Peter Schiff’s recent interview on Kitco is among his most virulent interventions. The famous economist openly criticizes the situation in the United States, alerting to an imminent dollar crisis, a fall in purchasing power, and a brutal reversal of world capital flows.

According to Schiff, we are witnessing the gradual collapse of the American economic model based on credit consumption and external financing. The United States has experienced above its means for decades, taking advantage of foreign investments and their reserve currency status. But this system vacillates: the dollar, treasury bills and American actions fall in parallel, a sign that the classic refuge dynamics (“Flight to Safety”) is broken.

The analyst anticipates stagflation in the United States, much brighter than that of the 1970s: a prolonged recession coupled with sustainably high inflation. Such a shock could erode confidence in American debt, forcing investors from around the world to turn away from the assets denominated in dollars. A “liberation” according to him, which would open a new period of global growth-outside the United States.

Is this observation exaggerated? Are the United States really on the verge of a severe recession?

The latest American foreign trade data in any case gives reflection material. last week, maritime imports from China dropped by 64% in a week. More broadly, trade in the United States-imports and exports-collapsed in a few days.

Although this may partly be explained by an anticipation effect – companies that have massively stored before the entry into force of new customs tariffs – the signal is still worrying. These data evoke, by their brutality, the logistical shock caused by the COVID crisis on international trade.

Such a slowdown could mark the beginning of a broader contraction of global demand, strengthening the idea of a cyclical reversal to the United States.

This scenario is also reinforced by an advanced key indicator: the US State Manufacturing 6-Month Ahead New Orders. This index, which measures the anticipations of new orders in the manufacturing industry, provides for an unprecedented fall within six months – even worse than during the 2008 or COVIR crisis.

The survey, carried out with purchasing directors at the national level, reaches a unprecedented level of pessimism since the creation of this indicator. The American industrialists themselves are preparing for a violent stroke of the demand.

