In 2023, the 100 largest global arms companies will reach a total of $632 billion, according to the latest Sipri report. In the top 10, five American companies, three Chinese, one British, one from Russia.

If you want peace, prepare for war (“And you want peace, prepare for war”, in French). The Latin expression has never been so true as noted by the Stockholm International Peace Research Institute (Sipri) in its latest report on the sales of the main arms suppliers In 2023, the top 100 arms and military sales companies made a total of $632 billion, an increase of 4.2% compared to 2022.

“Arms sector revenues increased in all regions, with particularly strong increases among companies based in Russia and the Middle East,” Sipri said.

Small producers

In 2022, sales were down due to the production capacities of large companies in the sector. Industry giants have adapted to the situation. But also, “small producers have been more effective in meeting new demand linked to the wars in Gaza and Ukraine, growing tensions in East Asia and rearmament programs in other regions.”

In this report, Sipri notes, for example, that all the companies in the ranking achieved a turnover of more than one billion dollars last year. Nearly three-quarters of companies increased their turnover.

“This trend is expected to continue in 2024,” said Lorenzo Scarazzato, a researcher at Sipri’s military spending and arms production program.

This forecast is based in particular on recruitment campaigns. For Lorenzo Scarazzato, this “suggests that they are optimistic about future sales.”

Rostec, biggest increase in the Top 10

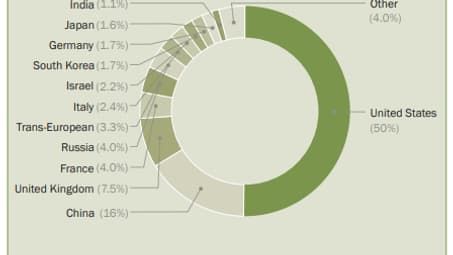

With 41 companies ranked in this top 100 (of which 5 occupy the first places), the United States largely dominates this industry. In the lead, Lockheed Martin and RTX (formerly Raytheon Technologies) which despite everything showed respective declines of 1.6% and 1.3%.

Emmanuel Chiva, general delegate for armaments (DGA) – 06/05

“These large companies often rely on complex, multi-tiered supply chains, which has made them vulnerable to continued supply chain challenges in 2023,” says Dr. Nan Tian, Director of the Military Spending Program and SIPRI arms production.

“This was particularly the case in the aeronautics and missile sectors.”

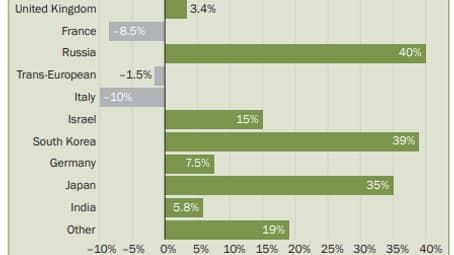

Along with the Americans, the Chinese, the British and the Russians are in the top 10 places. The largest increase in this group is achieved by the Russian Rostec which increased by 49.3% in just one year.

Europe lagging behind?

In this sector, the Europeans are clearly lagging behind. The combined revenues of the 27 largest companies (excluding Russia) totaled $133 billion in 2023, 0.2% more than in 2022.

“This is the lowest increase in all regions of the world,” notes Sipri, qualifying this result.

European arms companies producing complex weapons systems mainly worked on older contracts in 2023 and their revenues for the year therefore do not reflect the influx of orders.

“Complex weapon systems have longer production times, so the companies that produce them are inherently slower to react to changes in demand,” explains Lorenzo Scarazzato.

Among the 27 European companies, five are French: Thales (16th), Naval Group (32nd), Safran (33rd), Dassault Aviation (46th) and the CEA (50th).

Wars in Ukraine and the Middle East

Two other strong trends appear in this report. South Korean and Japanese companies lead revenue growth in Asia and Oceania.

The four South Korea-based companies recorded a combined 39% increase in arms revenue to $11.0 billion. The five Japanese companies saw their combined arms revenue increase 35% to $10.0 billion.

Furthermore, arms producers in the Middle East are seeing their turnover increase due to the conflicts in Gaza and Ukraine. Six of the 100 largest arms companies were based in the Middle East. Their combined revenues increased 18% to $19.6 billion.

“With the outbreak of the war in Gaza, the revenues of the three Israeli-based companies in the Top 100 reached $13.6 billion. This is the highest figure ever recorded by Israeli companies in the Top 100 of the Sipri.”

In Turkey, the three companies saw their revenues increase 24% to $6.0 billion, “thanks to exports boosted by the war in Ukraine and the Turkish government’s continued drive to become self-sufficient in production of weapons.”