the site, click HERE.

{kind=link}