In our last note, we highlighted that most major economies were ending 2024 in a “Goldilocks” zone – not too hot (inflation and labor markets), not too cold (economic growth) – and they’re set to enter 2025 with solid momentum.

For the U.S. in particular, 2025 could be a year of change, in part because of the election. So we want to look at what proposed policy changes could mean for the economy.

The U.S. election is expected to add to uncertainty

President Trump’s 2024 election campaign included a number of proposals for significant changes to trade and immigration policies, including a 10% across-the-board tariff with 60% tariffs on China and tighter immigration controls, especially for unauthorized immigrants.

All things considered, this isn’t all that different from the policies we saw in the first Trump administration, where tariffs were implemented on China, NAFTA was renegotiated, immigration was slowed, and border security was strengthened.

In his first term, Trump used tariff proposals as negotiation tools to win concessions from other countries, so not all proposed tariffs ended up being implemented. Most expect that to be the case in the next four years, too.

However, that is likely to add to uncertainty, particularly for companies with international supply chains. The Trade Policy Uncertainty index spiked under the first Trump presidency and has already risen to new record high ahead of his inauguration (chart below).

President Trump’s platform also includes reductions in tax rates and regulation – both things that are likely to help companies and, therefore, stocks.

Looking at data from Trump 1.0 for to see how Trump 2.0 might work

Recent experience from President Trump’s first term provides examples of what economic impacts we might expect from his second term.

