When Ottawa announced last week the distribution of $250 checks to workers (a measure put on hold), the discontent of retirees was quick. The discourse according to which seniors are struggling to make ends meet and that they are more affected by inflation than other cohorts has been heard repeatedly in the public space.

Posted at 6:30 a.m.

It’s quite curious, because in June, Duty had published a major file on the “largest intergenerational wealth transfer in history” 1. All the statistics and studies cited showed that seniors who will die in the coming years will leave inheritances larger than ever.

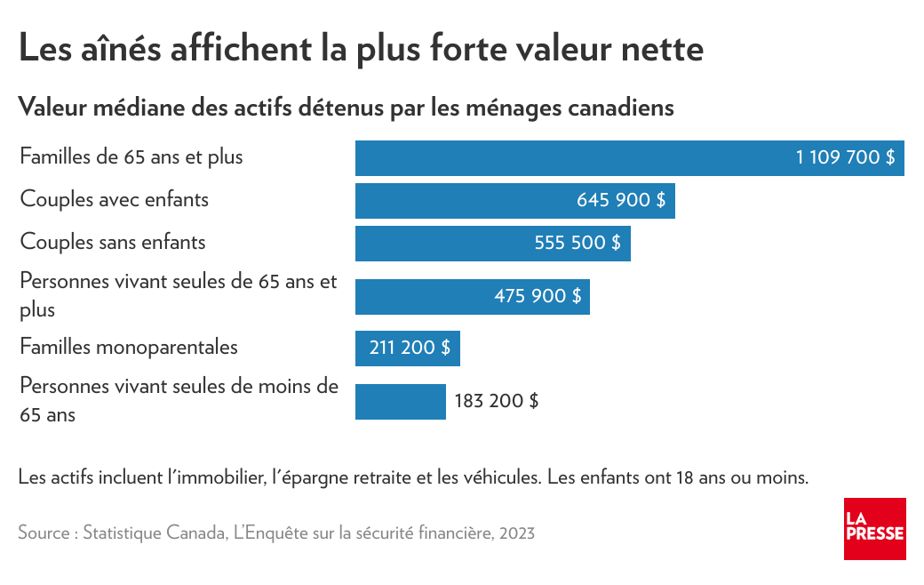

Chartered Professional Accountants (CPAs) took the trouble to quantify the “astronomical sums” that Canada’s baby boomers will leave: $1 trillion2. This is not surprising when we know that the median value of families made up of people aged 65 and over exceeds $1.1 million, which includes real estate, vehicles, savings and the value of retirement plans. retirement.

No other cohort has such high assets, according to Statistics Canada. This makes sense, when you think about it, since it takes time to accumulate wealth and benefit from the magic of compound interest.

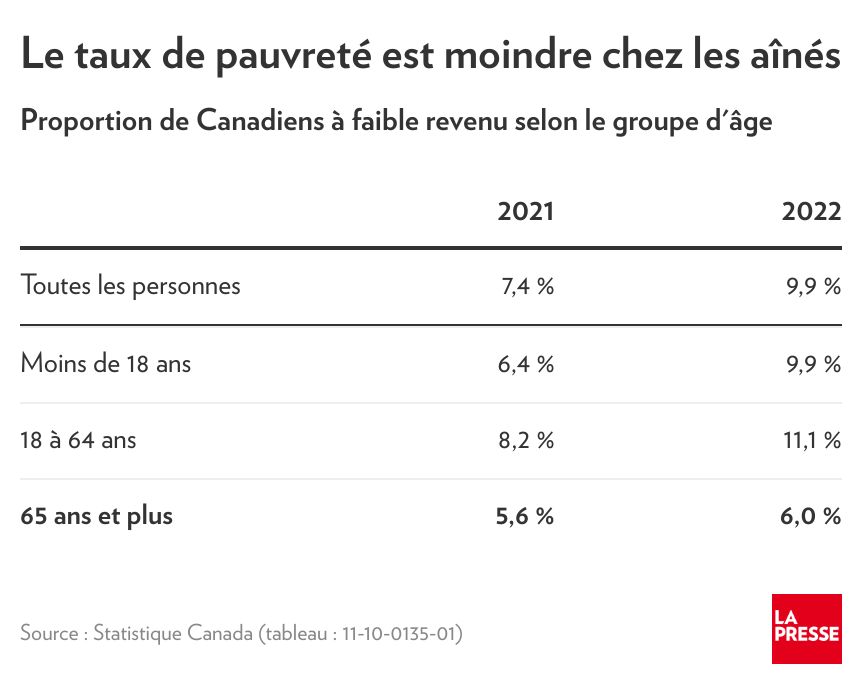

We can also analyze the situation by looking at the poverty rate by age group. But again, seniors stand out… due to their enviable situation.

