Behind the facade of an economy in apparent resilience, the financial situation of the Fed reveals worrying flaws. With record losses and monetary policy under pressure, the future of the greenback as a safe haven could be called into question…

This year, all eyes on the United States remained focused on the presidential election and the good performance of the dollar.

It must be said that between the withdrawal of Joe Biden and the overwhelming victory of Donald Trump, there was no shortage of dramatic events. And with a performance of almost +6% compared to the euro, the greenback proved the lie to the Cassandras who predicted a collapse of the American currency.

It was enough for political and economic commentators to predict, at the end of the year, a return eight years ago. As if Trump's second term could be equivalent to the first, but supercharged, and that Wall Street could hope for a year 2025 equivalent to 2017. After a crazy year 2024 for the American indices, no investor would be choosy about the 22%. increase on the S&P 500 which crowned the first year of Donald Trump's reign.

But the situation is very different from that of eight years ago. After years of quantitative easing, the rate hike decided by the Fed weighed down its balance sheet. With more than $5.7 trillion in Treasury bonds in its portfolio, it was inevitable that rising interest rates would force the institution to incur unrealized losses. And, with the remuneration of deposits higher than that of its assets held, the passage of time would not improve things.

Faced with this mathematical evidence, the Fed anticipated the criticism and quantified the cost of the rate hike cycle. But in view of the latest quarterly figures, the estimate was more than optimistic: it turns out to be totally disconnected from reality.

The hole in the balance sheet now exceeds $213 billion, compared to its $43 billion in equity. It is only through an accounting artifice that the Fed manages to maintain a facade of solvency.

The monetization of Treasury deficits had the advantage of displacing Uncle Sam's insolvency. By reporting the budget deficit in the balance sheet of the Central Bank, although it is supposed to be independent, Washington is now placing its budgetary negligence on all of the countries. dollar users.

Fictional budgetary rigor

It is obvious that the Fed is not a legal entity like any other, and that the authorities have no interest in forcing it to recapitalize or to go bankrupt.

In practice, as long as the Fed is allowed to operate with negative equity, the hole in its balance sheet simply represents a monetary injection in disguise.

The scale of the American budget deficit is no secret. But, according to the Central Bank, the year 2022 was supposed to have marked the end of monetary laissez-faire. With the rise in key rates, money printing had to come to an end and the Fed had to return to good practices.

In fact, the holding of Treasury bills, which doubled at the start of the pandemic and increased by another 50% between 2020 and 2022, has been declining for two years now. But more than proof of the end of debt monetization, this smoothing of the curve is mainly due to the drop in value of Treasury bonds held due to the rise in rates.

Over the first nine months of the year, the Fed received an average remuneration of 2.21% on the Treasury bills it holds in its portfolio. At the same time, it accepted deposits paid at 5.28% on average. Due to this unfavorable jaws effect on the cost of money, it received $121.6 billion in interest while it paid $178.8 billion in deposits, a loss of nearly 60 $ billion over nine months.

An underestimated loss of 500%

The most worrying thing is not so much the scale of the deficit, which is all in all consistent given the mountain of Treasury bonds held before the rate hike, but rather the FED's inability to estimate it.

In a note published in February 2022, she estimated the cost of the rate increase in the form of a probabilistic calculation. A remarkable exercise in transparency, and – on paper – much more rigorous than the peremptory forecasts to which monetary authorities have accustomed us since the subprime crisis.

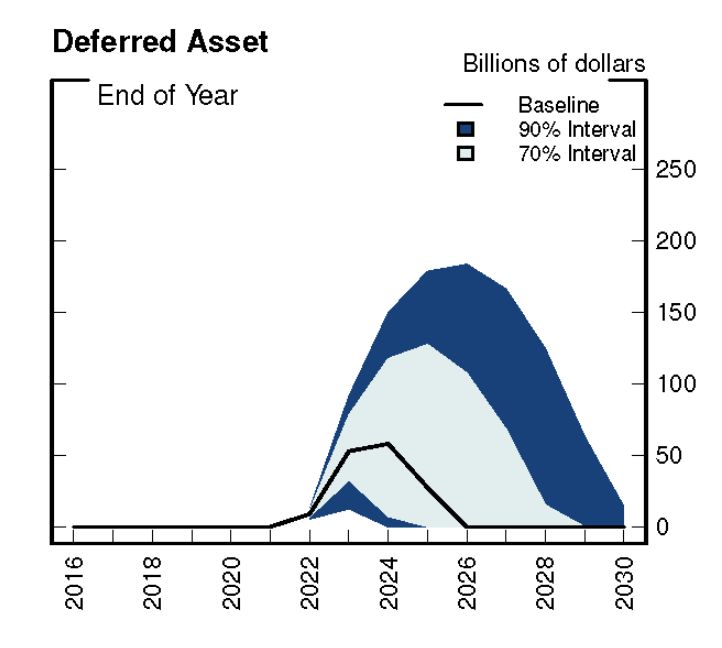

In the base scenario, the loss was expected to peak at $50 billion in 2024, before dropping below $20 billion from the summer of 2025. In the less favorable case, the probability of which was estimated at 70%, the loss would peak at $125 billion in 2025. Finally, in the worst scenario, it would stabilize at $210 billion. A worst-case scenario which, according to the FED's precisionists, would have less than a 10% chance of happening.

Scenarios for the evolution of losses on Treasury bills: median scenario (in black), unfavorable hypothesis (70% confidence interval, in light blue), very unfavorable hypothesis (90% confidence interval, in dark blue). Source : Fed

But with a loss that exceeds $213 billion as of December 20, 2024, the worst-case scenario has already been largely exceeded. The curve will only bend when the average return on treasury bonds held exceeds the average return on deposits. Unless there is a sharp reversal in monetary policy, this will not happen before 2026. At the current rate, the loss could well exceed $300 billion.

Evolution of gains and losses observed since the pandemic. Source : Fed Saint Louis

The Fed would thus find itself with a hole in its balance sheet representing more than five times its equity, and more than 10% of the value of Treasury bonds held.

Time will tell if the rest of the planet continues to modestly avert its eyes from the insolvency of the Fed, and persists in considering the dollar as the ultimate safe haven.

If confidence breaks, the greenback's outperformance against other currencies will end. We may only be one shutdown or a tense vote on the American budget of this awareness.