Major French banks will integrate Wero, the replacement for Paylib, directly into their applications. This new service will allow transfers to be made simply by using a telephone number, an email address or a nickname. Ultimately, Wero aims to become a complete payment solution, competing with giants like Apple Pay and PayPal.

Bad news for Lydia and PayPal: the banks are fighting back.

This Monday, September 30, the main French banking groups announce the launch of Challenge, “a sovereign payment application”. Wero, which will gradually replace Paylib (the service will disappear in March 2025), aims first to simplify payments between individuals.

It integrates directly with the applications of major banks and allows you to make instant transfers, free of charge and without IBAN. Ultimately, Wero should become an online and in-store payment solution, using QR codes and NFC.

How does Wero, the new European payment solution, work?

Launched by EPI (European Payments Initiative), a structure in which 16 European shareholders from the banking sector have invested, Wero takes the form of an independent application and a service available in bank applications.

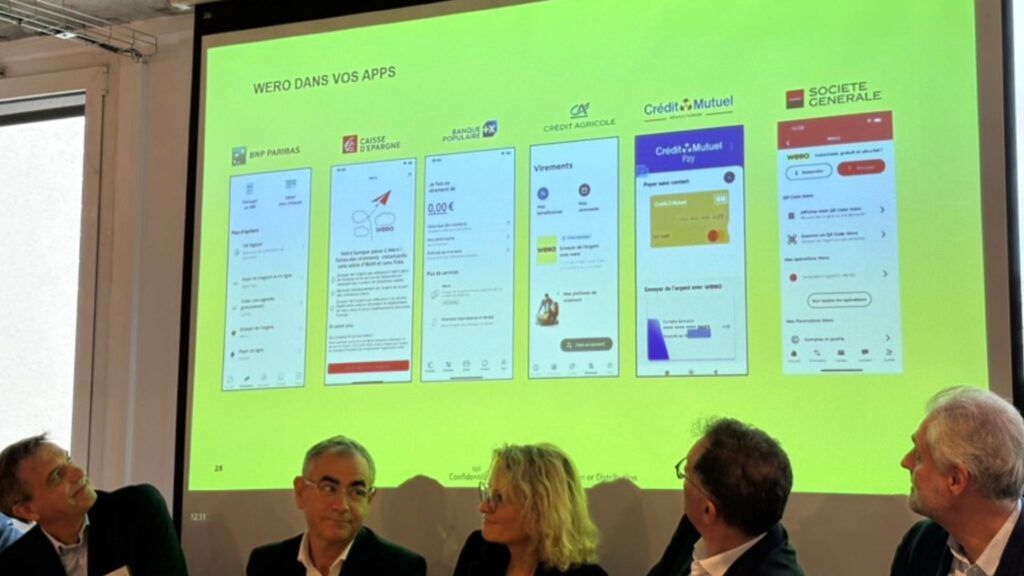

BNP Paribas, BPCE (Banque Populaire Caisse d’Épargne), Crédit Agricole, Crédit Mutuel Alliance Fédérale, Crédit Mutuel Arkéa, La Banque Postale and Société Générale are among its founding members, as well as all their subsidiaries.

All of them, with the exception of La Banque Postale, will allow their customers to make or receive Wero transfers from their usual application. La Banque Postale will call on its customers to download the independent software Wero, while awaiting a complete overhaul of its application.