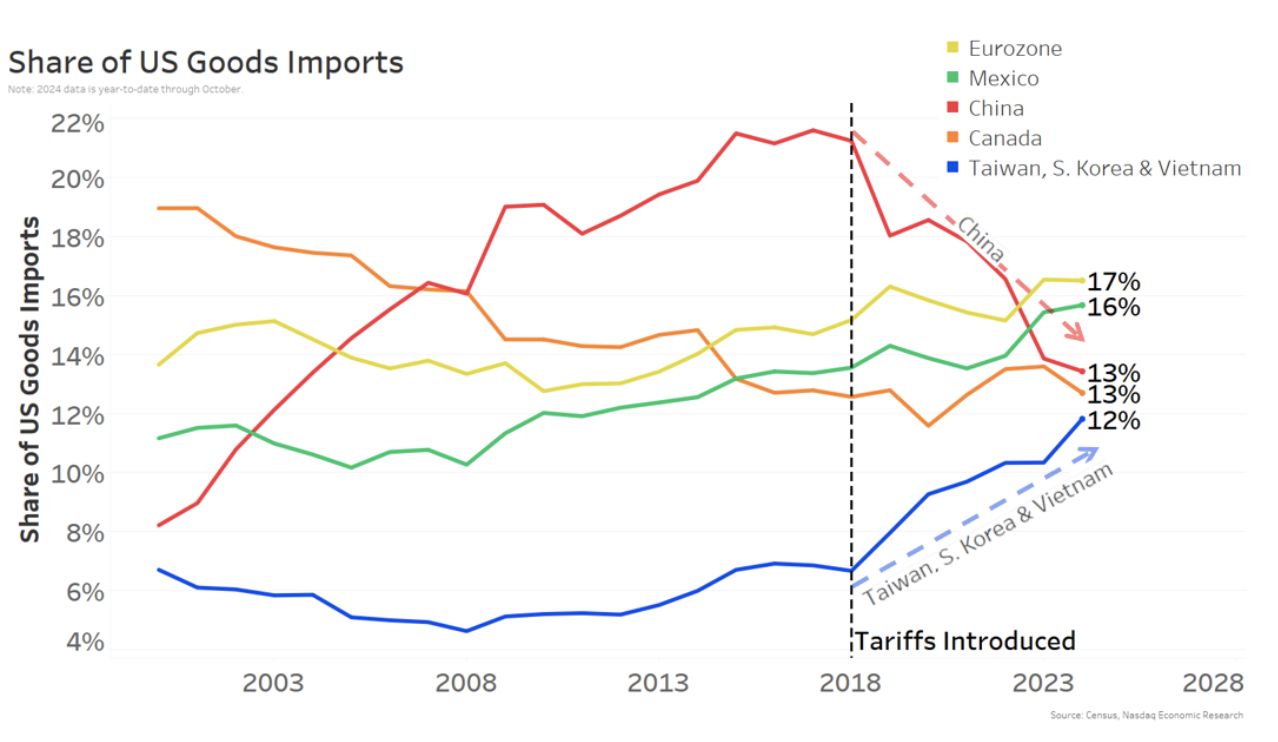

We can start with tariffs, which, in President Trump’s first term, were largely focused on China.

The added cost of importing from China pushed companies to change their suppliers, or supply chains. Over time, this has led to China’s share of U.S. goods imports nearly halving to 13% (chart below, red line).

However, many countries benefited, including China’s neighbors (Taiwan, Korea, Vietnam), as well as Mexico (“nearshoring”) and the Eurozone (“friendshoring”).

