Bond yields rose overall in October as improving labor market data led to questions about the trajectory of future rate cuts from the Federal Reserve.

Bond markets generally fell in October, driven by improved data on the US labor market and uncertainty surrounding the US presidential election. US Treasury yields continued to rise as strong non-farm payrolls numbers led markets to revise their expectations for a rate cut from the Federal Reserve (Fed). The US dollar continued to strengthen, reaching its highest levels since July.

In the euro zone, economic growth exceeded expectations in the third quarter, with an increase of 0.4%. Spain was a major player, while Germany also recorded surprise growth of 0.2%, avoiding a technical recession. In the United Kingdom, Finance Minister Rachel Reeves announced the autumn budget, causing some volatility in the gilt market while investors digest the investment and recovery plans.

Inflation in developed markets has generally slowed. In the United States, headline inflation fell slightly to 2.5%, while core inflation, which excludes volatile prices for food, energy, alcohol and tobacco, increased. increased to 3.3%. In the UK, headline inflation fell to 1.7% – below the Bank of England’s target for the first time in more than three years – while core inflation fell to 3 .2%. In Europe, headline inflation rose more than expected to 2%, while core inflation remained stable at 2.7%.

The European Central Bank cut interest rates by another 25 basis points in October, continuing to emphasize the importance it places on economic figures. President Christine Lagarde stressed that inflation was likely to rise a little before falling again, due to base effects.

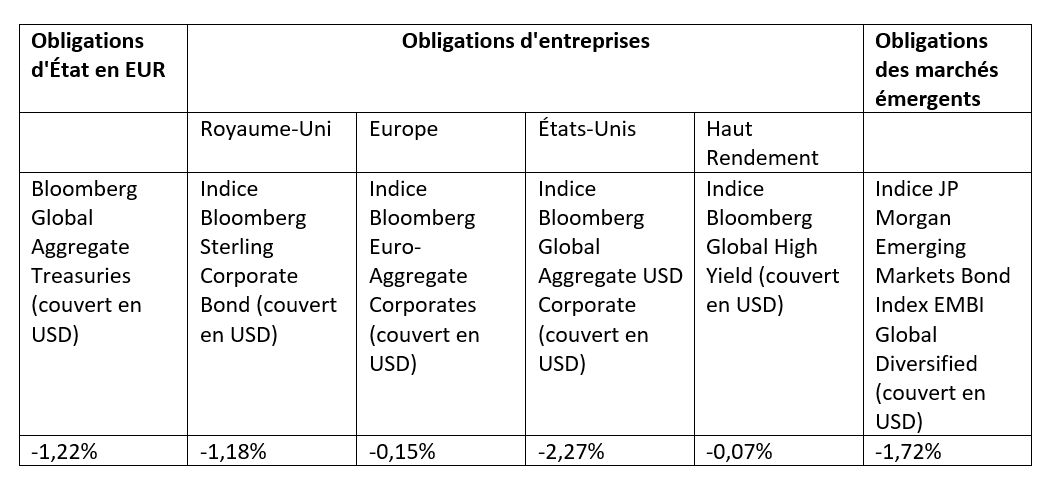

Monthly performance by market

Source: Bloomberg, data for the period September 30, 2024 to October 31, 2024. Bloomberg indices are used as indicators of each exposure.

Obligations d’Etat

Government bond yields rose broadly in October, driven by improving U.S. inflation and labor market data, as well as volatility related to the U.S. election. In the United States, 2- and 10-year yields increased by 53 and 50 basis points respectively. In the Eurozone, two-year German Bund yields rose 21 basis points, while 10-year yields rose 27 basis points. In the UK, yields on two- and ten-year bonds increased by 46 and 44 basis points, respectively.

