In my bulletin of January 19, 2024 entitled “The Fed had not won the war against inflation”, I wrote: “The increase in inflation is certainly likely to complicate the task of the Fed when making the decision that the markets have been anticipating for several weeks: stock market performance can be explained exclusively by the Fed's promise of a rate cut.”

I also added: “Overall, the market does not seem to be factoring in the risk of supply disruptions for raw materials at all. However, this risk constitutes one of the essential elements which could radically change the situation in terms of inflation.”

Twelve months later, the risk of disruption remains largely absent from valuations, and commodity prices, with a few exceptions, have remained surprisingly depreciated throughout 2024.

Agricultural raw materials, such as coffee, orange juice, chocolate or eggs, have recorded a spectacular increase in recent months, mainly due to factors specific to these markets, such as drought or avian flu. In contrast, metals have not performed remarkably well this year, as investors appear to rule out the possibility of short-term shortages.

Concerning metals, investors seem to largely neglect the risk of shortage… until it becomes reality, as was the case in 2024 for germanium, gallium and, more recently, antimony:

China has the capacity to cause metal prices to fluctuate, even if only by deciding to ban their exports. Controlling the transformation of almost all metals, it exposes these markets to a significant risk of price surges, particularly in a context of trade war. For the moment, this risk remains largely underestimated by the markets. For example, copper closes 2024 at the same level as at the start of the year:

Copper has even lost $1 since its June highs.

Futures sellers on this metal anticipate a more marked slowdown than expected in China. These bearish speculators are influenced by the evolution of Chinese bond yields.

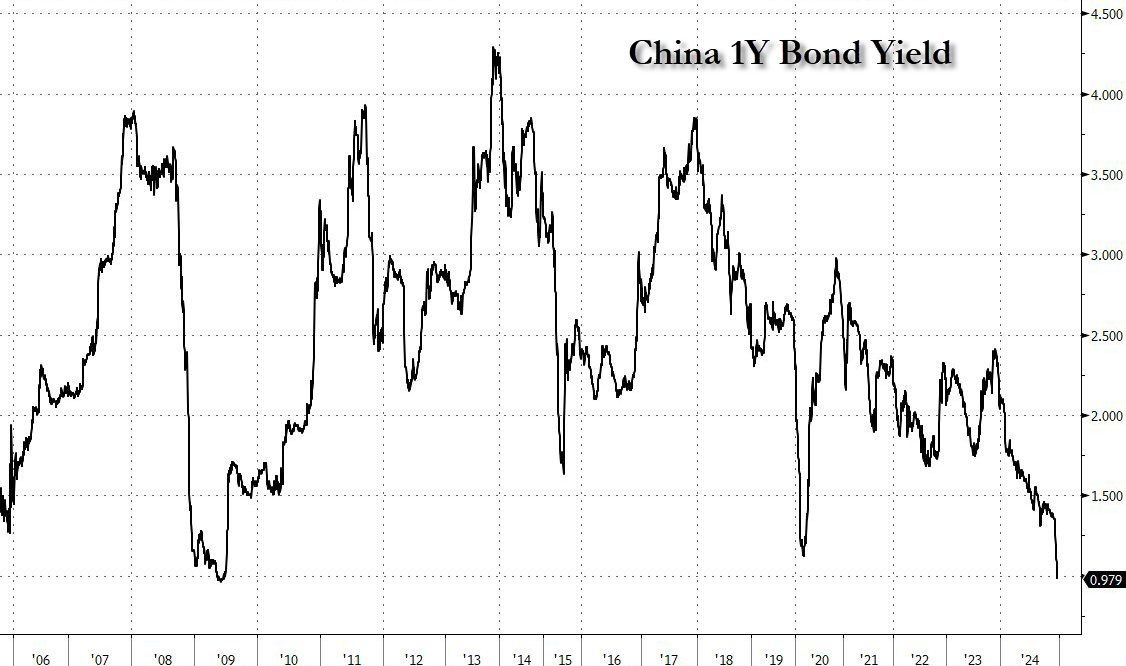

1-year yields in China have collapsed this year, reaching levels comparable to those observed during the great financial crisis of 2008. They even fell below the values recorded during the Covid crisis in 2020:

