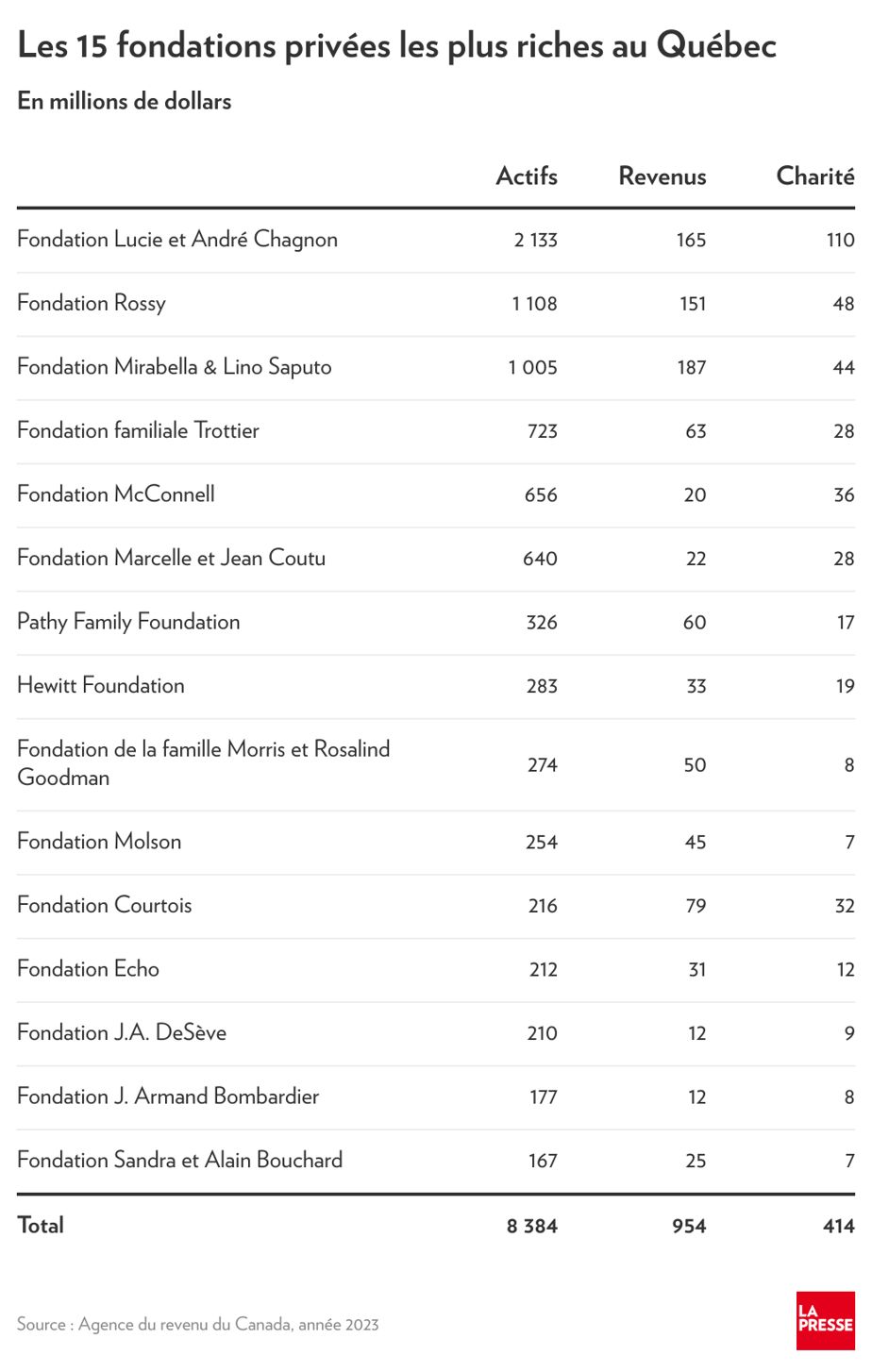

Quebec, with its 950 private foundations, benefits from one of the most generous tax regimes in the world. The 15 richest foundations redistribute on average 5% of their capital or 43% of their income, and voilà, they are “charitable” for tax purposes and pay no taxes for eternity. As a wind of austerity blows across the province, a question arises: do Quebecers benefit from the fiscal pact concluded with the founders and their foundations?

