In emerging markets, value and momentum stocks benefited from slightly lower valuations, but other factors also saw theirs rise.

In the third quarter, the rally continued for global and emerging market stocks, with global stocks up 6.4%, US stocks up 5.8% and emerging markets up 8.7%. Global developed market stocks were supported by the Federal Reserve’s 50 bps rate cut in September, strong economic indicators and encouraging earnings forecasts. The recovery plan announced by China had a strong impact on emerging markets, leading to a 25% increase in the CSI 300 over five consecutive sessions in September.

However, it is interesting to note that this was in reality a continuation of the rally observed since the start of the year, but in a different form. Utilities, real estate and finance were the best performing sectors in Q3, while information technology and communication services took the top spot in the first half of the year. This rotation suggests a healthier and more sustainable progression of the market.

This edition of WisdomTree’s quarterly stock market factors review aims to shed light on how these factors have evolved during the third quarter, and how this affects investors’ portfolios.

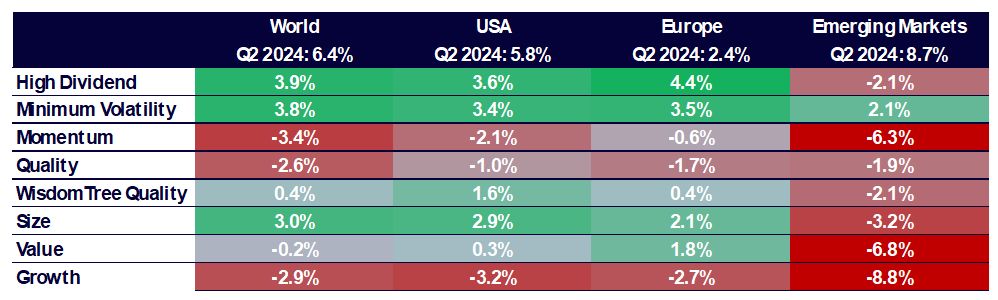

Focus on performance: a clear rotation of factors in Q3

In Q3, the MSCI World (+6.4%, MSCI USA (+5.8%) and the MSCI Emerging Markets (8.7%) recorded strong performances thanks to a resilient economy, positive earnings announcements and favorable monetary policies As in Q2, emerging markets recorded the best performance during the quarter, following China’s recovery plan.

Factor performance also highlighted the rotation we mentioned above:

- In Q3, High Dividend, Minimum Volatility and Small Cap factors performed best in developed markets.

- The quality, momentum and growth factors showed negative performances. This is a complete reversal compared to the first half of 2024.

- In emerging markets, only the minimum volatility factor showed outperformance.

- In this region, the growth factor was the most impacted, followed by the value and momentum factors.

Outperformance of stock market factors in Q3 2024 across regions

Source: WisdomTree, Bloomberg. From June 30, 2024 to September 30, 2024. Calculations are made in dollars for all regions, except Europe where they are made in euros. Historical performance is no guarantee of future performance, and any investment may lose value.

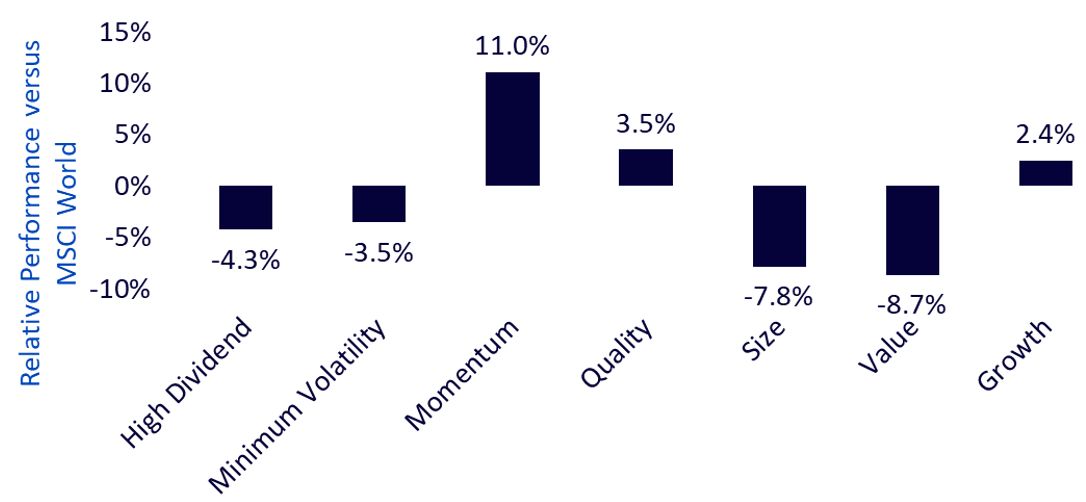

Factor performance since the beginning of the year: the situation remains the same overall

Despite the rotation that occurred in Q3, the overall situation for 2024 remains the same. The momentum factor remains the best performing for global equities, followed by quality and growth. The value factor and the scope factor remain the least efficient.

