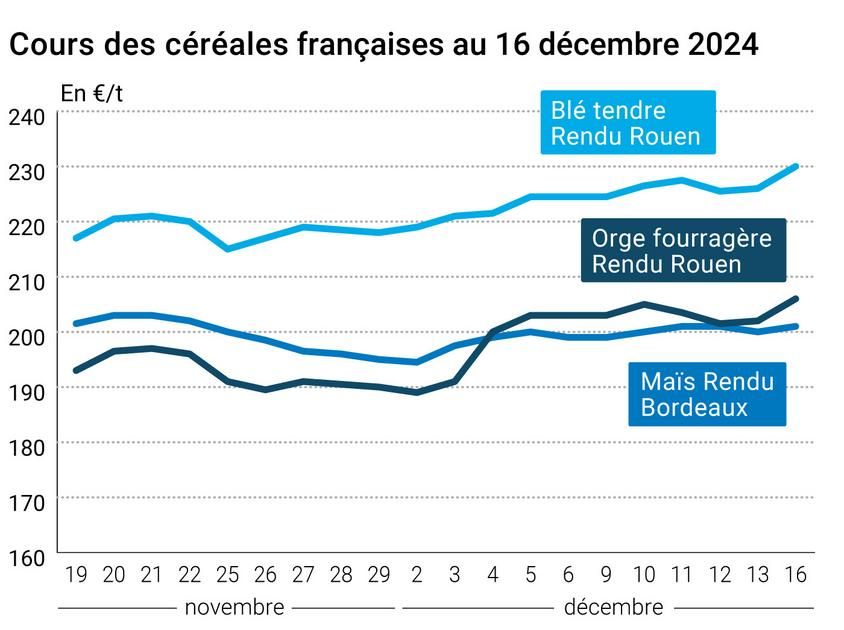

THE prix wheat gained 4 €/t on Euronext between December 13 and 16, supported by a Saudi purchase of 800,000 t for which European origins would potentially have been selected. This important purchase ofSaudi Arabia indirectly supported wheat prices in Minneapolis and Kansas City, while those on the CBOT fell slightly. THE markets French physical stocks followed the Euronext rise in soft wheat and feed barley.

Corn quotations also increased on Euronext and the CBOTbut to a lesser extent, thanks to technical purchases and the attractiveness of the United States origin for export.

To find out everything about agricultural market news, click here

The purchase of the Saudi GFSA shook the markets yesterday, with a volume well above the 595,000 t of wheat initially required in the call for tenders. There Russia should be little present, with Russian prices up $6/t C&F, according to the Ikar firm. Russian exports are also expected to decline in December, according to SovEcon. Uncertainty over Russian export taxes and the imminent implementation of quotas in February have given way to Western European, Romanian, Ukrainian and Argentinian origins, according to the Lachstock Consulting firm. L'North America and theAustralia should be absent. This stimulated price increases in Europe, but also in the United States. Even if this origin should not a priori be accepted, the abundance of contracted volume still had an impact on the prices of winter and spring wheat.

Remember that Russia should suspend its wheat exports to Syriadue to uncertainties over payment for imported volumes. Two ships bound for Syria have been rerouted, Reuters reports. The Ukrainian president announced that his country could take over and supply Syria with grain as part of the Grain from initiative Ukraine.

Algeria has published a call for tenders for durum wheat worth 50,000 t for delivery around March-April.

In butthe market was less turbulent. Good growing conditions in South America continue to weigh on global prices, with rain expected in Argentina and Brazil. In the United States, export figures supported prices.

The AHDB published its supply and demand reports in United Kingdom for the 2024-2025 cereal campaign, marked by the drop in the wheat harvest which fell 21% in volume from one year to the next. Barley and oat production, however, is estimated to increase in 2024. The drop in harvest should ration demand, particularly in milling, and more abundant early season stocks and imports should not be able to avoid the tension on the British market.

To find out everything about the latest news from professionals in the grain sector, click here

Fundamentals:

- United Kingdom, cereals, consumption : 24.18 Mt in 2024-2025, i.e. 2% decrease compared to 2023-2024 (source: AHDB)

- United Kingdom, wheat, imports : 2.75 Mt in 2024-2025, i.e. 13% more than in 2023-2024 (source: AHDB)

- United Kingdom, cereals, end of season stocks : 5.39 Mt, i.e. 14% decrease compared to 2023-2024 (source: AHDB)

Commerce international :

- Saudi Arabia, wheat, purchase : 804,000 t of hard wheat, optional origin, $268.87/t C&F on average, delivery February-April 2025 (source: Reuters)

- Russia, wheat, exports : 3.5 Mt in December compared to 3.7 Mt in December 2023 (source: SovEcon)

- United States, soft wheat, weekly export inspections : 298,075 t the week ending December 12 (source: USDA)

- United States, corn, weekly export inspections : 1,129,834 t the week ending December 12 (source: USDA)