Posted yesterday at 4:00 p.m.

Brigitte Alepin

Tax expert, professor and author

The founder of a private foundation can benefit from a tax credit of up to 53% on their donations. In addition, if these donations are made in the form of certain specific assets, such as shares listed on a stock exchange, he can also benefit from a total exemption from capital gains tax. As for the foundation, it escapes all forms of taxation, including on the income generated by its investments. This exemption contrasts with that in other countries, such as the United States, where foundations are subject to taxation on their investment income.

A charity frozen in time

In return for these generous tax gifts, the foundation is required to devote at least 5% of its capital each year to charitable purposes, and its operational expenses are taken into account, in this regard, as charitable expenses.

Why 5%? Because most large foundations are designed to last indefinitely, in accordance with the wishes of their founders. Therefore, with a 5% charitable spending requirement, only income generated by capital is allocated to charitable actions, which helps preserve the integrity of capital.

The Chagnon Foundation illustrates this dynamic well: it began with a donation of $1.4 billion in 2000, and its assets reached $2.1 billion as of December 31, 2023. The situation is even more striking with the MasterCard Foundation , launched in 2005 and today with assets of nearly US$42 billion. Thanks to a special arrangement with the Canada Revenue Agency, it benefited from a 15-year “charity break” – from 2007 to 2021 – which allowed it to postpone its redistribution obligations. During the same period, the MasterCard Foundation allocated an average of 2.67% of its assets to charitable purposes, while its total value grew by an impressive 1,600%.

Since the first civilizations, humanity has aspired to eternity, an ideal that is nourished by lasting structures. As early as ancient Egypt, where survival after death meant the construction of temples dedicated to the deceased, financial structures were put in place to guarantee their preservation over the ages. But at the time, this wish for eternity was not financed by other taxpayers: taxation of the living was not used to satisfy the desires for immortality of the elites.

The real problem with eternity is that it is difficult, if not impossible, to be both eternal and charitable. In other words, if an organization limits itself to redistributing 5% of its resources to preserve its capital in perpetuity, it cannot claim to be truly charitable. And if 5% is enough to merit the title of “charitable”, this would mean that a large proportion of Quebec taxpayers should also be considered “charitable” for tax purposes, since their contributions in the form of taxes, consumption taxes , property tax and social security contributions far exceed 5% of their assets.

-When will Quebecers start to “win”?

Under the current tax system, taxpayers must wait an average of 35 years before a foundation’s charitable actions exceed the tax benefits it and its founders receive (calculated on a present value basis). For donations in the form of shares listed on a stock exchange – representing approximately 12% of donations in Canada – this period can reach up to 100 years.

For example, since its creation in 2004, the Rossy Foundation has distributed approximately $250 million in donations, while the cost to public finances of the tax advantages granted to the founders and the foundation amounts to $345 million. This amount could be higher if the donations had been made in the form of shares of listed companies, as seems to be the case, because the forms submitted to the Canada Revenue Agency mention shareholdings in Dollarama. It is also worth noting that these forms reveal that the foundation holds several equity interests in companies incorporated in the Cayman Islands.

In summary, it is largely taxpayers who finance the creation and operation of these so-called “charitable” structures, while the founders and their foundations benefit from their influence by interfering in public issues, receive distinctions, such as medals, and have their names associated with many public buildings. For example, on January 9, 2025, the McCord Stewart Museum inaugurated the “Rossy Foundation Space”, which includes three new rooms, made thanks to a donation whose value has not been disclosed, as has the cost total project.

The solutions

The solutions are simple: increase the distribution percentage of foundations beyond 5%, gradually reduce the tax advantages granted to founders and introduce some form of taxation on the foundations’ returns.

These adjustments are possible, especially since foundations can hardly threaten to go into exile in the face of a fiscal tightening. A move could result in their registration being revoked and then assets being distributed to eligible donees (excluding foreign organizations).

However, a key measure to ensure the integrity of the system is to increase the number of tax audits. Only 196 tax audits were carried out for the 2023-2024 fiscal year, on nearly 86,000 charities in Canada. The tax gifts these organizations benefit from are very significant and it is imperative to intensify tax controls in order to avoid abuse and ensure that foundations truly fulfill their social mission, and not private or financial objectives.

As long as governments continue to tolerate this system, the gap between private wealth accumulated in foundations and public needs will continue to widen.