How can we not discuss Snowflake* at the end of the year? The company operating in the field of data and artificial intelligence is not benefiting from the enthusiasm encountered by investors for this theme over the past two years.

However, the company offers a complete and very useful platform for its customers, the AI Data Cloud, which allows companies to centralize their data, extract useful information from it, apply AI to solve problems, and create apps. data and share it all easily. Their business model is consumption-based, meaning the more data customers use and store, the more money Snowflake makes. Their cloud-native architecture is divided into three layers: compute, storage, and cloud services, each independently scalable but logically integrated.

However, in 2024, Snowflake has struggled to keep up with the frenetic pace of the AI revolution. They had to invest massively, sacrificing their margins to obtain more computing capacity. This shift was crucial to innovate and reinvent their offerings. One of the flagship products of this transformation is Iceberg Tables, which has attracted criticism but is seen by management as an opportunity to expand their market.

Recent results show a certain duality: cautious optimism in the face of the challenges of transition. Snowflake exceeded product revenue forecasts, reaching $900 million, and operating margins doubled. The forecast for the fourth quarter is also positive. These results are the result of rigorous cost management and product innovations.

Sridhar Ramaswamy, the new CEO, has been a driving force behind this change, emphasizing long-term innovation rather than immediate revenue optimization. This has led to trade-offs, such as short-term cash flow constraints, but paves the way for sustainable growth.

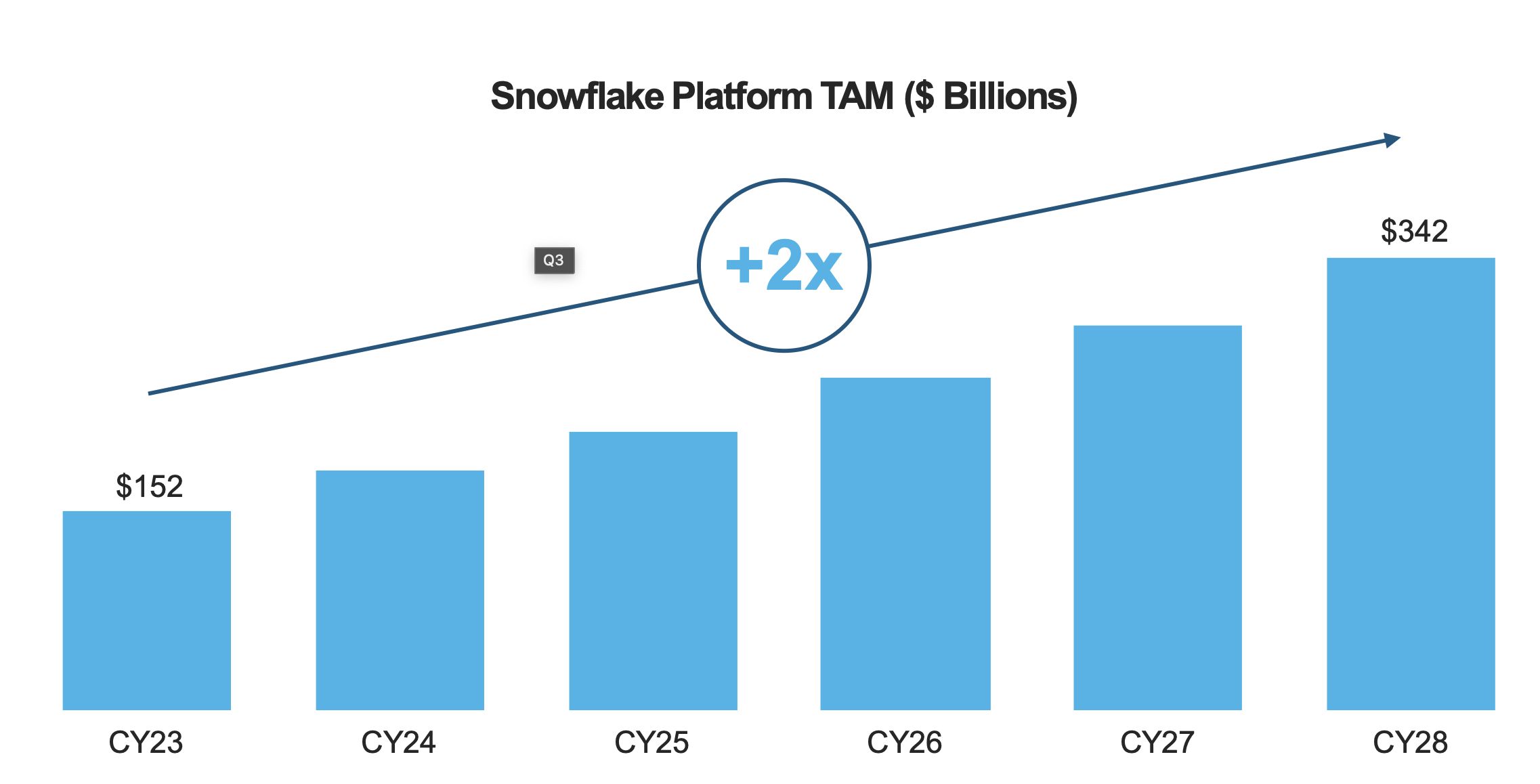

The company remains competitive despite competition from Databricks and a recent security breach. Looking ahead, 2025 could be a turning point. With investments in AI accelerating, Snowflake is well positioned to provide the necessary infrastructure. Backlog growth and AI-related revenues are expected to drive revenue expansion and margin improvement in the years to come.

Their solutions simplify the complexity of fragmented systems that many businesses face. Their unified platform facilitates the transition from data collection to advanced AI applications. With products like Snowflake Copilot and a secure cross-cloud architecture, they deliver on their promise of simplification without sacrificing power.

Despite these positives, Snowflake's stock is down about 16% in 2024, in part due to competition with Databricks and disappointing revenue forecasts. The stock, which peaked at $400 at the end of 2021, is now trading around $166. The question is whether it can go back to $400.

For this to happen, Snowflake will need to continue to innovate, expand its market, and improve its margins. Strategic partnerships, like that with Nvidia and Anthropic, and the expansion of AI-related products are key. However, investors must be patient and willing to accept the risks associated with this transition.

Investing in Snowflake now may be an opportunity for those who believe in its long-term potential. However, for the more cautious, waiting for clearer signs of profitability and growth might be wiser. In fact, the company is not profitable and is not expected to be for several years. Snowflake has the assets to bounce back, but the path to $400 will require continued time and effort.

*that means “snowflake” for those who hadn't made the connection.