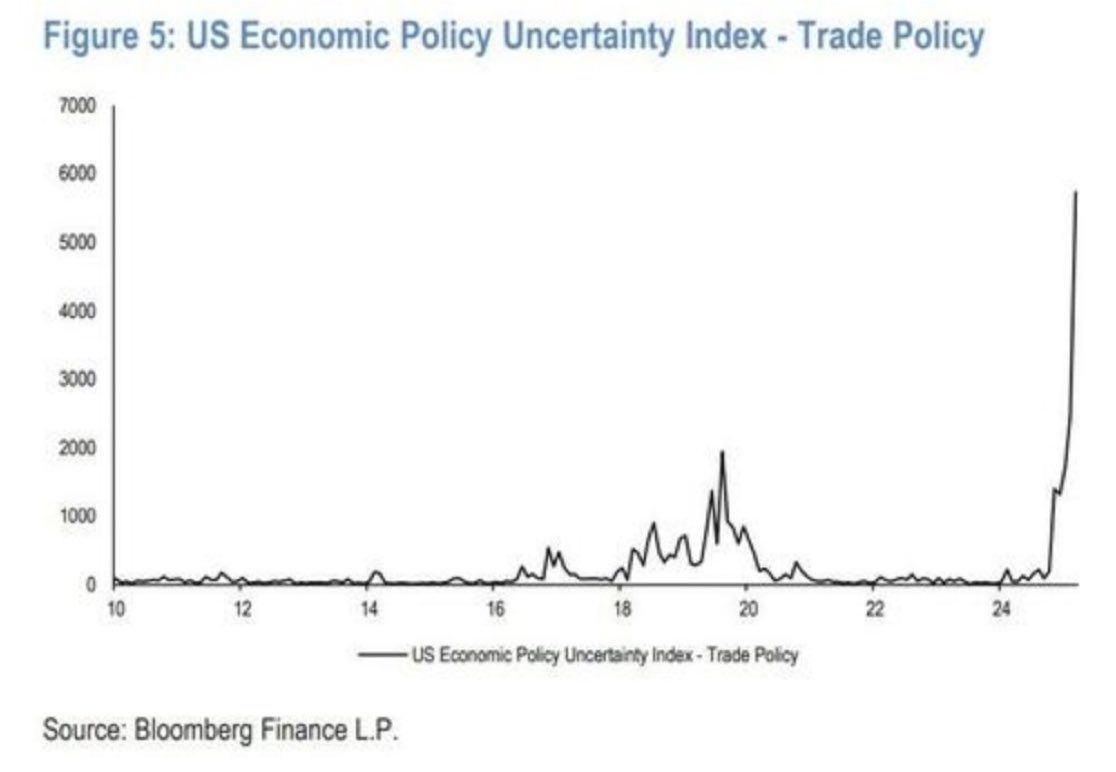

The anticipation of a collapse of demand is part of an economic context marked by an increasing uncertainty. Rarely the American economy has evolved in such an opaque environment. The administration in place sends contradictory signals and makes decided decisions, contributing to a climate of generalized instability. In the short term, this political and regulatory uncertainty erodes the confidence of economic actors and slows down investment decisions. The chaos generated by prices increases and geopolitical tensions causes a generalized wait -and -see effect.