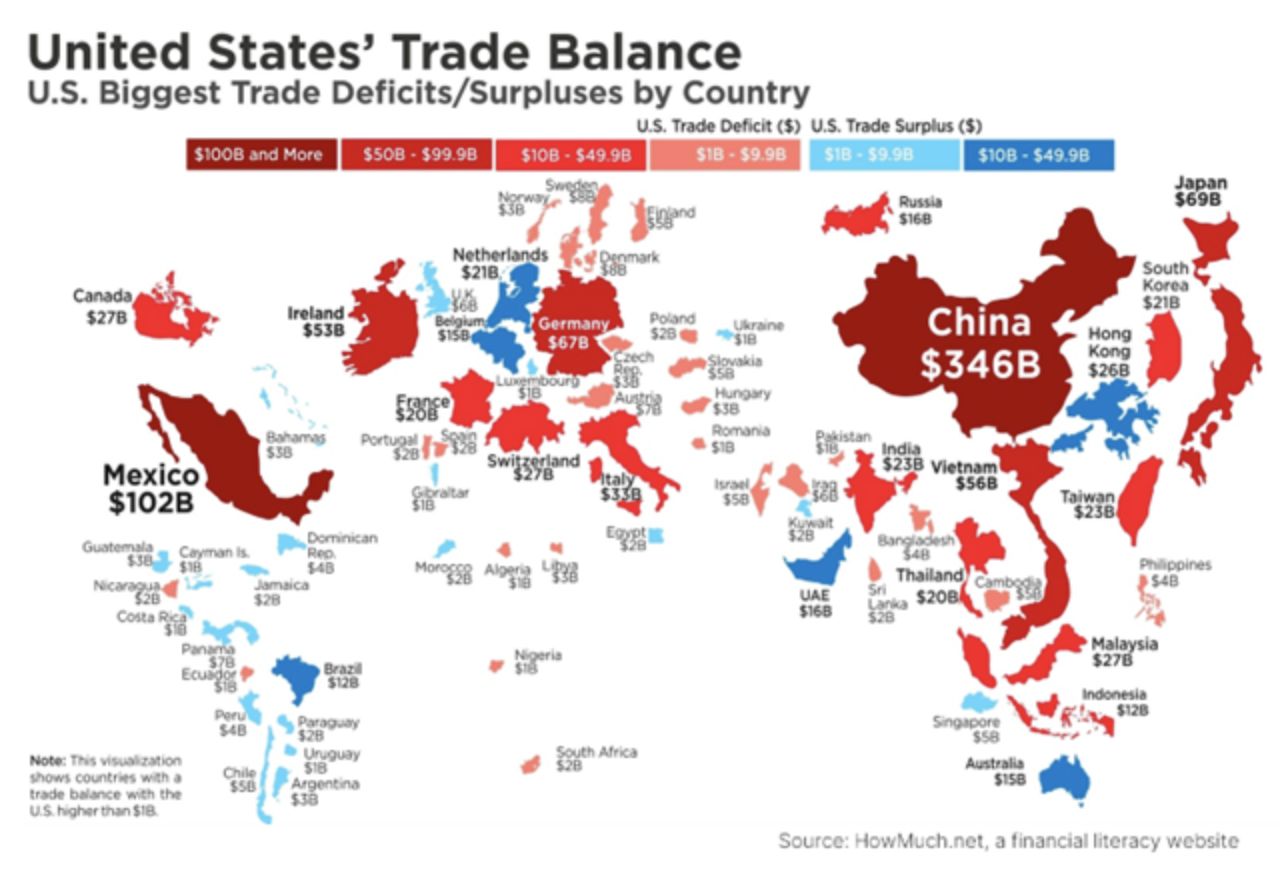

President Trump has proposed much broader tariffs in his second term. Many economists expect Trump to focus on countries with larger net exports to the U.S. as a way to close the trade deficit and fortify U.S. supply chains.

If that’s the case, the chart below shows the countries with the most trade (size of the country) and the largest U.S. trade deficits (darker red). Based on this, countries like Mexico, China and Vietnam are considered most likely focal points. And in fact, Trump has already proposed even higher 25% tariffs on Canada and Mexico.

Importantly, for U.S. companies that import goods from abroad, tariffs would be an added cost. For companies to maintain margins, they will try to pass those costs on to customers.

For that reason, the expectation is that tariffs will add to inflation. Although, there may only be a one-time upshift in prices, and given that the manufacturing sector only represents around 10% of the U.S. economy, the impact on overall inflation might not be as large as many think.

Immigration restrictions could reduce labor supply, boosting wages

Another potential source of higher costs is immigration restrictions. The most obvious impact from tighter immigration controls, and especially deportations, would be a reduction of the workforce.