French physical markets from December 16, 2024 (July base for cereals)

| Soft wheat | Specifications | Due date | euro/t | | Variation |

| Dunkirk rendering | 220/11 miller Harvest 2024 | Jan-Mar | 231,00 | N | 4,00 |

| Rendering La Pallice | 76/220/11 Harvest 2024 | Jan-Mar | 231,00 | N | 4,00 |

| Rendering Rouen | 76/220/11 Harvest 2024 | Jan-Mar | 230,00 | N | 4,00 |

| Pontivy/Guingamp rendering | forage 74 kg/hl base, 72 kg/hl mini Harvest 2024 | Dec-Mar | 226,00 | N | 4,00 |

| Fob Moselle | miller Harvest 2024 | Dec-Mar | 236,00 | N | 4,00 |

| Fob Rouen | FCW Superior A2 class 1 major. included Harvest 2024 | dec. | 237,95 | | 3,10 |

| Fob La Pallice | FAW Superior A2 class 1 major. included Harvest 2024 | dec. | 239,15 | | 3,10 |

| Departure from Marne | BPMF 220 Hagberg Harvest 2024 | Jan-Mar | 231,00 | N | 4,00 |

| Departure from Eure/Eure-et-Loir | BPMF 76 kg/hl Harvest 2024 | Jan-Mar | 225,00 | N | 4,00 |

| Departure South-East | miller Harvest 2024 | Jan-Mar | 240,00 | N | 5,00 |

| Durum wheat | Specifications | Due date | euro/t | | Variation |

| Rendering Port-la-Nouvelle | semolina standards Harvest 2024 | Dec-Mar | 295,00 | N | 0,00 |

| Departure from Eure/Eure-et-Loir | semolina standards Harvest 2024 | Dec-Mar | 285,00 | N | 0,00 |

| Departure South-East | semolina standards Harvest 2024 | Dec-Mar | 285,00 | N | 0,00 |

| But | Specifications | Due date | euro/t | | Variation |

| Bordeaux rendering | Harvest 2024 | Dec-Mar | 201,00 | N | 1,00 |

| Rendering La Pallice | Harvest 2024 | Jan-Mar | 201,00 | N | 1,00 |

| Pontivy/Guingamp rendering | Harvest 2024 | Dec-Mar | 207,00 | N | 1,00 |

| Fob Bordeaux | Harvest 2024 | Dec-Mar | 205,00 | N | 1,00 |

| Fob Rhin | Harvest 2024 | dec. | n.p. | | |

| | Harvest 2024 | Dec-June | 219,00 | N | 1,00 |

| Departure South-East | Harvest 2024 | Dec-Mar | 210,00 | N | 1,00 |

| Feed barley | Specifications | Due date | euro/t | | Variation |

| Rendering Rouen | 62-63 kg/hl Harvest 2024 | Jan-Mar | 206,00 | N | 4,00 |

| Pontivy/Guingamp rendering | Harvest 2024 | Dec-Mar | 209,00 | N | 4,00 |

| Fob Moselle | without limit. orgettes Harvest 2024 | Jan-Mar | 197,50 | N | 4,00 |

| Departure from Eure/Eure-et-Loir | Harvest 2024 | Jan-Mar | 196,00 | N | 4,00 |

| Departure South-East | 62/63 kg/hl Harvest 2024 | Jan-Mar | 215,00 | N | 1,50 |

| Malting barley – Winter 6 rows | Specifications | Due date | euro/t | | Variation |

| Fob Creil | Faro 11.5% max Port 500 t Harvest 2024 | Jan-June | 222,00 | N | 0,00 |

| Malting barley – Spring | Specifications | Due date | euro/t | | Variation |

| Fob Creil | Planet 11.5% max Port 500 t Harvest 2024 | Jan-June | 238,00 | N | 0,00 |

Quotations of milling products from December 10, 2024

| Its fine soft wheat | Specifications | Due date | euro/t | | Variation |

| Departure from Ile-de-France | | available. | 139,00-141,00 | T | |

| | pellets | available. | 151,00-153,00 | T | |

| Half-white remolding | Specifications | Due date | euro/t | | Variation |

| Departure from Ile-de-France | | available. | 169,00-171,00 | T | |

| Low flour | Specifications | Due date | euro/t | | Variation |

| Departure from Ile-de-France | | available. | 169,00-171,00 | T | |

Commercial quotes for dairy products from December 12, 2024

| Milk powder | Specifications | Due date | euro/t | | Variation |

| | NBPL departure at 30 days 5% H BT bulk | available. | 2520,00 | T | |

| Whey powder | Specifications | Due date | euro/t | | Variation |

| | NBPL departure at 30 days, BILA pH 6 bulk | available. | 865,00 | T | |

Dollar/euro evolution of December 16, 2024

| Devise | Closing value |

| 1 dollar US | 0,9526 euro |

| 1 euro | 1,0498 dollar |

Chicago Futures Market Closes December 16, 2024

| Raw materials | Fence | Chicago |

| Wheat | 550,00 | cents/wood. |

| But | 445,00 | cents/wood. |

| Ethanol | 2,161 | $/gallon |

Closing of the Euronext futures market on December 16, 2024

| Milling wheat (Euronext) |

| Echéance | Fence |

| Mars 2025 | 233,50 |

| May 2025 | 236,75 |

| Sept. 2025 | 225,25 |

| Volume | 88785 |

| Corn (Euronext) |

| Echéance | Fence |

| Mars 2025 | 208,00 |

| June 2025 | 215,00 |

| August 2025 | 219,00 |

| Volume | 3340 |

International market quotes from December 16, 2024

| Energy | Echéance | Closing value |

| Oil (Nymex) | Jan. 2025 | 70,71 $ |

| Ocean freight indices | from December 16 | Variation |

| Baltic Dry Index (BDI) | 1071 | 20,00 |

| Baltic Panamax Index (BPI) | 977 | -18,00 |

| Baltic Capesize Index (BCI) | 1340 | 77,00 |

| Baltic Supramax Index (BSI) | 955 | -4,00 |

| Baltic Handysize Index (BHSI) | 608 | -10,00 |