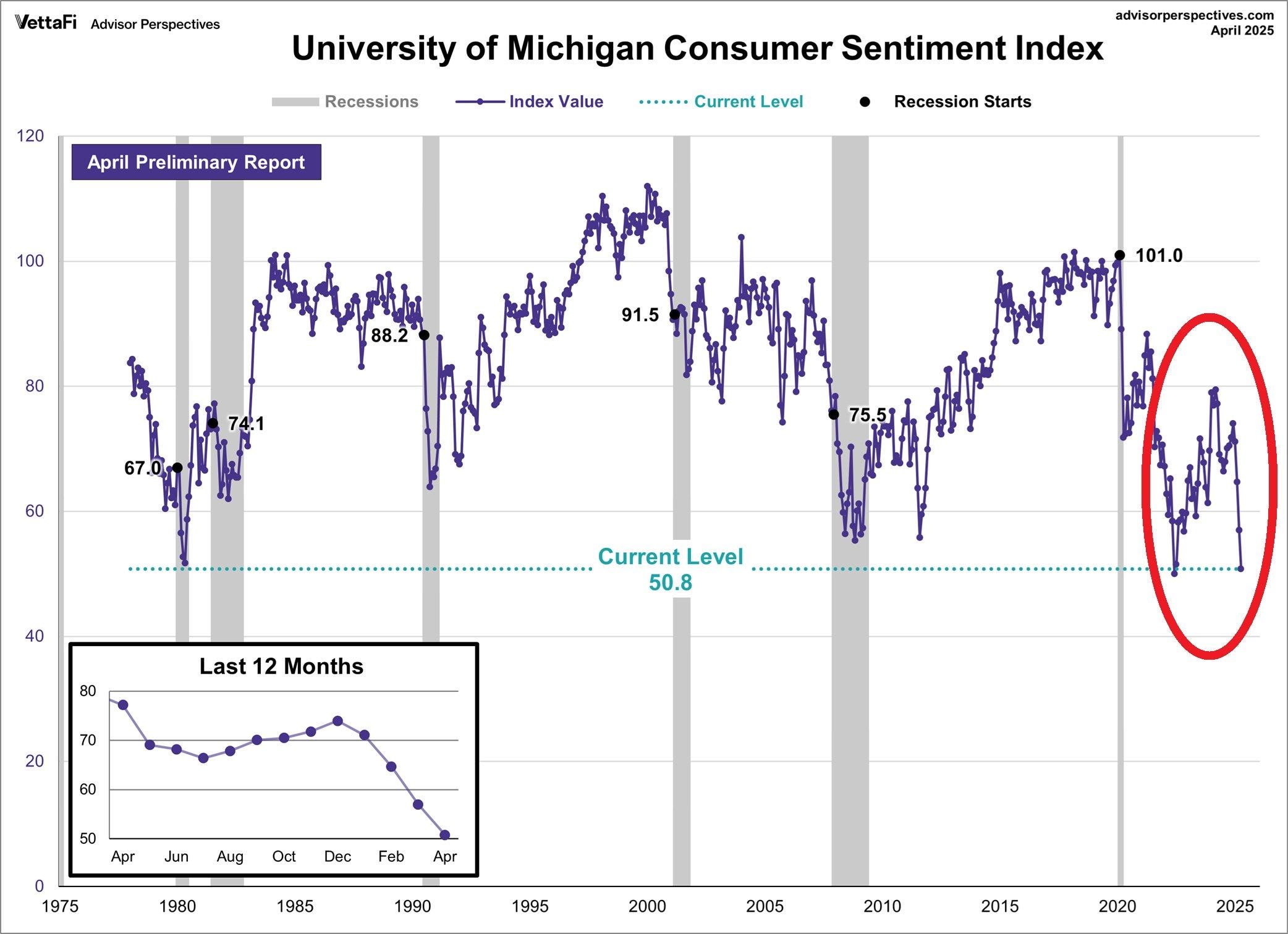

This ambient instability also weighs on consumer morale, whose confidence has just dived at historically low levels. Since the great financial crisis or the shock of the covid, the feeling of households had never been so shaken, revealing a deep concern in the face of the economic future of the country.

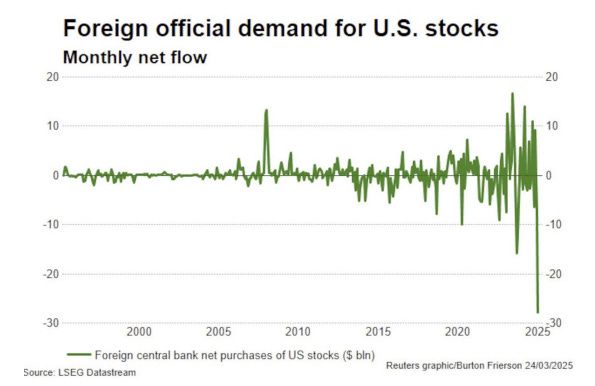

The threat of a clear slowdown in American consumption leads to a massive disengagement of foreign investors. Worried about the prospect of a recession, the latter turn away from the assets denominated in dollars, triggering an unprecedented wave of sales. Obligations, shares, and even treasury bills are liquidated on a large scale-a strong signal of loss of confidence in the economic resilience of the United States.

This rush outside the United States is accompanied by intense pressure on the dollar. The index Dxy, which measures the value of the greenback in the face of a basket of major currencies, has just crossed the symbolic threshold of the 100 – a clear signal of the loss of market confidence in the American currency. This drop is part of a generalized disengagement movement with regard to assets denominated in dollars, against a background of a more and more imminent recession.

-

Gold is the big winner of this movement.

Peter Schiff underlines that central banks massively buy gold, replacing the dollar. According to him, they anticipate a new monetary system where gold would restore the main world value reserve. He estimates that the golden price could reach $ 5,000 to $ 20,000 in the coming years – not because gold is appreciated, but because the dollar loses its purchasing power.

Last February, net purchases of gold by central banks reached 24 tonnes – a record since November 2024. This is the 20th month of net purchases out of the last 21, according to data from the World Gold Council.

This also marks the prospect of a 16th consecutive year of strengthening official reserves. In three years, central banks have accumulated 3,176 tonnes of gold.