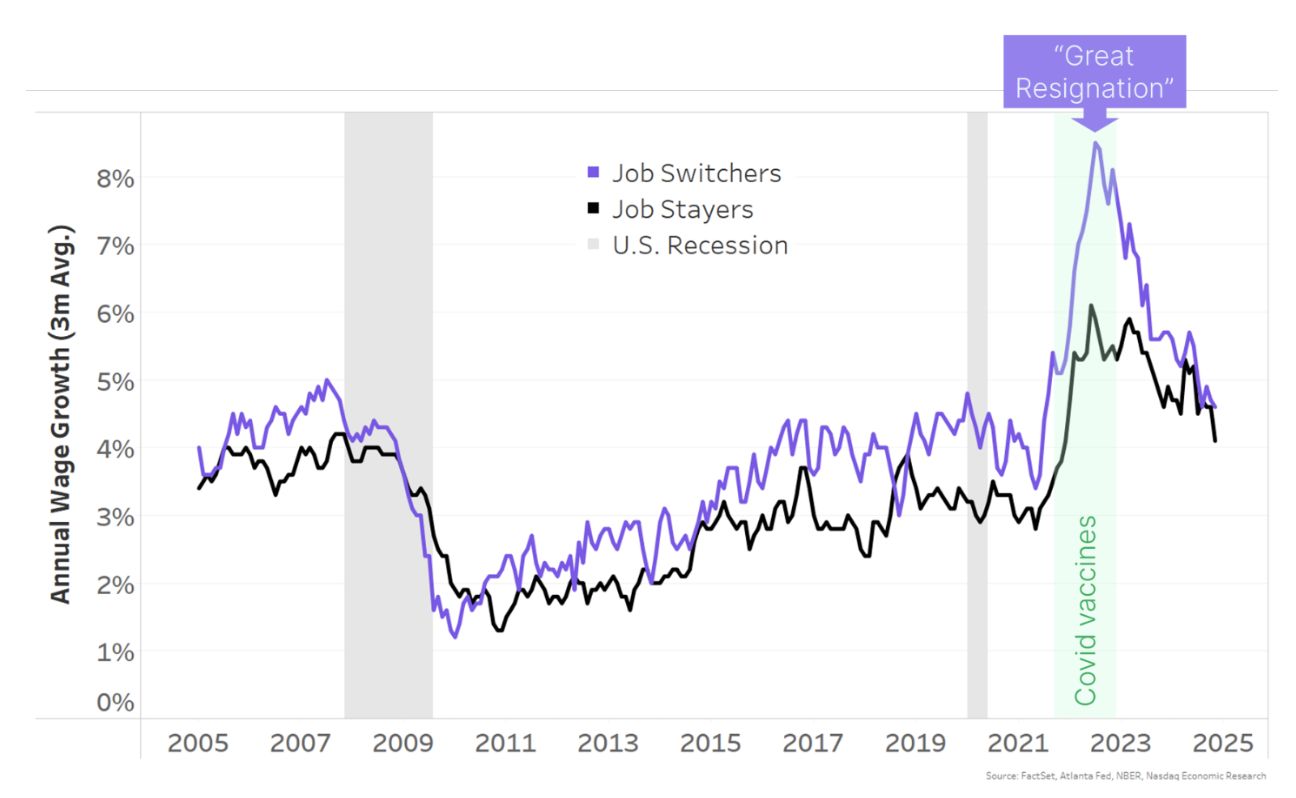

An interesting parallel from the first Trump administration is how Covid affected the economy. Covid reduced labor supply significantly in three ways:

- An estimated 2.4 million people who retired early (rather than risk getting sick).

- Enhanced unemployment benefits let people hold out for the perfect job.

- Visa issuance fell over 50% in 2020 and 2021 from 2019 levels as travel globally was restricted.

Combined, this led to significant shortages of labor once the economy picked up. At the peak of the recovery, once vaccines became widespread, there were two job openings per unemployed person, compared in 1.2 in 2019.

With lots of demand for a smaller pool of workers, people willing to switch jobs were able to earn much better pay. As a result, wage growth increased to 8.5% p.a. in 2022 (chart below, purple line) for job switchers, and also increased for job stayers (black line). Data shows business wage costs increased 25% since 2020, adding to the “sticky” inflation we have seen in 2024.

However, Trump’s immigration restrictions should only be a mini version of what we saw during Covid. By some reports, the U.S. has averaged about 1.4 million unauthorized immigrants per year since 2021, many of which may not yet have joined the labor force.

However, in the case of more widespread deportations, the industries most reliant on unauthorized immigrants are reported to be professional services, leisure and hospitality, construction and agriculture.

Higher wages needed to attract people back to those industries could also add toinflation. However, the consensus is that this would be far more modest than the wage inflation we saw in 2022.

Lower taxes, deregulation & M&A is good for stocks

Most of the other policies that were proposed by Trump’s should increase valuations for companies.

Given President Trump’s pro-business platform, many expect he would reduce regulatory restrictions. That would reduce costs for companies. Since M&A deals usually offer to buy shares at a premium to market prices, the prices for companies who are potential targets for acquisition may rise on the possibility of new deals.

Tax cuts are also expected to boost companies and the economy.

Not only does President Trump want to permanently enshrine his 2017 tax cuts, which are set to expire in a year, but he also wants to cut the corporate tax rate further to 15% from 21%.