In emerging markets, the momentum factor also performed best this year through the end of September.

The high dividend and minimum volatility factors are resilient, but continue to record negative returns.

Outperformance of stock market factors in 2024

Source: WisdomTree, Bloomberg. From December 31, 2023 to September 30, 2024. Calculated in US dollars. Historical performance is no guarantee of future performance, and any investment may lose value.

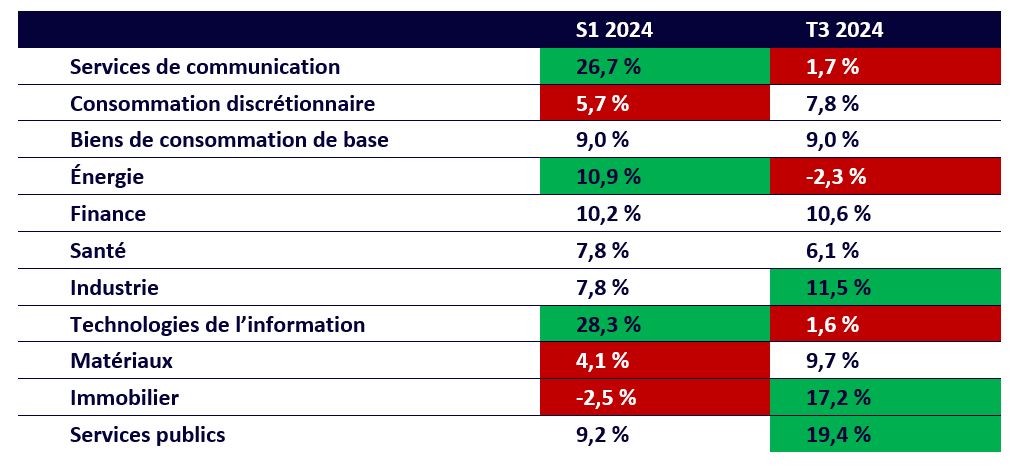

Third quarter: the time for portfolio readjustment has come

Strikingly, the three worst-performing sectors in Q3 had been the three best-performing sectors in the first half of the year. The rotation we observed across factors is also evident across sectors, providing a strong signal that the rally in stocks is gaining momentum and therefore becoming healthier. It is worth emphasizing that this is not just the case for performance, as fundamentals also show this range progression. Through mid-2024, the S&P 500’s earnings growth was primarily driven by the Magnificent Seven. In contrast, analyst forecasts for the rest of the year and early 2025 indicate that earnings growth will be shared more evenly between the seven largest stocks and the remaining 493 in the future.

S&P 500 sector performance in 2024

Source: WisdomTree, Bloomberg. From December 31, 2023 to September 30, 2024. Calculated in US dollars. Historical performance is no guarantee of future performance, and any investment may lose value.

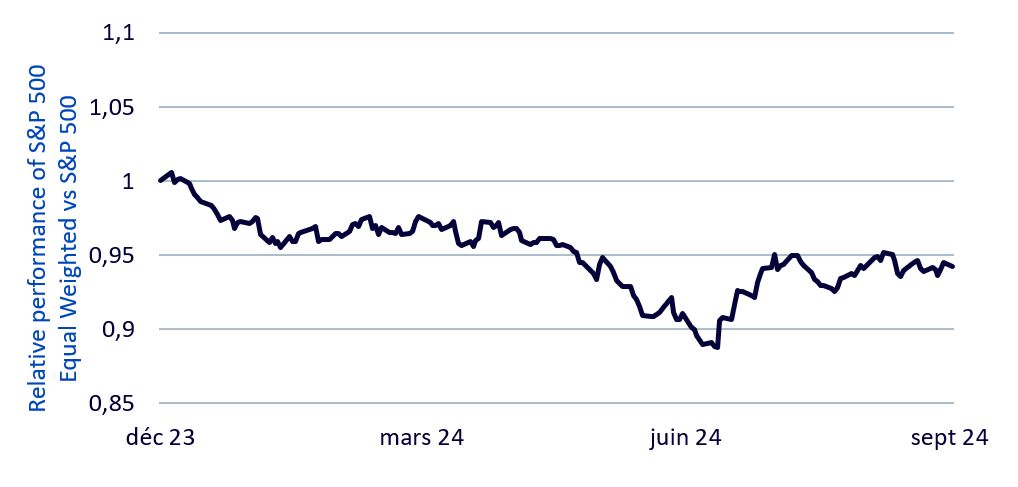

The performance of the Magnificent Seven (except Tesla) in Q3 was lackluster. Alphabet posted the 468e best performance in the S&P 500, Amazon the 440eMicrosoft the 439e and Nvidia the 424e.