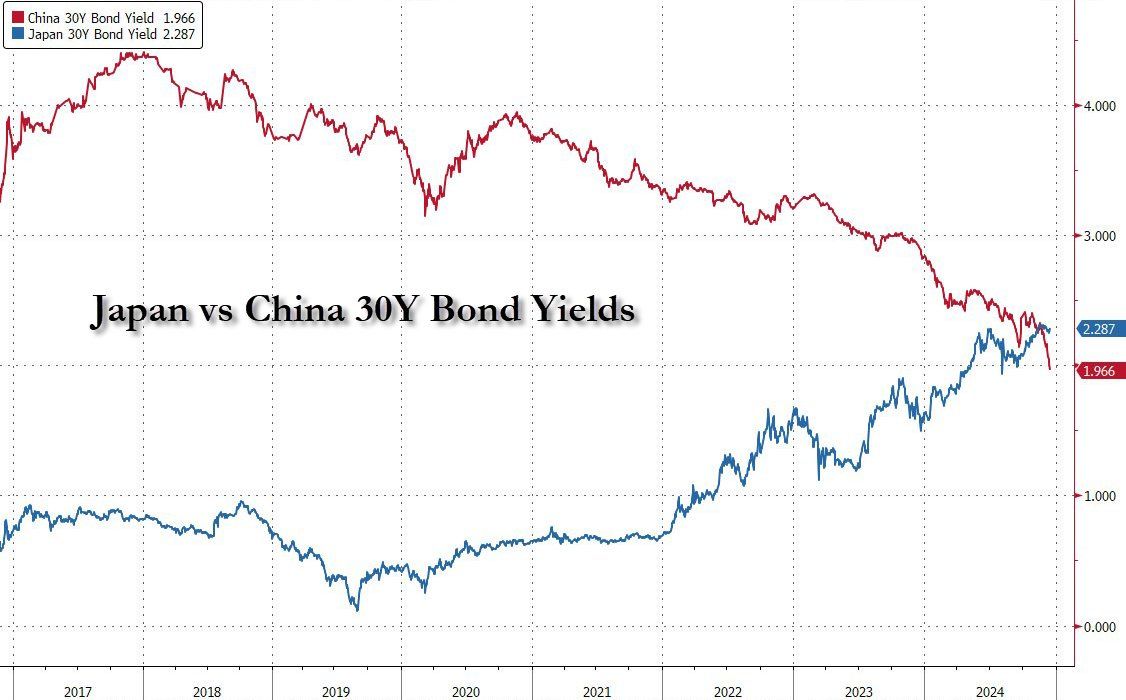

The Chinese 30-year-old has just fallen below the Japanese 30-year-old for the very first time:

It should be remembered that in 2014, the Chinese 30-year yield was at 5%:

The Japanese 30-year-old was at 0% in 2016:

In my bulletin of February 9, 2024 entitled “China: the deleveraging process has begun”, I wrote: “The real estate sector represents a quarter of China's GDP, however, high leverage levels suggest that the The sector's deleveraging process could lead many banks into a deflationary spiral.

According to analyst Kyle Bass, who is quite critical of China, there is even a broader systemic risk within the financial system and the Chinese economy, this danger being associated with the colossal debt of the real estate sector of the country”.

At the end of 2024, investors remain convinced that China is following a trajectory of “Japanization”, characterized by an imminent demographic collapse and persistent risks in the real estate and banking sectors. These challenges could require a massive “Japanese-style” support plan in the years to come.

These concerns about China are likely behind the increase in gold ETF assets this year.

In my April 9 newsletter titled “Gold ETF Rush in China,” I featured this chart of China’s most popular gold ETF:

Eight months later, the assets of this ETF continue to soar:

The situation is completely different in the United States, where growth prospects have never been in question in 2024. The strength of the American economy, supported by massive government spending plans and an abundance of liquidity, has even raised real awareness about inflation.

At the beginning of March, Janet Yellen, the United States Treasury Secretary, surprised the markets by admitting that she regretted having described inflation as “transient”.

In Europe, inflation in 2024 is all the more worrying as it is accompanied by a clear economic slowdown.

