Add

Article added

Download PDF

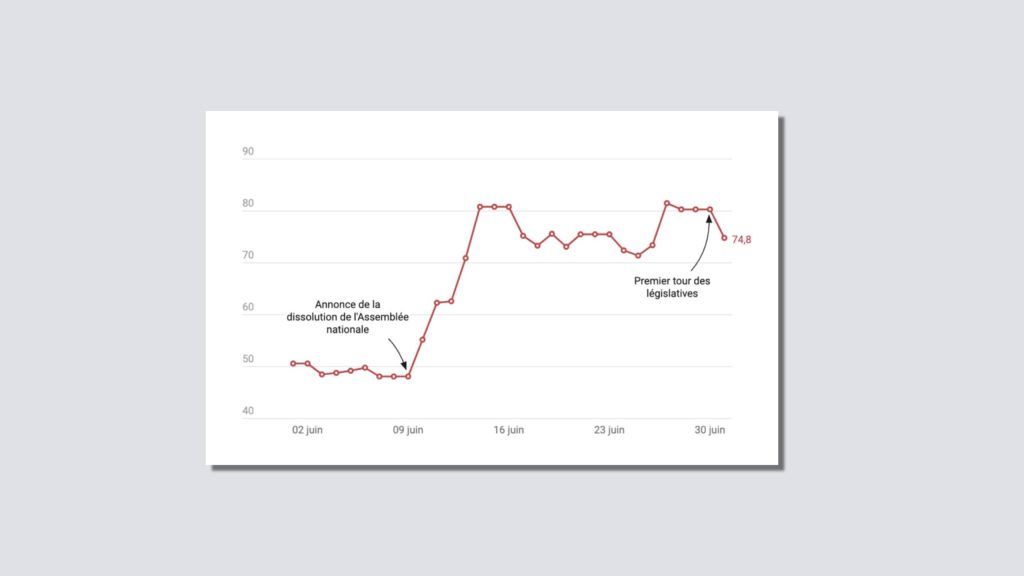

On Monday, June 10, the day after the European elections and the announcement by French President Macron of the dissolution of the National Assembly, the French economy experienced a negative shock.

- The CAC 40 opened down, the spread (the spread between French and German 10-year government bond yields, a key indicator of France’s credit risk) had widened and the euro had depreciated against the dollar.

- It was difficult to interpret this reaction, except that the markets saw a great risk of instability in the French economy.

It was still necessary to know what instability was involved. Several economic analyses, notably from financial institutions, have established a hierarchy of possible scenarios following the second round scheduled for July 7. We reviewed the different positions, consulting documents reserved for investors and conducting semi-directional interviews.

Worst case scenario: NFP majority

We almost always find the same conclusion: the worst-case scenario is that of a majority – absolute or relative – in the colours of the New Popular Front (NFP).

- For one of the major American investment banks, whose magazine was able to consult a document reserved for investors, such a situation would result in a spread by 130 basis points, compared to 48 before the dissolution was announced.

The intermediate scenario: “the majority of the RN would not present a major risk”

Further on, there were scenarios with a National Rally (RN) majority, judged much more favourably by several key players.

- A leading financial player, for example, considers that “a far-right majority would lead to a watered-down fiscal expansion Melon ».

The preferred scenario: a blockage of the National Assembly

The preferred scenarios seemed to be either those of an absolute majority Together (now unthinkable), or those of a political impasse.

The political impasse is preferred by the markets, at least in the short term, since, on the one hand, it will push very opposed parties to compromise in an attempt to govern together fragilely and, on the other hand, it will avoid major economic turning points. At the end of the first round of the legislative elections, with the announcements of withdrawal and a Republican front, the most credible scenario is in fact that of an absence of an absolute majority – which would exclude first a government led by Jordan Bardella, as he declared.

Numbers and letters

In fact, economic indicators have regained some colour at the start of the week:

- Compared to Friday at 5:30 p.m., the CAC40 closed at +1.5% on Monday July 1, driven mainly by French banks which experienced a rebound.

- The spread fell to 74.8 basis points from 80.3 on Friday.

- 1 euro was trading at 7:30 p.m. on Monday for 1.0735 US dollars, compared to 1.0722 at the same time yesterday, a slight increase of 0.12%.

However, we should not underestimate the hypothesis of an RN government majority at this stage. Ahead of the 2022 legislative elections, the polls gave the RN a lower number of seats than the party with the flame subsequently actually obtained at the polls. The markets have understood this well. And in this perspective, they largely prefer Bardella to Mélenchon. Several reasons can explain this:

- The RN’s economic program seems excessive in the eyes of many economists, unfunded, and unlikely to bring France back to a balanced public finances, but to a lesser extent than that of the NFP. Even some moderate economists like Olivier Blanchard have declared this.

- In the final days of the campaign, the RN gave up several key elements of its program, such as retirement at 60, at the cost of many contradictions. This may have reassured the markets.

The limits of the “Meloni” scenario

More significantly, several financial analysts seem to see in the RN in government a “Meloni” scenario.

- “If, during meetings, Bardella is insolent, populist, nationalist and presents himself as a new creature of the RN, when he addresses the media or his international interlocutors, he tends to want to reassure his most qualified interlocutors: no Frexit, a reasonable economic policy, no witch hunt against bankers, big industrialists and senior civil servants.”

However, it should be noted that unlike Meloni’s coalition government, the hypothesis of a Bardella government does not include, as in Italy, economic elites from the liberal centre-right, who are several times ministers and quick to reassure the markets.

- Moreover, unlike the Meloni government which is at the heart of the European political game, Bardella has also initiated several conflicts with the Union, of which his desire to reduce the French contribution to the European budget by 2 billion euros is just one example – not to mention the geopolitical dimension of the RN program which would inevitably affect French economic positions.

Whatever the reaction of the markets next Monday, the RN having recently shown itself to be contradictory, hesitant and evanescent in economic matters, it is not certain that it will be able to provide a guarantee of stability in the medium to long term. The other scenario – that of the absence of a parliamentary majority – could certainly reduce the vicissitudes of French public action, but Parliament will have to vote on a budget and a policy in the autumn in the context of a procedure for excessive deficit – it remains to be seen who will defend it in front of the hundreds of new deputies.

{kind=link}