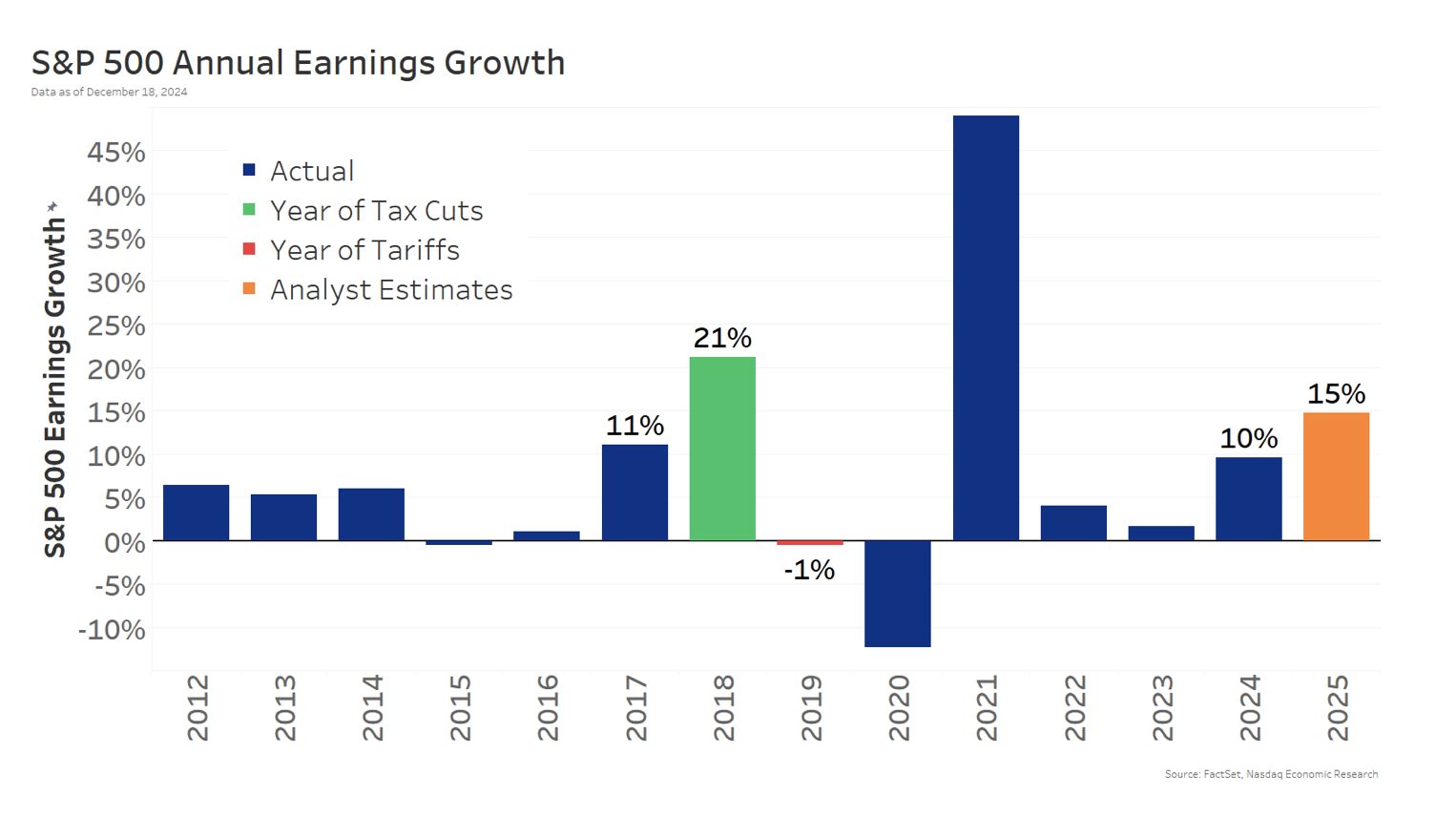

Interestingly, the year after Trump lowered the corporate tax rate to 21% from 35%, we saw a big boost to companies’ earnings, from 11% p.a. in 2017 to 21% in 2018 (green bar below). That’s close to a 1% increase in profits for every 1% cut to the tax rate.

That said, company earnings saw a small (1%) reduction in the year after Trump implemented the majority of tariffs (red bar, 2019).

What are markets saying? Higher growth, inflation and interest rates

The majority of economists think deregulation and tax cuts should boost growth (and companies’ profits). However, tariffs and immigration restrictions are likely to add to inflation, at least in the short term, and may reduce trade and growth over a longer timeframe.