In my bulletin of February 2, 2024 entitled “Europe paralyzed by the first inflationary shock”, I wrote: “The recent surges in inflation have plunged the continent into an unprecedented situation of blockage: the mobilization of farmers mainly finds its origins in the repercussions of the generalized decline in purchasing power observed in Europe in recent quarters. However, according to Brussels, one of the solutions to counter inflation also involves the negotiation of free trade agreements in order to contain the rise in prices of agricultural raw materials. But these agreements are very unfavorable for farmers who have already seen their real wages collapse in 2022 and 2023. The anti-inflationary remedy is worse than the disease! In the past, opening borders was an effective recipe for containing rising prices. However, now that inflation has woken up, this approach no longer works.”

Eleven months after the farmers' revolt in Europe, nothing has been resolved regarding inflation and the causes linked to the explosion in energy costs on the continent.

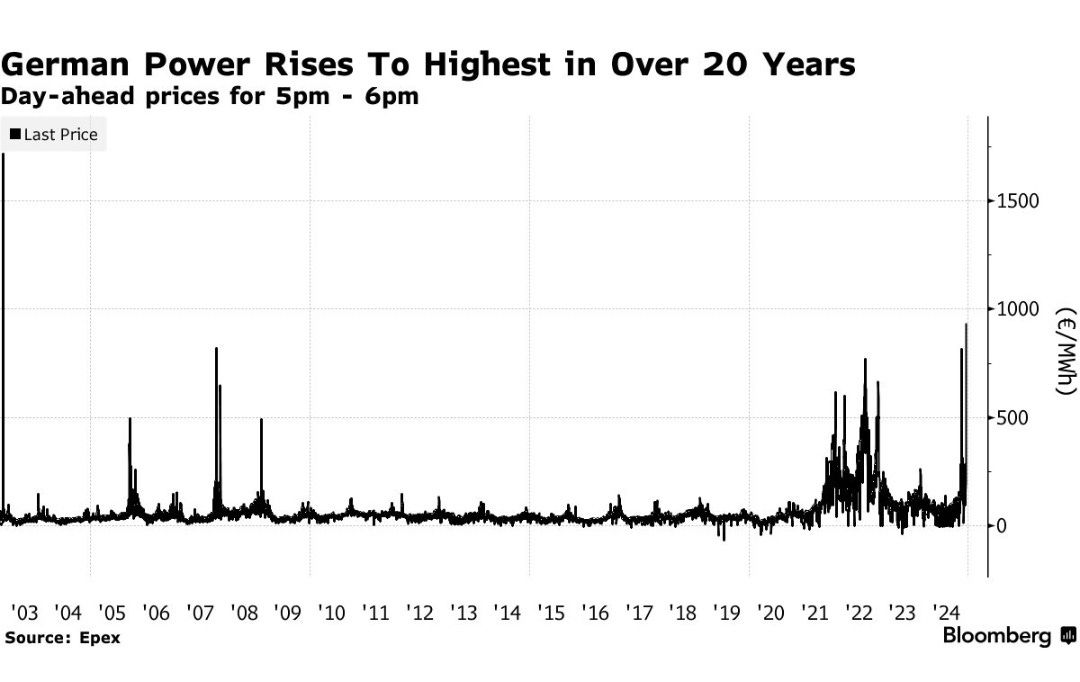

Electricity prices in Germany have risen sharply in recent days, reaching levels not seen since the 2022 energy crisis, due to low wind power production. Electricity imports hit their highest level in a decade on Wednesday, forcing gas and oil plants to step in to meet demand. Prices have exceeded €1,000 per megawatt-hour and remain extremely high:

Stagflation has taken hold in Europe in a lasting manner in 2024, but paradoxically, the European saver remains for the moment very passive in the face of the risk posed by the threat of this coming stagflationary period on the value of bond assets held by savers and on the solvency of the French banking system.