Credit markets

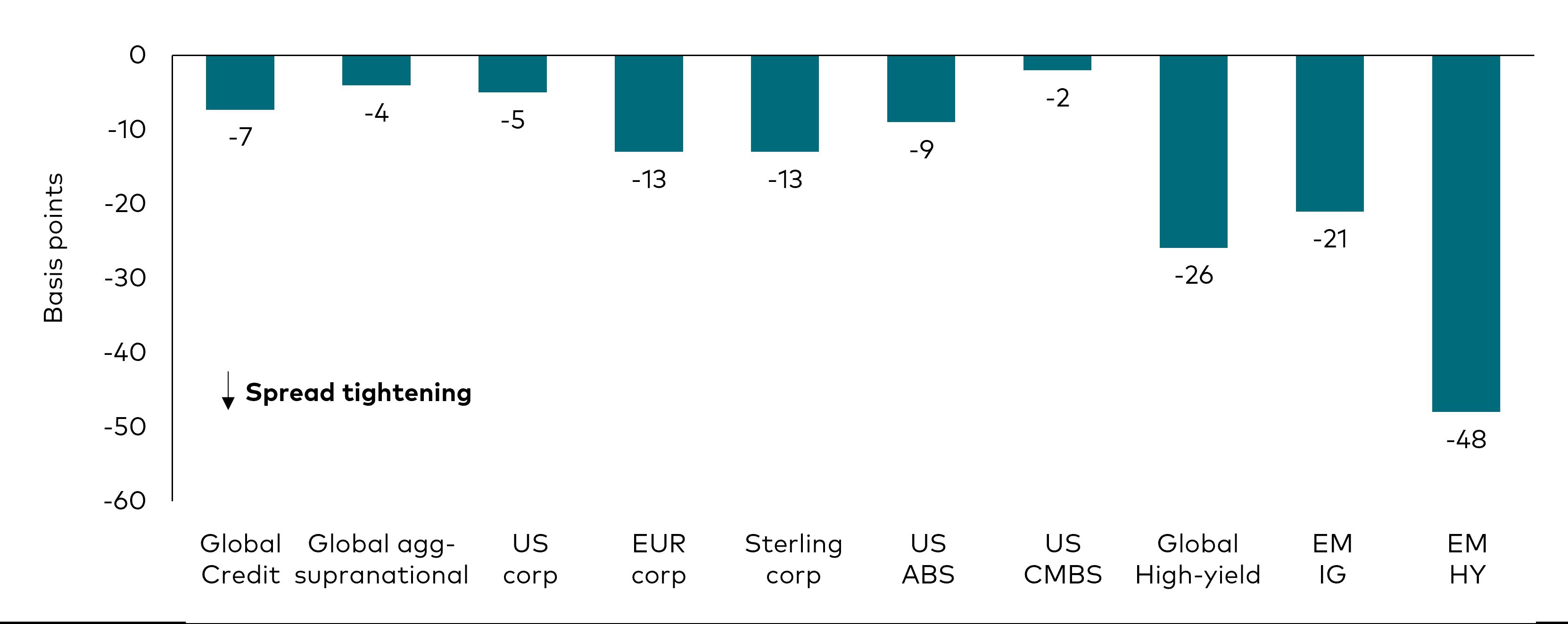

Overall, IG bond spreads tightened during the month. IG bond spreads in the United States, euros and sterling contracted by 5, 13 and 13 basis points respectively. The tightening of spreads was more pronounced in emerging markets (EM), with investment-grade and high-yield spreads contracting by 21 and 48 basis points during the month.

Evolution des spreads

Source: Bloomberg, data for the period September 30, 2024 to October 31, 2024. Indicators used for each exposure.

The third quarter corporate earnings season is in full swing. So far, we have not had any major negative surprises, apart from the weak points already known. The consumer discretionary sector continued to report subdued demand in key markets such as China and, to a lesser extent, Europe and the United States. The automotive sector also continues to experience difficulties.