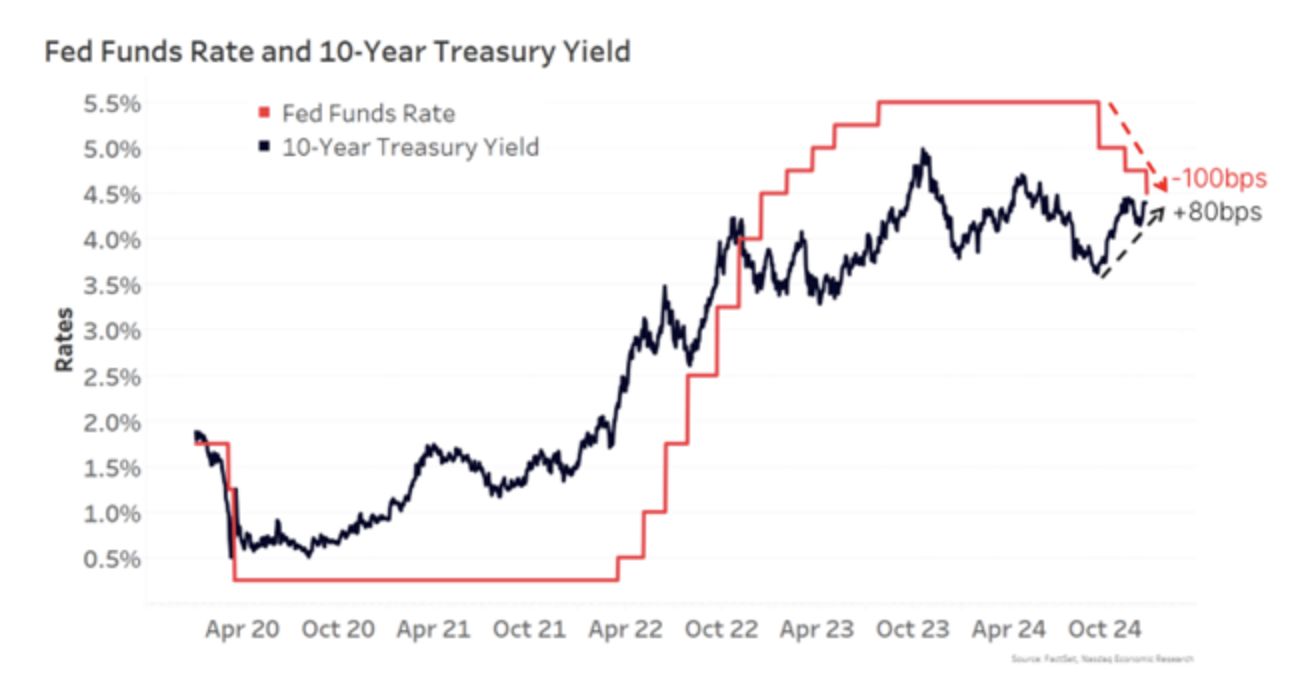

And it looks like markets agree. In the last few months, short- and long-term rates have moved in opposite directions.

We have seen the Fed cut rates 100bps (including today’s 25bps cut) to 4.5% in the last few months (chart below, red line) with further rate cuts expected as rates fall closer to the “neutral” zone – probably somewhere around 3%.

However, at the same time, long-term rates (10-year Treasury yields) are up 80bps (black line). That’s showing that markets are pricing in stronger growth and higher inflation over the next 10 years than we expected before the election.

Given this, markets now expect the Fed funds to fall to 3.95% over the next 12 months – a whole percentage point higher than what was expected in September.

Can the labor market hold up enough for the consumer to keep spending?

The big question is whether those higher rates may slow the economy more than tax cuts and deregulation boost it.