In the United States, the inflationary risk also intensified at the end of the year. The latest PPI figures confirm this rebound in inflation. Therefore, with inflationary expectations rising, it is logical to see 10-year rates soar to new highs again. Despite the rate cut decided by the Fed in September, they returned to their highest level since May:

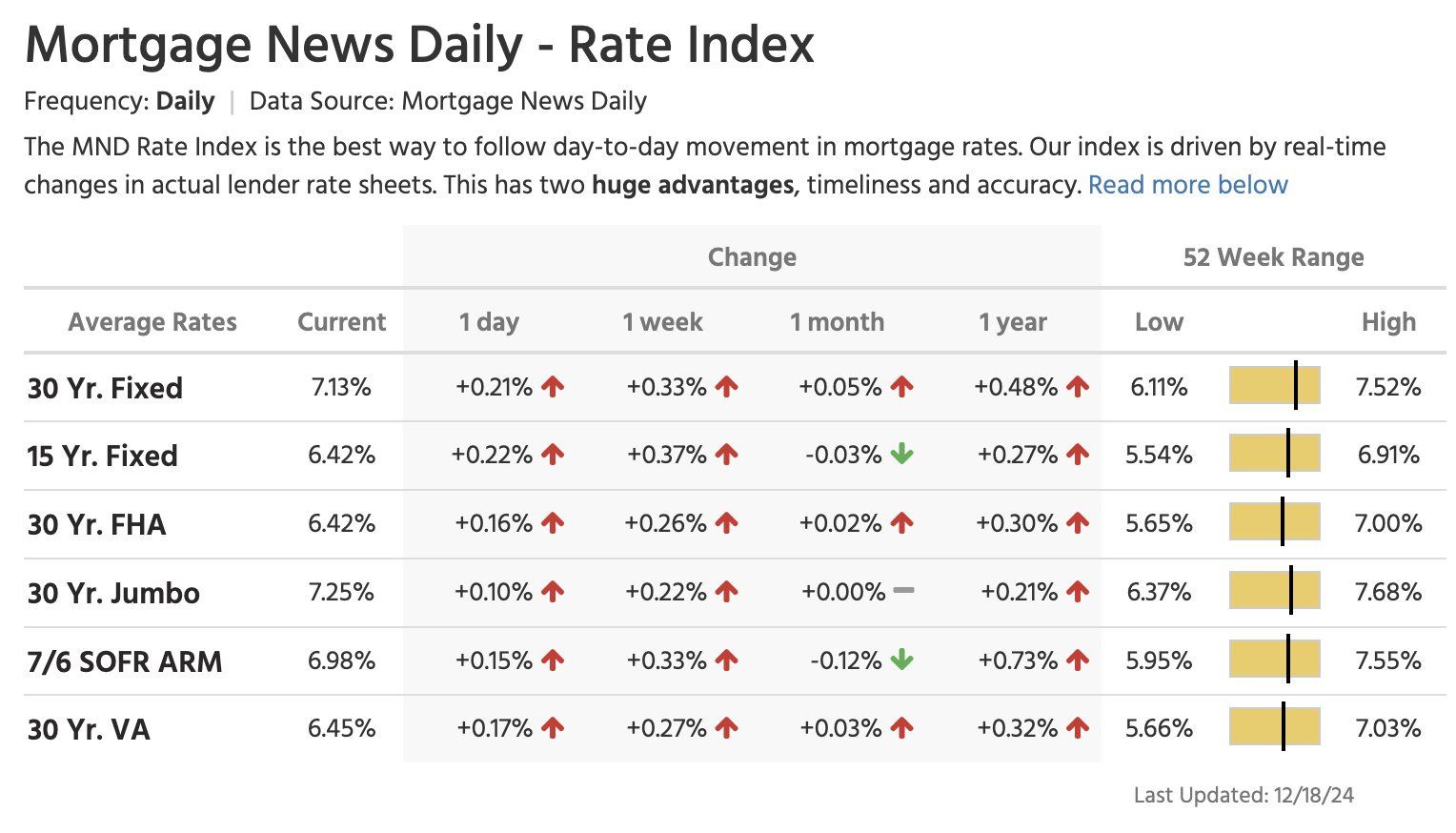

Direct consequence: the American real estate market is once again under pressure.

Last July, I said that the real estate market was paralyzed by high rates. The situation is deteriorating again: the average rate for 30-year mortgages increased sharply, reaching 7.13% after the Fed press conference, compared to 6.65% at the same period last year:

These high rates also represent an immense challenge for the short-term refinancing of American debt.