This is what led to the outperformance of most strategies focused on diversification and tending to underweight very large caps. The S&P 500 Equal Weight index perfectly illustrates the effect of this diversification. It outperformed the S&P 500 by 9.2% over the past quarter.

Performance relative du S&P 500 Equal Weight par rapport au S&P 500

Source: WisdomTree, Bloomberg. From December 31, 2021 to June 30, 2024. Calculations are made in dollars for all regions, except Europe where they are made in euros. Historical performance is no guarantee of future performance, and any investment may lose value.

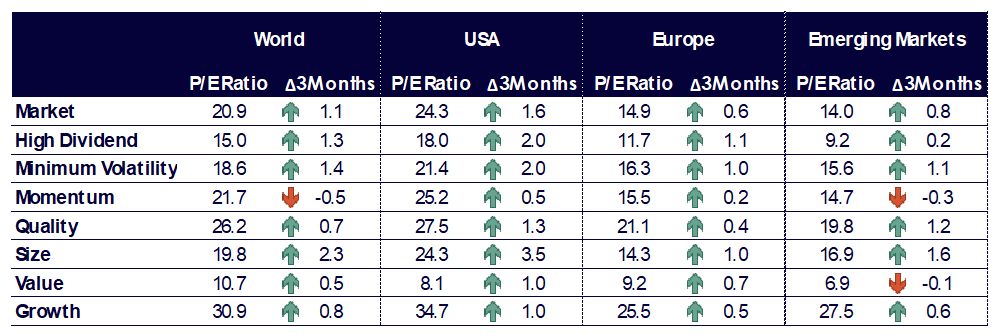

Valuations rose evenly in Q3

In Q3 2024, developed markets appreciated. Most factor portfolios have also become more expensive, with small caps seeing the biggest jump. Only momentum stocks saw their valuation fall slightly. The valuation of growth stocks, particularly in the United States, remains significantly high, reaching a price-to-earnings ratio of 34.7. In emerging markets, value and momentum stocks benefited from slightly lower valuations, but other factors also saw theirs rise. Overall, value stocks remain very cheap, with a price-to-earnings ratio of 8.1 in the US and 6.9 in emerging markets.

Historical evolution of price/earnings ratios of stock market factors

Source: WisdomTree, Bloomberg. As of September 30, 2024. Historical performance is no guarantee of future performance, and any investment may lose value.

Outlook for the rest of the year

With the Federal Reserve having begun its cycle of rate cuts, with positive economic data and solid earnings, the stock market rally appears set to continue. However, its broadening, which we saw in Q3, may require a different approach than what has worked over the past 18 months. With market concentration at an all-time high across stocks, sectors and countries, strategies that emphasize diversification could be a wise approach for investors.

A balanced approach, allowing investment outside of large and very large capitalizations, is likely to allow them to benefit from this expansion while diversifying their risk.

The world is represented by the MSCI World net TR index. The United States is represented by the MSCI USA net TR index. Europe is represented by the MSCI Europe net TR index. Emerging markets are represented by the MSCI Emerging Markets net TR Index. The minimum volatility factor is represented by the MSCI Min Volatility net total return index. The quality factor is represented by the MSCI Quality net total return index.

The momentum factor is represented by the MSCI Momentum net total return index. The high dividend factor is represented by the MSCI High Dividend net total return index. The breadth factor is represented by the MSCI Small Cap net total return index. The value factor is represented by the MSCI Enhanced Value net total return index. WisdomTree Quality is represented by the WisdomTree Quality Dividend Growth Index.

Disclaimer

This document was prepared by WisdomTree and its affiliates. It does not in any way constitute a forecast, research or investment advice, nor a recommendation, an offer or a solicitation to buy or sell securities or to adopt any investment strategy. The opinions expressed correspond to the date of publication of the document and may vary depending on the circumstances. The information contained herein, including any opinions expressed herein, is derived from proprietary and non-proprietary sources. Therefore, no guarantee is given as to the accuracy or reliability of the information. Further, WisdomTree, any affiliated company, any of their officers, employees or agents disclaim any liability for any errors or omissions (including liability to any person for negligence). Use of the information contained herein is at the sole discretion of the reader. Past performance is not a reliable indication of future performance.