Our baseline assumption remains that revenue and earnings growth will improve in coming quarters. Indeed, the cycle of falling interest rates strengthens consumer confidence and stimulates economic activity. Geopolitical tensions, however, pose a risk to the recovery scenario by 2025. Another risk is the potential re-emergence of inflationary pressures if a sharp increase in global freight prices were to be reflected in commodity prices. Overall, we remain of the view that the fundamentals of IG companies are in good shape thanks to the general deleveraging observed over the last few years.

The technical outlook remains positive. Since the start of the year, we have observed regular flows towards IG credit. With central banks now on a downward path and credit yields remaining at attractive levels, we believe credit demand will remain strong.

Emerging markets

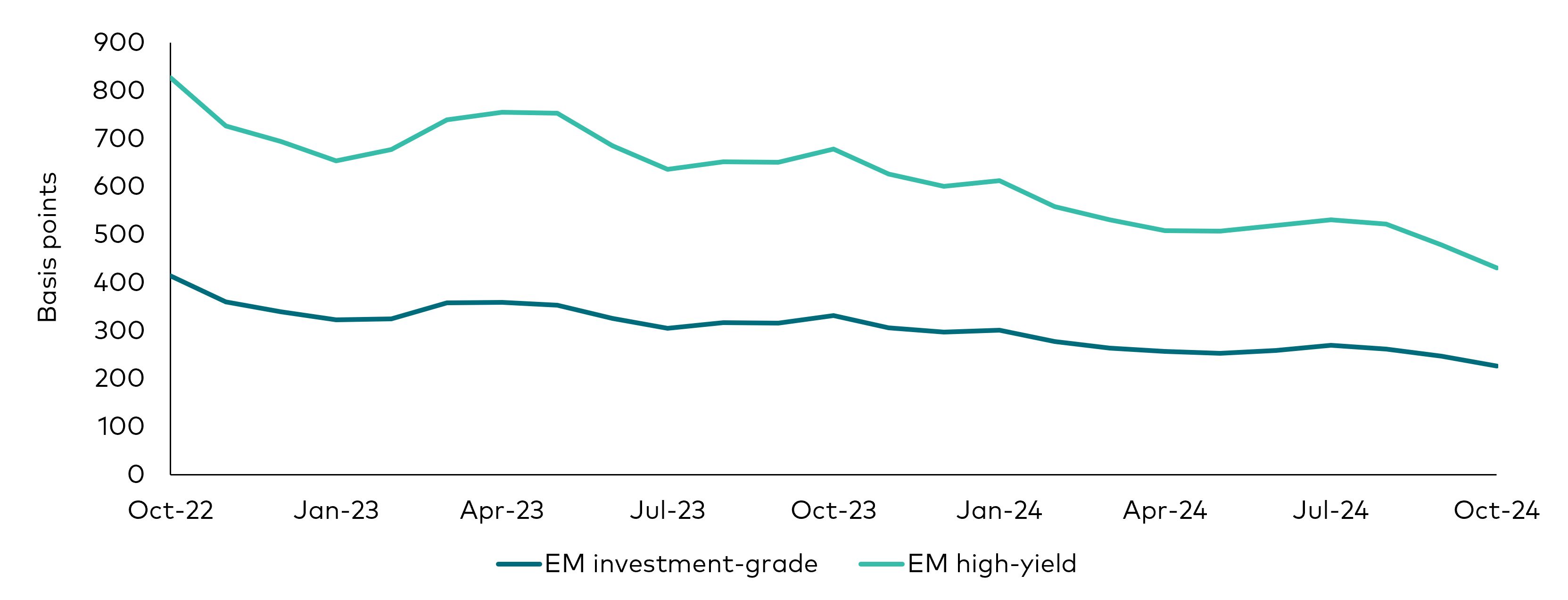

Corporate bonds from emerging countries fell by 1.7% in October, as the impact of the decline in US Treasury bonds (-2.8%) took precedence over the positive performance of spreads (+1, 1%). Emerging IG credit (-3.0%) notably underperformed emerging high yield bonds (-0.5%) during the month, due to the stronger influence of declines in US Treasuries on IG bond yields, as well as the positive impact of improving distressed credits, such as Argentina, on the performance of emerging high yield bonds.