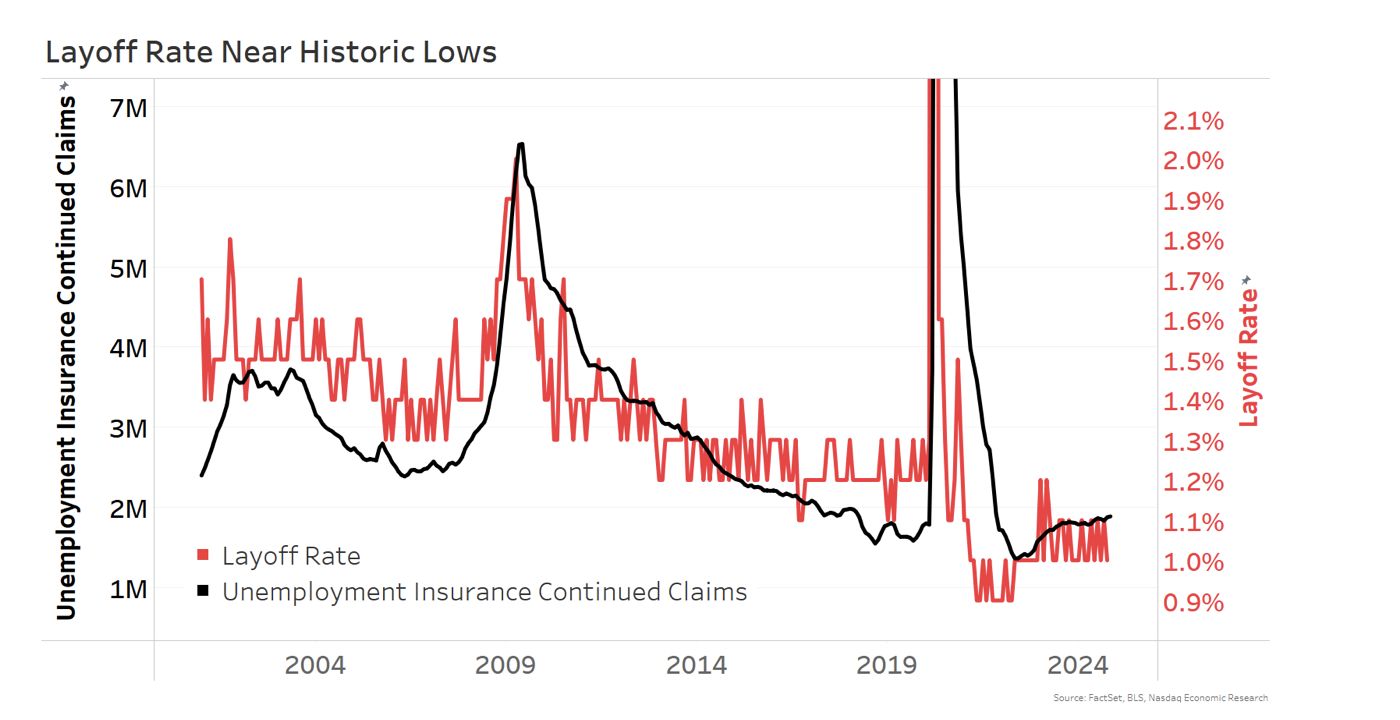

Data shows that higher interest rates have especially impacted smaller companies. Many are paying much higher interest on loans, contributing to an ongoing earnings recession. As a result, small businesses, who also employ nearly half of all U.S. workers, seem to have reduced hiring plans.

But that’s not the main reason why unemployment is rising. Instead, higher wages have attracted more workers back to jobs. In fact, companies remain hesitant to lay off workers with the layoff rate near all-time lows (chart below, red line).

U.S. consumer spending is the main reason the U.S. economy has been stronger that many other advanced economies. That strength seems to now be coming from the strong jobs market and rising wages.

For the economy to hold up in 2025, we need the labor market to stay strong.

Further interest rate cuts, combined with tax cuts, might be just what we need to keep the U.S. economy growing for at least another year.

The information contained above is provided for informational and educational purposes only, and nothing contained herein should be construed as investment advice, either on behalf of a particular security or an overall investment strategy. Neither Nasdaq, Inc. nor any of its affiliates makes any recommendation to buy or sell any security or any representation about the financial condition of any company. Statements regarding Nasdaq-listed companies or Nasdaq proprietary indexes are not guarantees of future performance. Actual results may differ materially from those expressed or implied. Past performance is not indicative of future results. Investors should undertake their own due diligence and carefully evaluate companies before investing. ADVICE FROM A SECURITIES PROFESSIONAL IS STRONGLY ADVISED. © 2024. Nasdaq, Inc. All Rights Reserved.