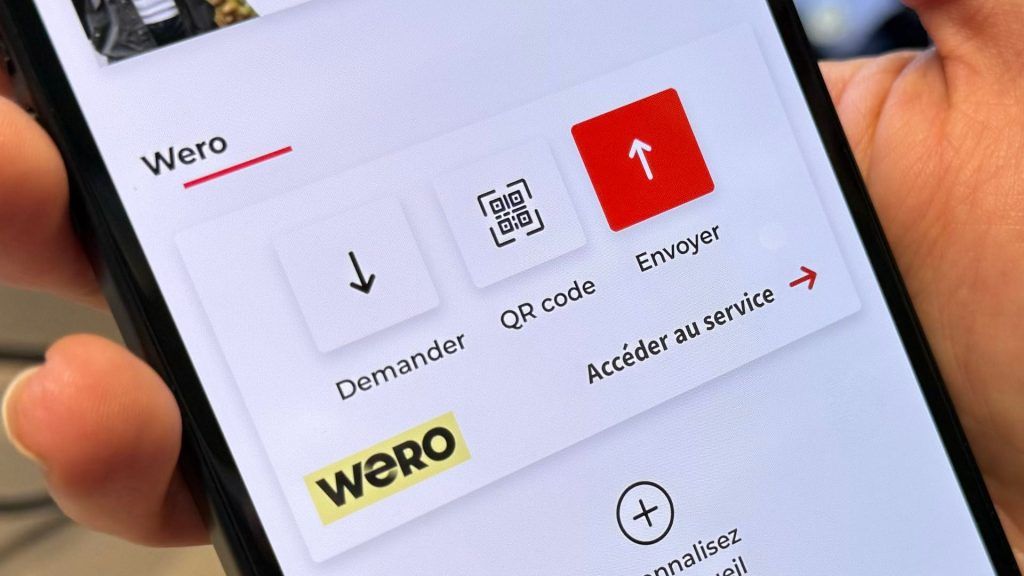

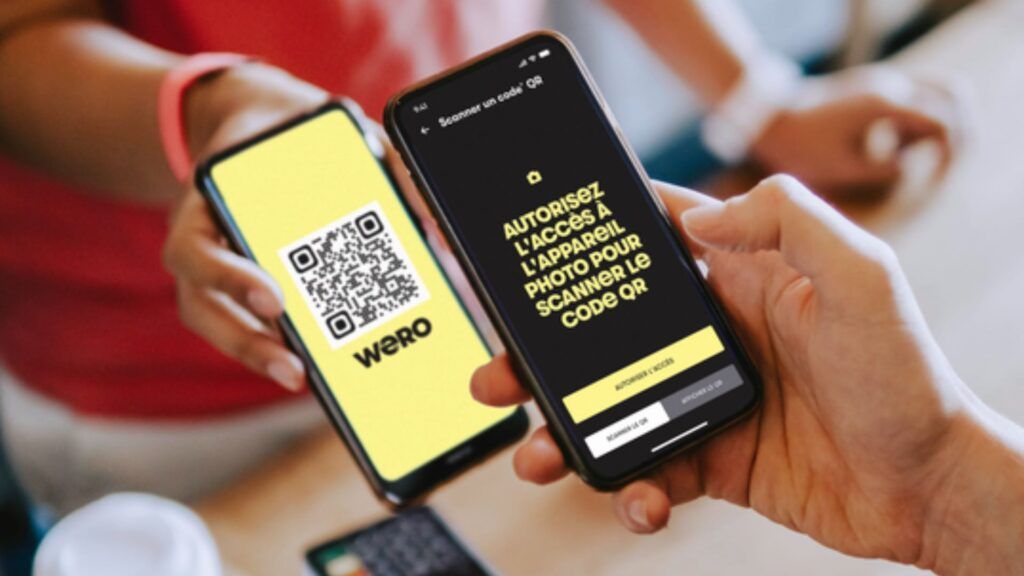

From your bank’s app, you will soon be able to make a Wero transfer. You can use your friend’s phone number, email or pseudonym to find them, then instantly send the money. Wero also allows you to request an amount, with a notification sent to the person concerned, or to generate a payment QR code. Once scanned, it allows you to immediately send the right amount to the right person, saving time.

With Wero, banks hope to recover customers who left for “fintechs”, such as Lydia or PayPal, with a service adapted to current needs. The alliance hopes to make Wero a recognized payment solution for peer-to-peer sales, thanks to its QR code system of which it says it is very proud. The sentence “I’ll make you a Wero” must become popular for the service to be successful.

The deployment of Wero among large banks should take place between today and the beginning of 2025. Then, by March 2025, Paylib will definitively bow out.

The consortium of banks, which claims that 46% of people adapt their mobile habits depending on their bank, says it is confident in the success of the project. Nearly ten additional banks have already expressed their desire to join Wero, while the transfer system will also work with German and Belgian accounts. Ultimately, EPI aims to create a universal European system, based on Wero, which could end the domination of Americans over digital payments (and therefore reduce dependence on Visa or Mastercard, with a European payment system based on instant transfers).

| Banque | Deployment date |

|---|---|

| BNP Paribas | October 24 |

| BPCE Group | Between September 2 and October 2 |

| Credit Agricole | September 26 |

| Crédit Mutuel Alliance Fédérale | Between September 25 and November 6 |

| Crédit Mutuel Arkéa | January 2025 |

| La Banque Postale (from the Wero app) | October 28 |

| Société Générale | October 24 |

By 2026, Wero could replace Apple Pay

The launch of Wero focuses on transfers between individuals, but banks are not hiding their real ambitions with the application. In 2025, they will begin to experiment with the possibility of paying on the Internet with Wero, a bit like buttons “Pay with PayPal” or “Pay with Apple Pay”. Then, they will attack physical businesses, with the possibility of using a QR code to pay any merchant, even if they do not have a card reader. EPI is inspired by WeChat Pay and AliPay, the Chinese payment systems, also based on QR codes.

Finally, in 3 to 4 years, Wero could attack your wallet. Banks hope to create “a simple and sovereign solution” to replace Apple Pay, Samsung Pay or Google Pay, the payment solutions integrated into smartphones.

In Europe, where the iPhone is now required to open its NFC chip, Wero could become the official application for contactless payment. There is still a long way to go, but French and European banks are finally preparing their entry into the 21st century.

{kind=link}