Spreads between EM IG and high yield bonds

Source: Bloomberg and Vanguard. For the 24 months until October 30, 2024. References used: Emerging debt IG: Bloomberg EM USD Aggregate Average OAS Index; EM high-yield: Bloomberg Emerging Markets High Yield Average OAS Index.

Perspectives

We think the returns are attractive. Historically, returns at these levels have typically been followed by strong performance over the next six to 12 months.

Regarding credit, spreads are in line with a soft landing. In the United States, we continue to see good consumption performance, even if the market sees a certain divide between low and high income segments. Despite sluggish growth in Europe, we believe business fundamentals will remain strong. They are in fact starting from a good base and many issuers have reduced their debt in recent years. Technicals also remain strong, with strong demand for the asset class and supply expected to remain limited. Global credit currently offers higher returns than money market, and it is likely to significantly outperform it if further rate cuts are anticipated.

Regarding IG credit, we are starting to see a reversion to the mean in Europe, although we still view it as more attractive than US IG credit. Regarding high yield corporate bonds, technical data remains strong, although less favorable than in recent times. This year, the activity of the “rising stars” has accelerated compared to that of the “fallen angels”, but the situation is starting to normalize. Some spread compression has been seen within the sector, with CCC bonds outperforming B and BB bonds, although overall valuations still appear stretched. In the event of a recession, lower quality sectors would become more vulnerable. However, yields at current levels would likely offset some of the spread widening.

We are positive on emerging bonds because the fundamentals are strong and the yields are attractive. We believe a cycle of US rate cuts should be favorable for the asset class as long as global growth continues. However, valuations are tight and economic uncertainty remains high.

Information on investment risks

The value of investments, and the income from them, may fall as well as rise and investors may get back less than they invested.

Past performance is not a reliable indicator of future results.

Some funds invest in emerging markets which may be more volatile than more established markets. As a result the value of your investment may increase or decrease.

Funds investing in fixed income securities carry a risk of default and erosion of the capital value of your investment, and the level of income may fluctuate. Movements in interest rates may affect the principal value of bonds. Corporate bonds may offer higher yields but, as such, may present greater credit risk, increasing the risk of default and erosion of the capital value of your investment. Income levels may fluctuate and movements in interest rates may affect the principal value of bonds.

Reference to specific securities herein should not be construed as a recommendation to buy or sell such securities, but is for illustrative purposes only.

Important information

Reserved for professional investors (as defined in the MiF II Directive) investing for their own account (including management companies (funds of funds) and professional clients investing on behalf of their discretionary clients). In Switzerland, this document is intended for professional investors only. Not for distribution to the general public.

The information contained herein should not be considered an offer to buy or sell or the solicitation of an offer to buy or sell any securities in any jurisdiction where such offer or solicitation is contrary to the law, or to any person to whom it is unlawful to make such an offer or solicitation, or if the person making the offer or solicitation is not qualified to do so. The information in this document does not constitute legal, tax or investment advice. It is therefore recommended not to refer to it when making investment decisions.

The information contained herein is intended for educational purposes only and does not constitute a recommendation or solicitation to buy or sell any investments.

Published in the EEA by Vanguard Group (Ireland) Limited which is regulated in Ireland by the Central Bank of Ireland.

Published in Switzerland by Vanguard Investments Switzerland GmbH.

Published by Vanguard Asset Management, Limited, which is authorized and regulated in the United Kingdom by the Financial Conduct Authority.

© 2024 Vanguard Group (Ireland) Limited. All rights reserved.

2024 Vanguard Investments Switzerland GmbH. All rights reserved.

© 2024 Vanguard Asset Management, Limited. All rights reserved