Find the latest news and trends in commodity prices around the world every month thanks to the analysis of our sectoral economists. This month, focus on cocoa, the price of which per tonne has reached its highest level in 6 months, exceeding 10,000 USD/tonne. An increase of 50% compared to the previous month!

- In December 2024, cocoa prices increased by 50% compared to the previous month.

- The price of a tonne of cocoa beans reached its highest level in 6 months, exceeding 10,000 USD/tonne.

A very concentrated supply and an increasing demand

Four countries represent 75% of global production, mainly in West Africa. More particularly, Ivory Coast and Ghana, which represent 58% of this production, have recently suffered from unfavorable weather conditions leading to a drop in production not covered by other producing countries. Global cocoa production is expected to reach 5 million tonnes in 2024/2025.

At the same time, global demand continues to increase, particularly in Europe and North America which consume nearly 50% of the world's cocoa. Consumption is also growing in emerging markets – Asia, Middle East, South America – despite rising prices. During the 2023/24 campaign, the supply deficit represented more than 400,000 tonnes. Deficit which could continue to widen in 2025.

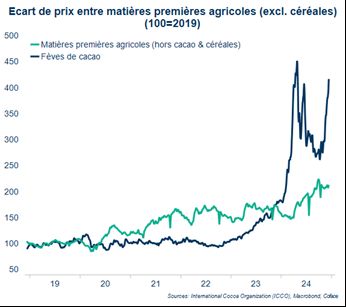

Price gap between agricultural raw materials

The data corresponding to this graph is available in the following table

Industry concentration fuels inflationary pressures

The cocoa processing industry is dominated by Europe, particularly Germany and the Netherlands. Four companies thus control two-thirds of the world's crushing capacity, and the same is true in the retail confectionery market. This concentration makes it difficult for new players to enter in the face of the sector's behemoths and reinforces the North-South gap in the value chain.

Cocoa prices are experiencing a new surge after several months of decline on the markets. This increase, which originates from structural imbalances between supply and demand, is accentuated during this holiday season with increasing demand to honor existing contracts.

Simon Lacoume, sector analyst at Coface.

A rise in prices sustained by supply deficits

Production deficits in Ivory Coast and Ghana, combined with growing demand to honor existing contracts, accentuate the rise in prices. The structural imbalance between supply and demand suggests, in the medium term, that cocoa prices will stabilize at an equilibrium price significantly higher than in previous years, and most likely close to 10,000 USD/tonne. Prolonged supply tensions could also seriously affect large chocolate manufacturers, who remain dependent on a few supplier countries. Industry consolidation has led to the formation of processing giants, whose investments are only profitable when production capacity is fully utilized. Although a shortage of raw materials is considered a low probability risk, its potential impact on the industry could be profound.