Mutual insurance contributions have continued to increase since 2023. The causes do not lie only in the increase in health expenses. This continued growth has significant impacts on households. Decryption and analysis of the consequences.

Mutual insurance companies announce an increase in their contributions of 6% in 2025. Each year, the same reasons are put forward to explain these price increases, but they are increasingly struggling to justify such an escalation.

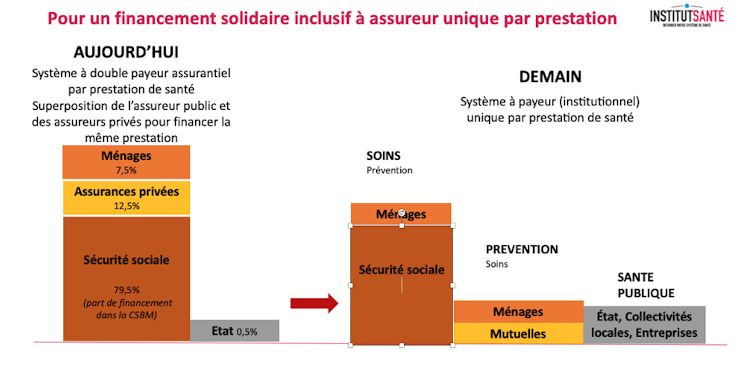

Given the financial difficulties of Medicare, a comprehensive reform of health financing is necessary.

False notes from mutual insurance companies

The 20% increase in contributions between 2023 and 2025 far exceeds inflation (8.8%) and the national health insurance spending target (9.1%). Neither the rise in the cost of living nor that of health expenditure justifies such a difference. Every year, the mutual sector interprets the same score, with its usual notes. The causes put forward to justify the increases are the aging of the population, the rise in prices, the transfer of health insurance expenses or even the implementation of 100% health.

Although aging increases health care costs, it is the public insurer that bears the brunt. Chronic patients, reimbursed 100% by the latter, nevertheless continue to contribute to mutual insurance companies. This transfer of charges represents a gain of 3.5 billion euros for complementary companies since 2012.

Furthermore, individual contracts for retirees, much more lucrative than collective contracts for workers, make aging generally favorable to mutual insurance companies. First false note.

Lower prices in France

Concerning the price argument, the increase in health spending is based 80% on the increase in volumes, and not on prices, which have increased “only” by 0.6% per year since 2013. Prices health goods and services in France are even 30% lower than the OECD average.

This reality greatly benefits mutual insurance companies, which mainly reimburse services whose prices are falling in real value. Second wrong note.

The marginal impact of 100% health

Expenditure transfers are a reality in certain years, such as the 30% to 40% increase in dental user fees in 2023, the additional cost of which is of the order of 450 million euros per year.

However, this additional cost is largely offset by the reverse shift in co-payments for chronic patients on the one hand and cannot explain the 6% increase in 2025, which contains none. Third false note.

From 2023, the impact of 100% health has become marginal. In addition, this measure has favored the commodification of these goods and services with mercantile promotions devoid of ethics, such as “2 pairs for one euro more”. These excesses from which some benefit are unduly paid for by everyone. Fourth false note.

An incomplete score

Among the mutual arguments, some seem curiously forgotten: management fees and reimbursements for alternative medicines for example. However, the former exceed 8 billion euros in 2023 (20% of contributions), up 3% per year since 2011 (i.e. more than 2 billion €). They are mainly due to communication expenses (€3.5 billion). It’s a high price for the insured!

Management costs for supplementary health insurance and health insurance in €m since 2011

Provided by the author

Source: Drees – Health Institute

Concerning alternative medicine, the generalization of a flat rate offer of 50 euros per session of a service not recognized by scientific authorities costs more than a billion euros to policyholders. This choice of reimbursing a chiropractor better than a medical specialist should not be imposed on 96% of the French population.

An increasingly unbearable burden for the middle class

The frantic increase in mutual insurance contributions affects the French population in different ways, but its macroeconomic impact is undeniable. In 2025, contributions will reach nearly 56 billion euros, or around 2% of GDP, a significant levy for households and businesses.

The first affected by this inflationary spiral are retirees, who finance 100% of the contributions of their individual contract, whose annual rate is on average twice as expensive at age 70 (€1,800/year) as at age 40 (€900). ).

Triple penalty for retirees

It’s the triple penalty of entering retirement: a falling income, contributions (financed at 100% and no longer at 50%) which increase twice as fast as inflation, and a quality of contract which deteriorates.

If 56% of workers benefit from a so-called high-coverage class A contract, this is only 11% of retirees, who are among the wealthiest. With an effort rate of almost 10% of disposable income, this middle class of retirees no longer has any financial interest in continuing to pay high contributions for low reimbursements.

These contracts represent an increase in labor costs for employers of around 14 billion euros per year, without bringing any improvement in health at work, which is deteriorating significantly judging by the sharp increase in work stoppages. .

Remember that collective contracts (with C2S) cost the State nearly 10 billion euros per year in the form of tax and social exemptions.

-The urgency of a new financing model

The middle class, particularly retirees, can no longer carry the weight of a system that is running out of steam. The overlapping of a private insurer and a public insurer for the same health service is an economic aberration, which does not exist in any other developed country. Faced with the growing challenges of health financing, it is urgent to imagine a socially and economically optimized model, clearly differentiating the missions of public and private financing.

Health insurance, which we will call health insurance in the new model, will alone guarantee the reimbursement of essential care expenses. A non-insurable co-payment, the amount of which will be revised (around 15%), will be applied to the reimbursement of care.

A redefined role for mutuals

All current exemption conditions (including long-term illnesses, pregnancy, work accidents) will be applied. People on low incomes (including students) will also be exempt from user fees in the new system. In this model, mutuals would devote themselves to the following functions:

-

Additional reimbursement and prevention:

-

Mutual insurance companies will cover services not reimbursed by public health insurance;

-

They will actively finance prevention, via tools such as a personal prevention contract;

-

Strict and fair regulation:

-

Prohibition of any discrimination based on medical criteria:

-

Compulsory and individual affiliation to limit the effects of adverse selection:

-

Subsidy for the most disadvantaged to enable their membership:

-

Introduction of a standard contract:

-

Guarantees defined and voted by Parliament to ensure universal minimum coverage:

-

This contract allows a simplified comparison of prices for the general public:

-

Freedom for operators to offer additional options with reinforced transparency rules and marketing that must be available online.

Future health financing system in France

Author provided (no reuse)

Source: Health Institute

Multiple wins

The financial gains from this new system would be of the order of 20 billion euros reinvested in the health system (prevention, innovations, training). Strengthening solidarity and universal access to health, improving risk coverage, better readability and accountability of stakeholders in financing will be other benefits.

This health financing reform is absolutely major in fixing our system. It is also for the future of our social security and therefore our social protection. Health financing is THE major challenge for developed countries, along with that of the ecological transition, for the next twenty years. The objective is also to make health financing a major lever for wealth creation and social justice, and not a cost center.

Finally, the reform is part of a systemic reform, with known contours, which also includes the transformation of the organization of health actors and that of the governance of the system.