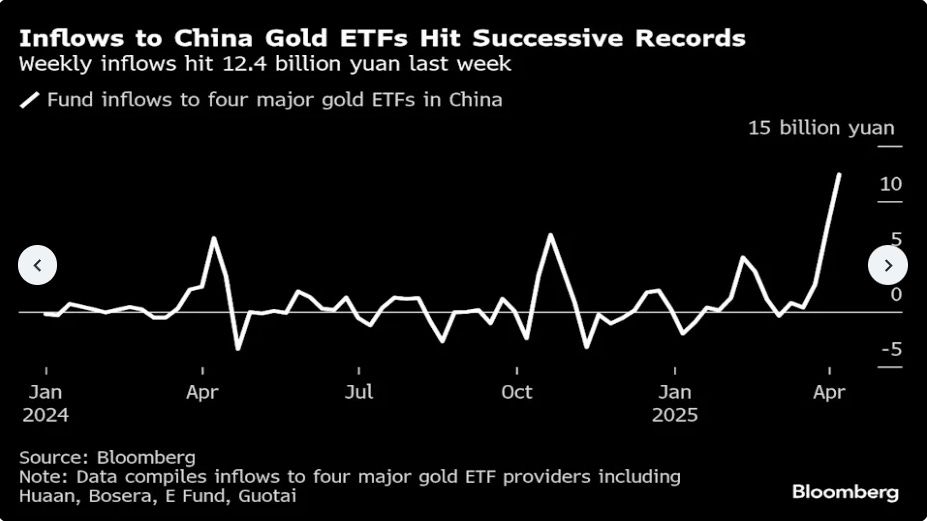

Central banks are not the only ones to buy gold: the outbreak of prices has triggered a new rush on metal in China. Investors, financial institutions, refineries and individuals turn massively to gold, whether via investment ingots, accumulation plans offered by banks, or ETFs. This renewed interest is explained by loss of confidence in dollar assets and growing uncertainty linked to persistent trade tensions between Beijing and Washington. Result: gold imposes itself as a refuge value, strategic and durable, far beyond the simple speculative bet.

Record flows to ETF backed by yellow metal pushed the premium local on gold at $ 20 per ounce. At the same time, volumes of term contracts on gold negotiated on the Shanghai Stock Exchange jumped, reaching their highest level in one year.

The gold rush in China takes place in a total indifference of the general American public, still focused on loss of speed. While the dollar is quickly depreciated, symbol of a global recoil of confidence, the investor retail American remains paralyzed, without enjoying the spectacular increase in gold.

This discrepancy illustrates a deep asymmetry of anticipations between the east and the west. In China, gold has already become a strategic pillar, adopted both by households, central banks and institutional banks. Meanwhile, in the West, investors, still distracted by other economic narratives, let a historic opportunity pass.

In his interview, Peter Schiff also underlines that the actions of gold mining companies are historically undervalued, due to the disinterest of private investors for gold, who have turned to Bitcoin. According to him, the mining today offers a potential of increase higher than that of physical gold, in particular due to increased margins, favored by a relatively low energy cost and a high sale price of yellow metal.

If his forecasts prove to be correct, we could attend in the coming weeks a profound change in behavior on the financial markets. On the one hand, traditional actions are likely to be sold with each rebound (“SELL The RIP”), because investors will begin to anticipate a severe recession, sustainably high interest rates and a structural weakening of the dollar. On the other hand, mining values, in particular gold producers, could, on the contrary, benefit from a renewed interest: each withdrawal will then become an opportunity to buy (“buy the dip”).

This movement would be explained by the return to grace of gold as a refuge value, but especially by the growing attraction for tangible assets capable of generating cash in an inflationary environment. The mining, long neglected, combine operational lever effect, low valuation and direct exposure to the increase in precious metals. If the scenario envisaged by Schiff materializes, investors could carry out a rapid and massive reallocation of their capital towards the mining sector, still largely undervalued. After missing the prices of physical gold, they will seek not to let the opportunity pass on mining actions.

Reproduction, integral or partial, is authorized provided that it contains all hypertext links and a link to the original source.

The information contained in this article has a purely informative nature and in no way constitute an investment council or a recommendation for purchase or sale.

--

{kind=link}