The proportion living below the poverty line is lower (6%) than among other adults (11.1%). This is without taking into account that the financial situation of those aged 65 and over changed little between 2021 and 2022 while the inflationary surge was rampant. The same cannot be said among the youngest, as we see in the table below.

It makes sense, when you think about it. The annuities paid by Quebec and Ottawa are not fixed. On the contrary, they are fully indexed to the cost of living. On the other hand, not all workers have had the chance to see their wages jump at the same rate as inflation. In addition, seniors have taken greater advantage of the rise in interest rates to enrich themselves since their bank accounts are larger. Their CPGs have returned well.

However, listening to the president of the Fédération de l’Âge d’Or du Québec (FADOQ), Gisèle Tassé-Goodman, at the microphone of Nathalie Normandeau and Luc Ferrandez3we have the impression that many seniors live in precarious conditions due to inflation and that those who have the means to travel are the exception. “Incomes are fixed for people who receive government benefits. The cost of groceries, consumer goods, transportation, rent, has increased enormously. We need to help these people. »

The speech of the Quebec Association for the Defense of the Rights of Retired and Pre-retired Persons (AQDR) is similar. “The people who have been most affected by the increase in the cost of living, proportionally, are seniors, particularly the most vulnerable seniors, people who only live on federal income,” said Pierre Lynch. , president of the AQDR, to my colleague Karim Benssaiseh4. The NDP and Bloc Québécois made similar comments, demanding that seniors also be entitled to $250 in April.

Since numbers can be misleading or misinterpreted, I contacted a retirement income expert. Pierre-Carl Michaud is a professor in the applied economics department at HEC Montréal and scientific director of the Institute on Retirement and Savings. He agrees that the message about seniors is not always consistent with today’s reality. Until the middle of the last century, retirees were struggling financially and this perception remains embedded.

“In almost all OECD countries, we have this problem of myth which is very difficult to undo,” he told me. We may be sensitive to the image of the single elderly person, who has almost no retirement income, who lives in difficulty… There are some, in Canada, but the average elderly person lives with the power to substantial purchase. »

Certain public policies that are costly for the State are also based on this myth of miserable seniors and everyone pays the price in the end. “We have to get rid of it,” argues the academic who is not insensitive to the plight of seniors despite the figures on them that he has been studying for years.

Its calculations also highlight a little-known phenomenon: retirees whose after-tax income is higher at age 65 than before age 65. On average, in Quebec, 66 to 69 year olds earn the equivalent of 90% of their work income5. For half of the population, this replacement rate is 100% and it rises to 300% among the poorest.

Yes, retirement in many cases results in an increase in income.

Are seniors more affected by inflation because the composition of their shopping basket differs considerably from that of younger people, as we sometimes hear? The data, replies Pierre-Carl Michaud, instead demonstrate that their expenses “are quite close to the Canadian average”.

Of course, whether we’re talking about average or median, there are always people at the ends of the spectrum. Moreover, one in five seniors lives on 60% of their pre-retirement income, a replacement rate considered “relatively low”. Their personal reality exists and the idea here is not to deny it. On the contrary, we must ensure that targeted measures are put in place to improve their situation, which the original idea of $250 checks unfortunately did not do at all. The second version, if applicable6, should be more sensible.

1. Read the file of Duty

2. View CPA analysis

3. Listen to the intervention of the president of FADOQ

4. Read the article on the position of the AQDR

5. Consult the calculations of Professor Pierre-Carl Michaud

6. Read the article “Government removes $250 check from bill, but won’t abandon it”