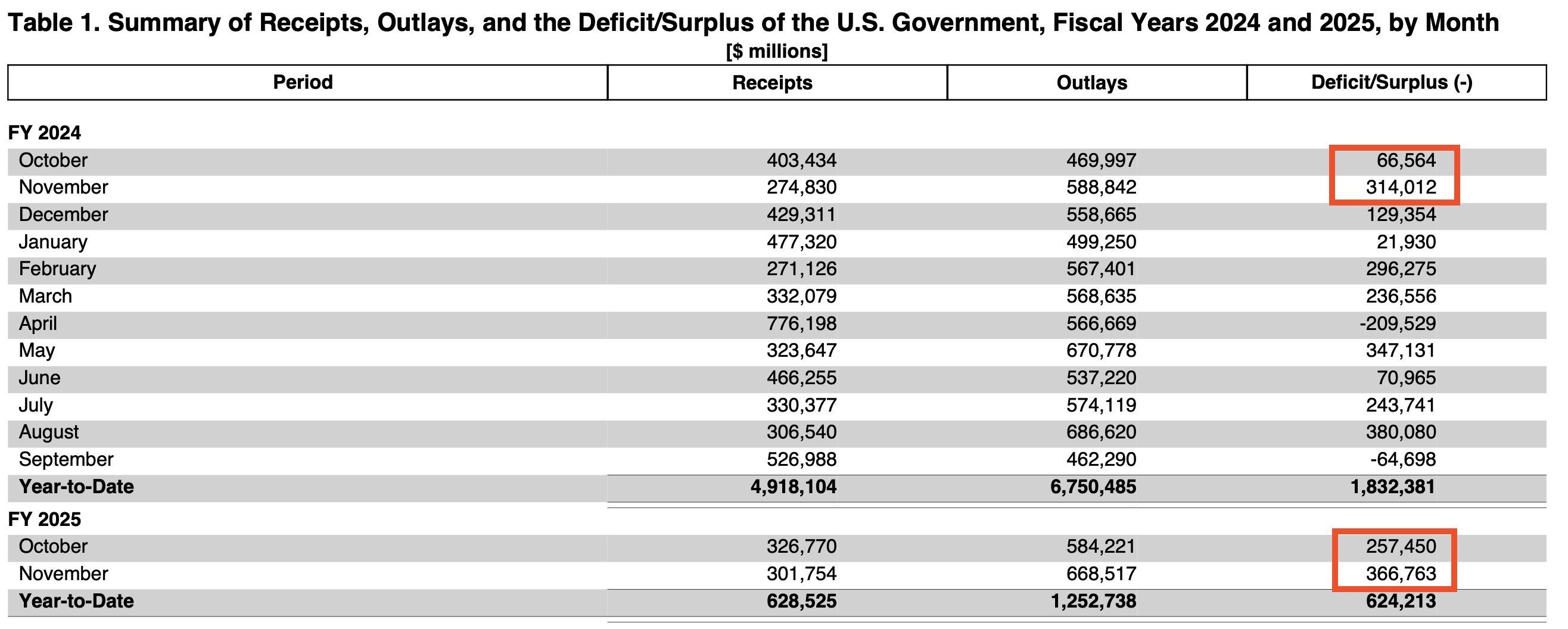

This challenge is all the more colossal as the deficit continues to grow at an alarming rate. During the first two months of fiscal year 2024, the total deficit reached $380.5 billion, an already worrying situation. But over the same period of fiscal year 2025, this figure soared to $624.2 billion, a spectacular increase of 64% in just one year!

A growing part of the debt is now financed by short-term bonds maturing in less than a year. With $2,000 billion in bonds, bonds and notes maturing in 2025, to which are added $2,000 billion in annual budget deficits (and this figure risks being largely exceeded), the gross financing needs reach a total of $4,000 billion.

The need to finance this amount of new debt is the main argument supporting the forecast of a rise in the price of gold in 2025.

Reproduction, in whole or in part, is authorized provided that it contains all hypertext links and a link to the original source.

The information contained in this article is purely informative and does not constitute investment advice, nor a recommendation to buy or sell.

- -